The latest move in oil has put energy names back in focus. Over the past six months, Exxon Mobil and Baker Hughes have outperformed Brent crude on a normalised basis, Chevron has remained broadly constructive, SLB has lagged the commodity and Woodside's broker consensus has been more measured.

When crude moves, the impact rarely stays contained to the commodity itself. Higher oil prices can affect inflation expectations, shipping costs and corporate margins across the global economy.

What the latest move is showing

There are three broad ways companies can benefit from firmer oil prices:

- Producing oil and gas, by selling the commodity at a higher price

- Providing services and equipment to producers

- Transporting oil around the world

Each of the names below represents one of those exposure types, with a different risk profile when crude rises.

1. Exxon Mobil (NYSE: XOM)

Over the past six months, Exxon Mobil has outperformed Brent crude, with its share price up nearly 35% compared with about 30% for Brent. As of 11 March 2026, both were trading just over 3% below their all-time highs, while Exxon remained closer to its 52-week high.

Exxon Mobil is one of the world's largest integrated oil companies, with exposure spanning exploration, production, refining and chemicals. When oil prices rise, its upstream business may benefit from wider margins, while its scale and diversification can help cushion weaker parts of the cycle.

Exxon Mobil (XOM) vs. Brent Crude 3-month performance

Analyst consensus: Buy

According to TradingView data, analyst sentiment towards Exxon is broadly positive. Of the 31 analysts tracked, 15 rate the stock Strong Buy or Buy, 13 rate it Hold, 1 rates it Sell and 2 rate it Strong Sell.

That positive view is linked to Exxon's balance sheet strength and higher-margin production. The most optimistic analysts project a 1-year price target as high as US$183.00. The average price target is US$145.00, which sits about 3.6% below the current trading price.

2. Chevron (NYSE: CVX)

Chevron is another global integrated major that has benefited from the recent move higher in crude, with its shares trading near 52-week highs. Like Exxon, Chevron operates across the value chain, including upstream production, refining and marketing.

Chevron's completed acquisition of Hess adds Guyana and other upstream assets, which some analysts see as supportive over time. That said, the earnings impact remains subject to integration, project execution and commodity price risks.

Exxon Mobil vs Chevron performance, 6-month chart

Analyst consensus: Buy

Chevron is viewed similarly to Exxon, with broker sentiment remaining broadly constructive. Recent TradingView aggregates show 30 analysts covering the stock over the past three months, with 17 rating it Strong Buy or Buy, 11 at Hold, 1 at Sell and 1 at Strong Sell.

Analysts have highlighted Chevron's diversified portfolio and the potential contribution from Hess, although commodity price volatility and execution risk may keep some more cautious.

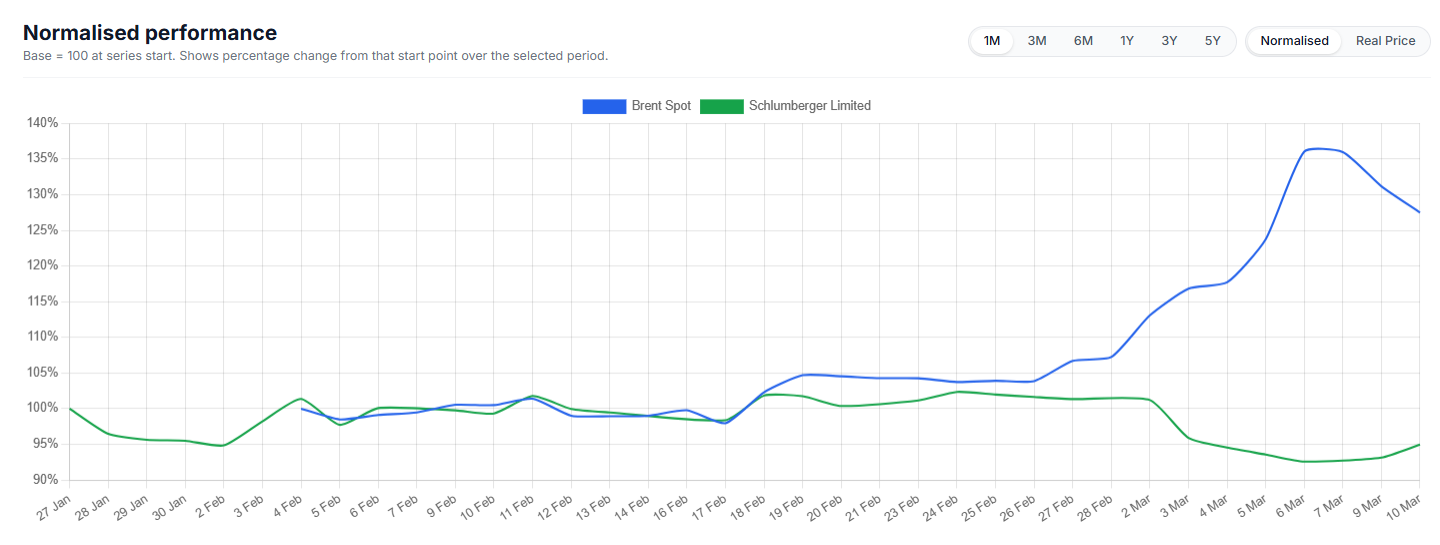

3. SLB (NYSE: SLB)

SLB, previously known as Schlumberger, is one of the world's largest oilfield services and technology providers. It supplies tools, equipment and software that help producers find, drill and complete wells more efficiently.

Over the past six months, SLB has lagged Brent crude, with the share price trading in a choppier range and remaining below its recent peak. That suggests the stronger oil backdrop has not been fully reflected in the share price.

That pattern is not unusual for oilfield services companies, where customer spending decisions often follow moves in the underlying commodity rather than move in lockstep with them. Any future re-rating would depend on factors including producer capital spending, contract timing, service pricing, offshore activity and broader market conditions. A firmer oil price should not be assumed to translate automatically into a firmer SLB share price.

SLB vs Brent crude, 1-month normalised performance

Consensus: Buy

According to TradingView data, third-party analyst consensus on SLB is Buy. Of the 33 analysts covering the stock, 27 rate it Strong Buy or Buy, 4 rate it Hold and 2 rate it Sell or Strong Sell.

That indicates constructive broker sentiment, although the gap between oil prices and SLB's recent share-price performance suggests investors may still want clearer evidence of improving service demand and pricing before the stock fully reflects the stronger commodity backdrop.

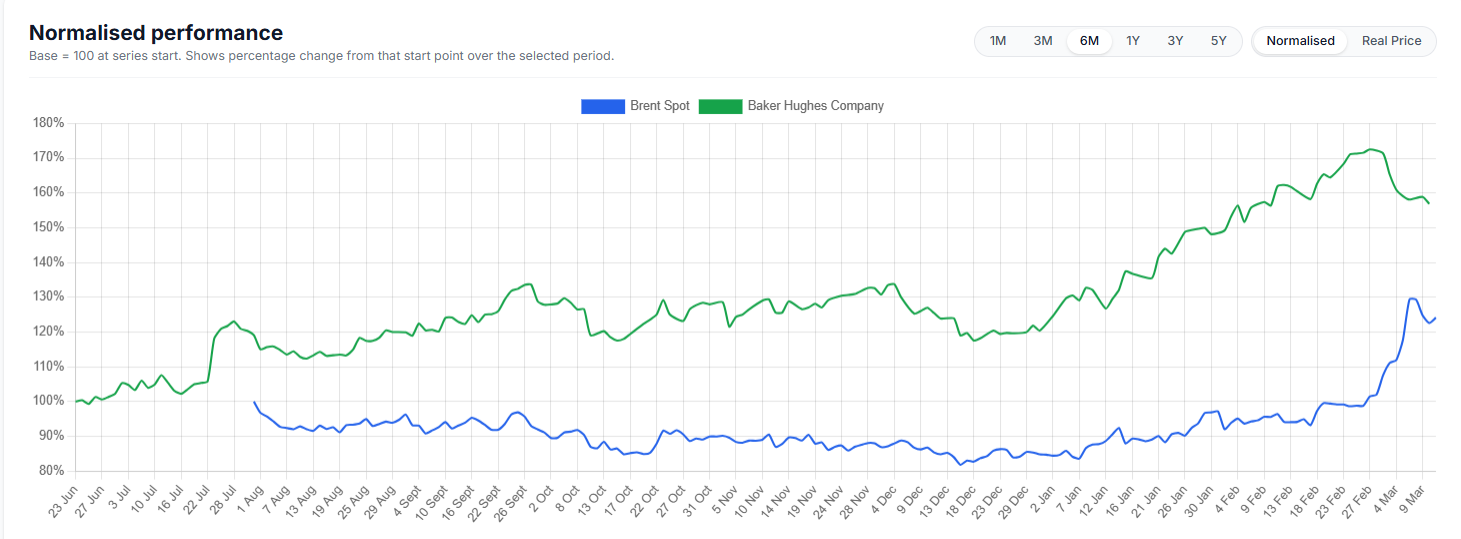

4. Baker Hughes (NASDAQ: BKR)

Baker Hughes is another major oilfield services and equipment provider, with additional exposure to industrial segments such as LNG and power infrastructure. Even when oil prices are not at extreme highs, advances in drilling technology and lower break-even costs have helped keep many shale plays profitable, supporting demand for its services.

The company has also been described as well positioned because of its balance sheet and its exposure to ongoing exploration and production activity. In a period of higher, or even stable-to-firm, oil prices, that mix of services and energy technology may create several revenue drivers.

Over the past six months, Baker Hughes has materially outperformed Brent crude on a normalised basis. Brent traded in a much tighter range for most of the period before moving higher late, while BKR climbed more steadily and reached a significantly stronger cumulative gain. That suggests BKR's share price benefited not only from the backdrop in oil, but also from company-specific optimism and broader support for oilfield services and energy technology names.

BKR vs Brent crude, 6-month normalised performance

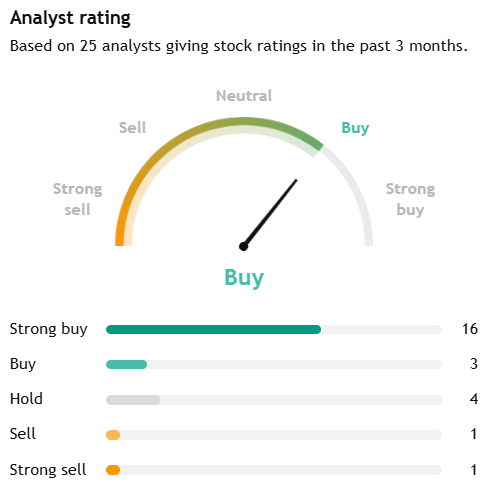

Analyst consensus: Buy

According to TradingView data, Baker Hughes is categorised as Strong Buy. Based on 25 analysts who provided ratings over the past three months, 16 rated the stock Strong Buy, 3 rated it Buy, 4 rated it Hold, 1 rated it Sell and 1 rated it Strong Sell.

Overall, broker sentiment towards Baker Hughes is broadly positive, with more than three quarters of covering analysts rating the stock either Strong Buy or Buy, while most of the remainder were at Hold. That supportive analyst view appears to reflect BKR's exposure to both traditional oilfield services and broader energy and industrial technology markets, including LNG infrastructure.

5. Woodside Energy (ASX: WDS)

Woodside Energy gives the list an Australia-based producer with significant exposure to LNG and oil markets. Its earnings are closely tied to realised commodity prices, which makes the stock sensitive to shifts in crude and gas pricing, as well as broader global energy demand.

Compared with some of the larger US energy names, broker sentiment towards Woodside appears more measured. Investors are balancing the company's global LNG exposure and leverage to stronger energy prices against softer recent realised prices, project and execution risks, and longer-term regulatory and decarbonisation pressures.

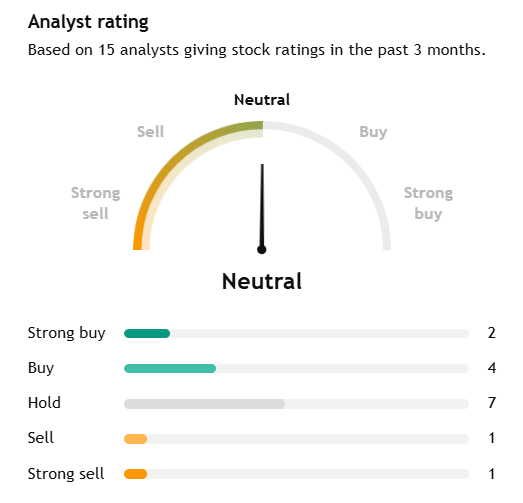

Analyst consensus: Hold

According to TradingView data, Woodside is rated Neutral/Hold. Of 15 analysts, 2 rate it Strong Buy, 4 rate it Buy, 7 rate it Hold, 1 rates it Sell and 1 rates it Strong Sell.

The average 12-month price target is A$29.20 versus a current price of about A$30.28, implying downside of roughly 3.6%. Relative to the larger US energy names in this list, that points to a more cautious broker view.

6. Global oil tanker operators

Oil tanker companies can benefit when firmer oil prices, OPEC+ policy shifts and geopolitical tension increase long-distance shipments and disrupt usual trade routes. When oil volumes travel further, 'tonne-mile' demand can support tanker day rates and profitability even when the broader energy market is volatile.

Analyst consensus: N/A

This is a broader industry category rather than a single publicly traded stock, so there is no single broker consensus to cite. Analyst views would need to be assessed at the company level, such as Frontline plc (FRO), Euronav (EURN) or Scorpio Tankers (STNG).

More broadly, the sector is cyclical. Any benefit from tighter shipping markets can reverse if routes normalise, freight rates fall or supply increases.

Risks and constraints

Higher oil prices do not remove risk for these names.

- If prices rise too far, too fast, demand destruction and policy responses can weigh on future earnings.

- Political decisions from OPEC+ or other major producers can reverse a rally by increasing supply.

- Services and tanker companies are highly cyclical. When the cycle turns, pricing power can fade quickly.

- Company-specific issues, including project execution, realised pricing and capital spending, still matter.

Taken together, these names may benefit from firmer oil prices, but they also carry sector-specific, geopolitical and company-level risks that deserve close attention.

Key market observations

- Woodside provides LNG and oil exposure, although current broker sentiment is more neutral than for the larger US names.

- Tanker operators may benefit when freight markets tighten, though that trade remains highly cyclical and route-dependent.

- SLB and Baker Hughes may benefit if firmer oil prices translate into more drilling and completion activity, but the share-price response has been mixed.

- Exxon Mobil and Chevron offer direct exposure to stronger upstream margins, supported by diversified operations.

References in this article to Exxon Mobil, Chevron, SLB, Baker Hughes, Woodside, tanker operators, analyst consensus ratings and price targets are included for general market commentary only and do not constitute a recommendation or offer in relation to any financial product or security. Third-party data, including consensus ratings and target prices, may change without notice and should not be relied on in isolation. Energy and shipping exposures are cyclical and can be materially affected by commodity price volatility, realised pricing, production changes, project execution, geopolitical disruptions, freight market conditions, regulatory developments and shifts in investor sentiment. Any views about potential beneficiaries of higher oil prices are subject to significant uncertainty.

Reportingdates and release times are based on company investor relations calendars whereconfirmed. Where dates or times are not marked confirmed, they are GO Marketsestimates. Consensus EPS, revenue and analyst-range data are sourced fromBloomberg and Earnings Whispers, as at 09 July 2026 (AEST). Company guidance,backlog and operating metrics are sourced from the latest company filings orresults presentations, unless stated otherwise. Any scenario analysis reflectsGO Markets analysis. Figures and schedules may change without notice.

The information provided is of general nature only and does not take into account your personal objectives, financial situations or needs. Before acting on any information provided, you should consider whether the information is suitable for you and your personal circumstances and if necessary, seek appropriate professional advice. All opinions, conclusions, forecasts or recommendations are reasonably held at the time of compilation but are subject to change without notice. Past performance is not an indication of future performance. Go Markets Pty Ltd, ABN 85 081 864 039, AFSL 254963 is a CFD issuer, and trading carries significant risks and is not suitable for everyone. You do not own or have any interest in the rights to the underlying assets. You should consider the appropriateness by reviewing our TMD, FSG, PDS and other CFD legal documents to ensure you understand the risks before you invest in CFDs. These documents are available here.

Any references to Australian or international shares, sectors, indices, ETFs, crypto-related stocks or other instruments are provided for market commentary and watchlist purposes only and do not constitute a recommendation, offer or solicitation to buy, sell or hold any financial product or adopt any investment strategy. International markets may involve additional risks, including currency fluctuations, regulatory differences, market structure differences, reduced liquidity and higher volatility. Company-specific, sector-specific and macroeconomic risks may also affect performance.

Commentary on geopolitical developments, economic data, central bank decisions, earnings, policy changes and other global or financial market events is based on information available at the time of publication and may change without notice. Such events can lead to sudden market moves, price gaps, reduced liquidity, wider spreads and increased volatility, particularly in leveraged products such as CFDs. Forward-looking statements, expectations and scenario analysis are inherently uncertain and should not be relied on as guarantees of future market behaviour or outcomes.