- Accounts

- About

- Trading

- Platforms

- Tools

- News & education

- News & education

- News & analysis

- Education hub

- Economic calendar

News & Analysis

US Stocks finish mixed in choppy session after Hot UK CPI spooks the markets

20 April 2023Major US indexes finished mixed in a choppy session for equities and FX after a hotter than expected re-ignited inflation fears and a global hawkish re-pricing of risk assets.

Decent earnings and the big bounce back in Netflix encouraged the “Buy the Dip” crowd, pulling stocks up from their lows to see the major US indexes finish mostly flat for the day, the Dow being the underperformer, down 79.62 points or 0.23%, whilst the Nasdaq eked out a green finish.

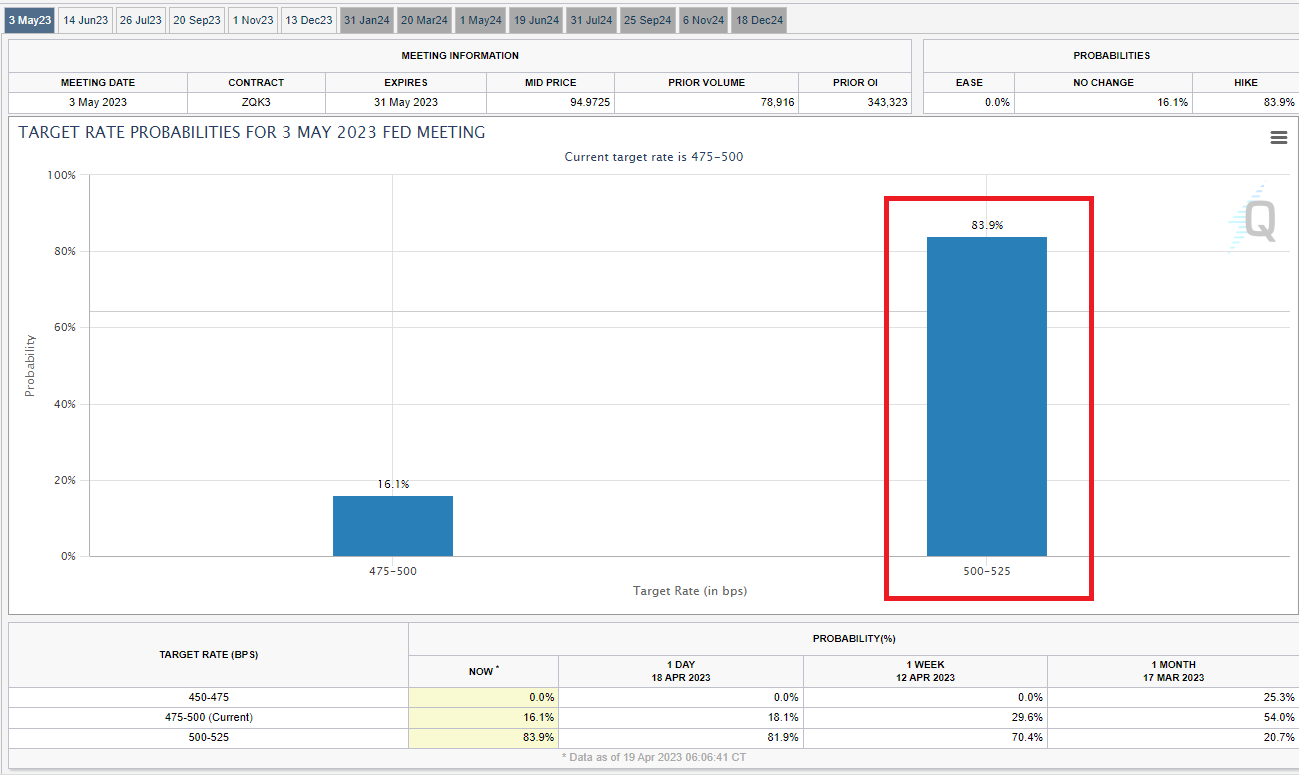

UK inflation figures showed an easing from 10.4% y/y February to 10.1% Y/Y in March, but still well above the expected 9.8% Y/Y that markets had priced in which saw a hawkish move in rates markets for all major Central banks, not just the BoE, Fed Fund odds of a FOMC 25 bp rate hike climbed to 84% as the global inflation story remains stubborn.

One market that didn’t seem to by phased by this hawkish re-pricing was the VIX or “fear Index” which continued the recent volume sell-off, hitting its lowest level since 2021. The VIX is a measure of the Put/Call ratio, a lower level means less investors buying Puts (downside protection) showing that even against the sticky inflation, a lot of investors (rightly or wrongly) remain optimistic on equities.

FX Markets

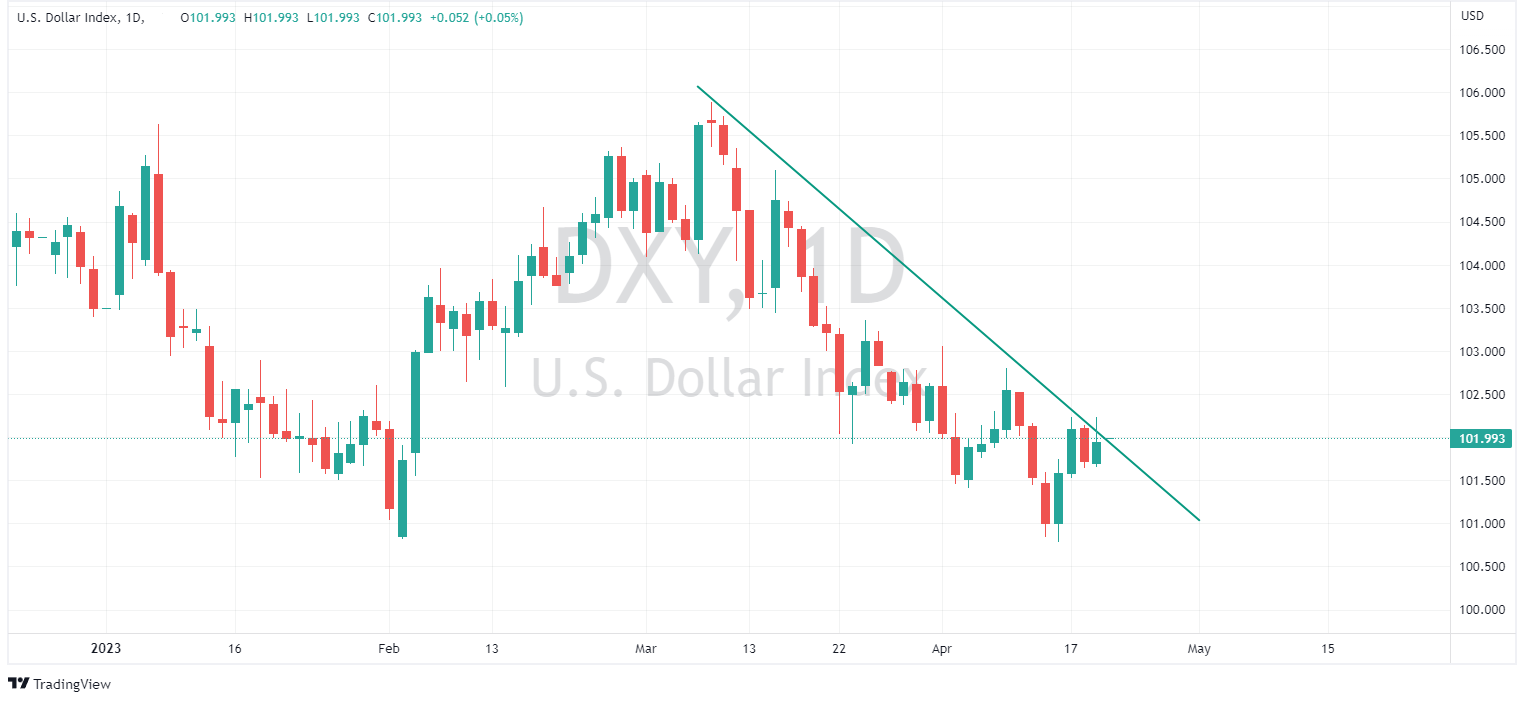

FX Markets, like equities, had a choppy session on Wednesday, with the US Dollar mostly stronger , supported by a hawkish re-pricing of the Feds rate hike trajectory, with any rate cuts from the Fed later in the year now being unlikely according to the futures market. This saw the US dollar index poke above 1.02 before finding resistance at its upper trend line and pulling back.

EURUSD was marginally lower Wednesday with trading either side of 1.0950, while GBPUSD was the outperformer after the hot UK CPI figure, managing to hold post CPI gains against the USD in a choppy session as UK Bond markets are now pricing in a 99% probability for a 25bp hike in May.

Commodities

Crude Oil continued to dip, trading back to the low end of the range it formed after the Surprise OPEC+ cuts a few weeks ago amid 4yr high Russian exports and hawkish central bank pricing.

Gold Dipped below the 2000 USD an ounce level on a stronger USD and higher yields, but did find some serious buying at the 1970 support area, recouping most of its losses.

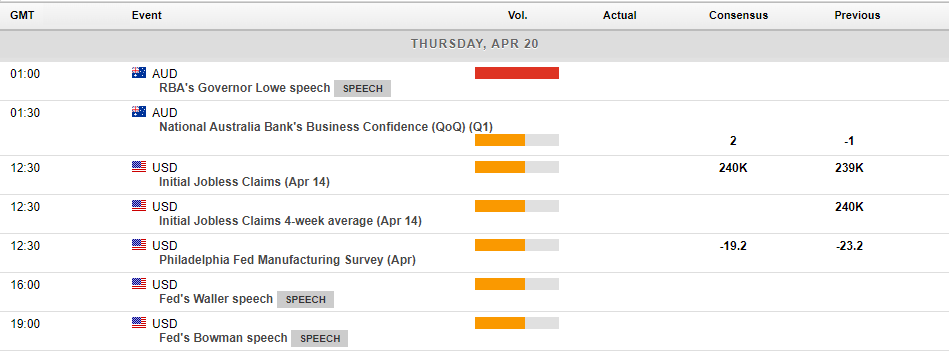

In todays economic announcements, RBA governor Lowe will be speaking at Midday AEST, after the this weeks RBA minutes , which were seen as hawkish, this is one to watch for AUD traders.

Also later, US unemployment claims for the week will be released which will give another indicator of the strength (or not) of the US labour market and by extension the US economy.

Disclaimer: Articles are from GO Markets analysts and contributors and are based on their independent analysis or personal experiences. Views, opinions or trading styles expressed are their own, and should not be taken as either representative of or shared by GO Markets. Advice, if any, is of a ‘general’ nature and not based on your personal objectives, financial situation or needs. Consider how appropriate the advice, if any, is to your objectives, financial situation and needs, before acting on the advice. If the advice relates to acquiring a particular financial product, you should obtain and consider the Product Disclosure Statement (PDS) and Financial Services Guide (FSG) for that product before making any decisions.

Next Article

Gold technical and fundamental analysis – How to trade it’s recent price action

Gold has been one of the most popular and highly traded markets recently as price action in the precious metal has really come alive, rate hikes, the war in Ukraine and Bank Crises have all played a part in the fundamental reasons for gold price movements in the last 12 months. Let’s take a look at the chart to see these fundamental effects and h...

April 20, 2023

Read More >

Previous Article

Tesla results have arrived

World’s largest automaker, Tesla Inc. (NASDAQ: TSLA), reported Q1 financial results after market close in the US on Wednesday. Elon Musk’s company...

April 20, 2023

Read More >