You've been using a 30-pip trailing stop for as long as you can remember. It feels professional, manageable and relatively safe.

But during volatile sessions, you see your winners get stopped out prematurely, while low-volatility winners drift back and hit stops that are relatively too tight.

Same 30 pips, different market contexts, but inconsistent in the protection of profit and overall results.

The Fixed-Pip Fallacy?

Traders gravitate toward fixed pip trailing stops because they feel concrete and calculable. The approach is easy to execute, readily automated through platforms like MetaTrader, and aligns with how most people naturally think about profit and loss.

But this simplicity masks a fundamental problem.

A twenty-five pip move in EURUSD during the London open represents an entirely different market event than the same move during the Asian session. The context matters, yet the fixed-pip approach treats them identically.

This becomes even more problematic when you consider different currency pairs. GBPJPY might have an average true range of thirty pips on an hourly chart, while EURGBP shows only ten. The same trailing stop applied to both instruments ignores the reality that volatility varies dramatically across pairs.

Timeframe introduces yet another layer of complexity. Take AUDUSD as an example: a ten-pip move on a four-hour chart barely registers as meaningful price action, but on a five-minute chart it represents a significant swing. The fixed-pip method treats these scenarios as equivalent.

The natural response might be to use something more sophisticated, like an ATR multiple. This accounts for your chosen timeframe, the instrument's normal volatility, and even session differences. But it brings its own complications.

When do you measure the ATR? Do you use the value at entry, knowing it might be distorted by sessional effects? Or do you make it dynamic, which becomes far more complex to implement in practice?

Perhaps there's another way forward that doesn't rely on abstract measures of volatility but instead responds directly to the movement of price in relation to the trade you're actually in—accounting for your lot size and the profit you've already captured.

Maximum Give Back: The Percentage Approach

Instead of asking "how do I protect profit after fifty pips," ask "how do I protect profit after giving back a certain percentage of open gains."

Consider a maximum give-back threshold of 40%. When your trade is up one hundred pips, the trailing stop activates if price retraces forty pips from peak, locking in a minimum of sixty pips.

But when that same trade reaches two hundred fifty pips of profit, the stop adjusts, and now it activates at a one-hundred-pip pullback, securing at least one hundred fifty pips. The stop distance scales naturally with the magnitude of the win you're sitting on.

This creates a logical asymmetry that fixed pip approaches miss entirely. Small winners receive tighter protection. Big winners get room to breathe.

The approach adapts automatically to what the market is actually giving you in real time, without requiring you to predict anything in advance.

You don't need to maintain a reference table where EURUSD gets thirty pips and GBPJPY gets sixty. You don't need different standards for different instruments at all.

The same 40% logic works whether the average true range is high or low, whether volatility is expanding or contracting. It is designed to be more adaptive to regime changes than fixed-pip stops, potentially requiring less manual recalibration as it's responding to the trade itself rather than to abstract measures of what the instrument normally does.

The market tells you how much it's willing to move in your direction, and you protect that information proportionally. Nothing more complicated than that.

Key Parameters to Specify in Your System:

- Maximum Give Back Percent: 30-50% is typical, but is dependent on how much profit retracement you can tolerate.

- Minimum Profit to Activate: In dollar amount or an ATR multiple form entry. This prevents premature exits on tiny winners, e.g., if it has moved 5 pips at 40% that would mean you are only locking in a 3-pip profit.

- Update Frequency: Potentially every bar. More frequent, but there may be issues if there is a limited ability to look at the market (if using some sort of automation, this could be programmed).

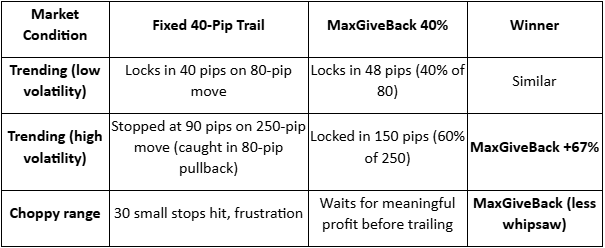

Is Maximum Giveback Always the Optimum Trail?

As with many approaches, results can be highly dependent on underlying market conditions. It is important to be balanced.

The table below summarises some observations when maximum giveback has been used as part of automated exits.

The major difference isn’t likely to be an increased win rate. It is about keeping more of your runners during high-volatility price moves rather than donating them back to the market.

It may not always be the best approach, as different strategies often merit different exit approaches.

There are two obvious scenarios where fixed pips may still be worth consideration.

- Very short-term scalping (sub-20 pip targets)

- News trading, where you want instant hard stops

Integrating Maximum Giveback With Your System

You may have other complementary exit filters in place that you already use. Remember, the ideal is often a combination of exits, with whichever is triggered first.

There is no reason why this approach will not work well with approaches such as set stops, take profits and partial closes (where you simply use maximum Giveback in the remainder as well as time-based exits.

Final Thoughts

To use fixed-pip trailing stops irrespective of instrument pricing, volatility, timeframe, and sessional considerations is the trading equivalent of wearing the same jacket in summer and winter.

Maximum Give Back trailing adjusts to the ‘market weather’. It won't make bad trades good, but it could help stop you from cutting your best trades short just because your stop was designed for average conditions.

The market doesn't trade in averages but has specific likely moves dependent on context. Your exits should not be average either.

Reportingdates and release times are based on company investor relations calendars whereconfirmed. Where dates or times are not marked confirmed, they are GO Marketsestimates. Consensus EPS, revenue and analyst-range data are sourced fromBloomberg and Earnings Whispers, as at 09 July 2026 (AEST). Company guidance,backlog and operating metrics are sourced from the latest company filings orresults presentations, unless stated otherwise. Any scenario analysis reflectsGO Markets analysis. Figures and schedules may change without notice.

The information provided is of general nature only and does not take into account your personal objectives, financial situations or needs. Before acting on any information provided, you should consider whether the information is suitable for you and your personal circumstances and if necessary, seek appropriate professional advice. All opinions, conclusions, forecasts or recommendations are reasonably held at the time of compilation but are subject to change without notice. Past performance is not an indication of future performance. Go Markets Pty Ltd, ABN 85 081 864 039, AFSL 254963 is a CFD issuer, and trading carries significant risks and is not suitable for everyone. You do not own or have any interest in the rights to the underlying assets. You should consider the appropriateness by reviewing our TMD, FSG, PDS and other CFD legal documents to ensure you understand the risks before you invest in CFDs. These documents are available here.

Any references to Australian or international shares, sectors, indices, ETFs, crypto-related stocks or other instruments are provided for market commentary and watchlist purposes only and do not constitute a recommendation, offer or solicitation to buy, sell or hold any financial product or adopt any investment strategy. International markets may involve additional risks, including currency fluctuations, regulatory differences, market structure differences, reduced liquidity and higher volatility. Company-specific, sector-specific and macroeconomic risks may also affect performance.

Commentary on geopolitical developments, economic data, central bank decisions, earnings, policy changes and other global or financial market events is based on information available at the time of publication and may change without notice. Such events can lead to sudden market moves, price gaps, reduced liquidity, wider spreads and increased volatility, particularly in leveraged products such as CFDs. Forward-looking statements, expectations and scenario analysis are inherently uncertain and should not be relied on as guarantees of future market behaviour or outcomes.