What Is a Bollinger Band Reversal?

The Bollinger Band reversal is a mean-reversion strategy that looks for the price to temporarily overextend beyond its typical range before snapping back inside.It consists of three lines:

- An upper band

- A lower band

- A 20-period simple moving average (SMA) in the middle.

The Upper band and Lower band are set at a default level two standard deviations from the SMA.When the price closes outside one of the bands, it often signals significant price momentum. This level of momentum is often followed by "move exhaustion” and subsequently pulls back to a more usual state. If the next move returns price inside the bands, this may offer a possible reversal opportunity. This setup can happen on any timeframe on any asset.As always with any chart pattern, the pattern can only be thought of as complete when there is a confirmation candle. Confluence factors such as where the candle sits in relation to the range (e.g., in the top half for a bullish trade) and increased volume are often considered part of a complete trading plan in the Bollinger Band reversal setup.

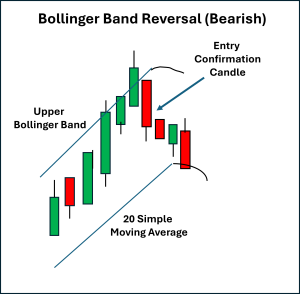

Bearish Bollinger Band Reversal

A bearish reversal occurs when the price moves sharply above the upper band, showing extreme buying pressure, but then closes back inside the band. This can suggest the price may have become overextended, and sellers are attempting to regain control.

- A: Prior advance (bull candles) → strong upward momentum pushing price above the upper Bollinger Band.

- B: Over-extension → a candle closes outside the band, showing unsustainable momentum.

- C: Re-entry with confirmation → a subsequent bearish candle closes back inside the band, confirming the reversal.

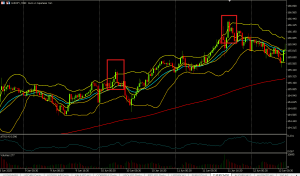

The EURJPY 30-minute chart below shows two examples of this setup in action:

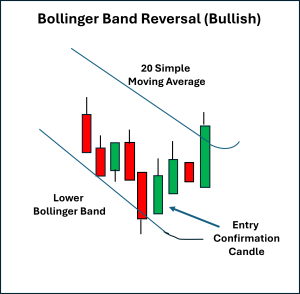

Bullish Bollinger Band Reversal

A bullish reversal can be seen on a chart when the price falls below the lower band, showing extreme selling pressure, but then closes back inside the lower band. This suggests that the downward trend in price is becoming exhausted, and buyers are stepping in.

- A: Prior decline (bear candles) → strong downward momentum pushing price below the lower Bollinger Band.

- B: Over-extension → a candle closes outside the band, showing unsustainable downside pressure.

- C: Re-entry with confirmation → a subsequent bullish candle closes back inside the band, validating the reversal.

The Gold Futures CFD 1-hourly chart below shows two examples of this setup in action:

Stop Placement and Exits

Initial risk management stops are generally placed just beyond the candle that closed outside the band:

- In bearish setups: the stop goes above the high of the candle that closed outside the upper band.

- In bullish setups: the stop goes below the low of the candle that closed outside the lower band.

Exit strategies often include:

- Using the 20-period SMA (the “mean” in the mean reversion) as a potential profit target or signal to trail the initial stop level.

- Using a set risk-to-reward ratio, such as 2:1.

Final Thoughts

The Bollinger Band reversal is a popular mean reversion strategy that takes advantage of price extremes. Traders who are developing a formal trading plan with this setup wait for a close outside the bands, a re-entry of price inside the bands (in the opposite direction), and a confirmation candle.In essence, traders are attempting to capitalise on the pullback.It is important to note that price can “walk the bands” for an extended time, so risk management with stop placements should be part of any plan using this setup.Practicing across different market conditions, asset classes, and timeframes will help identify where Bollinger Band reversals are most effective and how best to integrate them into your trading toolbox.

Reportingdates and release times are based on company investor relations calendars whereconfirmed. Where dates or times are not marked confirmed, they are GO Marketsestimates. Consensus EPS, revenue and analyst-range data are sourced fromBloomberg and Earnings Whispers, as at 09 July 2026 (AEST). Company guidance,backlog and operating metrics are sourced from the latest company filings orresults presentations, unless stated otherwise. Any scenario analysis reflectsGO Markets analysis. Figures and schedules may change without notice.

The information provided is of general nature only and does not take into account your personal objectives, financial situations or needs. Before acting on any information provided, you should consider whether the information is suitable for you and your personal circumstances and if necessary, seek appropriate professional advice. All opinions, conclusions, forecasts or recommendations are reasonably held at the time of compilation but are subject to change without notice. Past performance is not an indication of future performance. Go Markets Pty Ltd, ABN 85 081 864 039, AFSL 254963 is a CFD issuer, and trading carries significant risks and is not suitable for everyone. You do not own or have any interest in the rights to the underlying assets. You should consider the appropriateness by reviewing our TMD, FSG, PDS and other CFD legal documents to ensure you understand the risks before you invest in CFDs. These documents are available here.

Any references to Australian or international shares, sectors, indices, ETFs, crypto-related stocks or other instruments are provided for market commentary and watchlist purposes only and do not constitute a recommendation, offer or solicitation to buy, sell or hold any financial product or adopt any investment strategy. International markets may involve additional risks, including currency fluctuations, regulatory differences, market structure differences, reduced liquidity and higher volatility. Company-specific, sector-specific and macroeconomic risks may also affect performance.

Commentary on geopolitical developments, economic data, central bank decisions, earnings, policy changes and other global or financial market events is based on information available at the time of publication and may change without notice. Such events can lead to sudden market moves, price gaps, reduced liquidity, wider spreads and increased volatility, particularly in leveraged products such as CFDs. Forward-looking statements, expectations and scenario analysis are inherently uncertain and should not be relied on as guarantees of future market behaviour or outcomes.