- Accounts

- About

- Trading

- Platforms

- Tools

- News & education

- News & education

- News & analysis

- Education hub

- Economic calendar

News & Analysis

Asian session looking to open up after Wall St rallies on strong earnings and data releases – tech leads after Meta beats

28 April 2023US stock indices rallied as risk appetite returned as banking fears seemed to take back seat and strong tech earnings saw the bulls in charge. The Dow and S&P 500 had their best day since January while the Nasdaq led the charge higher, rallying almost 2.5% after impressive tech earnings continued with Meta rallying 14% in the session.

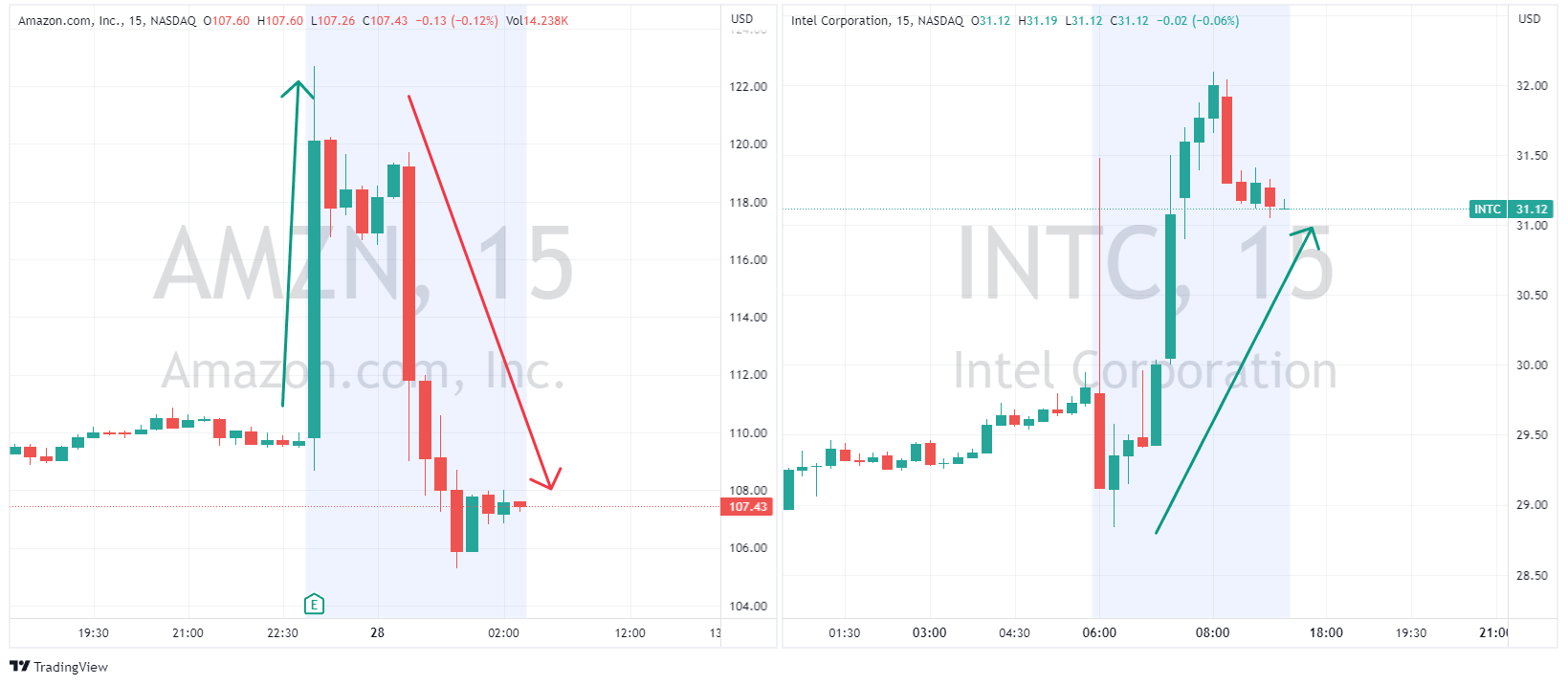

Tech earnings again saw some big moves after hours, with Amazon (AMZN) and Intel (INTC) both reporting after the bell, Amazon pumped and dumped over 12% in either direction after some initial confusion on the strength of earnings, Intel after some volatility rallied over 4% after hours on positive earnings.

Data releases out of the US came in mixed with Q1 GDP coming in well below consensus at 1.1% vs 2.0% expected, while jobless claims fell to 230k vs 247k expected, neither moved the needle on the expectation of a Fed hike next week, with 25bp priced in with a 87% probability according to Fed Fund futures.

FX Markets

USD saw mild gains ahead after mixed data in Thursday’s session and ahead of today’s PCE inflation figure. The US Dollar index rose to 101.80 after the weaker than expected GDP figures saw safe haven flows, only to retrace most of the gain as equity markets continued to rally.

The Yen and the Euro were both modestly weaker against the USD. EURUSD pivoted around the psychological 1.10 level, dipping below briefly before reclaiming it while USDJPY rallied as rising US bond yields saw rate differentials increase, and a positive stock market session saw safe haven buying of the Yen evaporate.

Commodities

Gold again traded in it’s range and again was rejected at the 2000 USD an ounce level, this level is a major psychological level which has been major resistance for Gold recently, similar to the JPY, rising yields and risk on stymying safe haven flows were major headwinds for the precious metal.

Copper rebounded off support at its March lows, rallying for the first time in seven sessions on improved risk sentiment.

Interestingly the Copper-Gold ratio is approaching the 2022 lows, this ratio is seen as a bellwether of global economic health and could be indicating recessionary forces ahead.

In todays economic releases, the big one will the Core PCE inflation reading out of the US. This reading is supposedly the Feds favoured inflation gauge, so whilst it is unlikely to change the Feds path next week, it may lead to a repricing of future Fed meetings and see some volatility especially in the USD on its release.

Disclaimer: Articles are from GO Markets analysts and contributors and are based on their independent analysis or personal experiences. Views, opinions or trading styles expressed are their own, and should not be taken as either representative of or shared by GO Markets. Advice, if any, is of a ‘general’ nature and not based on your personal objectives, financial situation or needs. Consider how appropriate the advice, if any, is to your objectives, financial situation and needs, before acting on the advice. If the advice relates to acquiring a particular financial product, you should obtain and consider the Product Disclosure Statement (PDS) and Financial Services Guide (FSG) for that product before making any decisions.

Next Article

BoJ Governor Ueda’s first monetary policy meeting

The Bank of Japan is due to hold its first monetary policy meeting under new Governor Ueda on the 29th of April 2023. Since his appointment, Governor Ueda has frequently indicated that the BoJ will continue with its current easing stance on monetary policy with targets for long and short-term interest rates. Although headline and core inflation run...

April 28, 2023

Read More >

Previous Article

What are jobless claims?

Jobless claims refer to a weekly statistic published by the U.S. Department of Labor, indicating the number of individuals applying for unemployment i...

April 27, 2023

Read More >