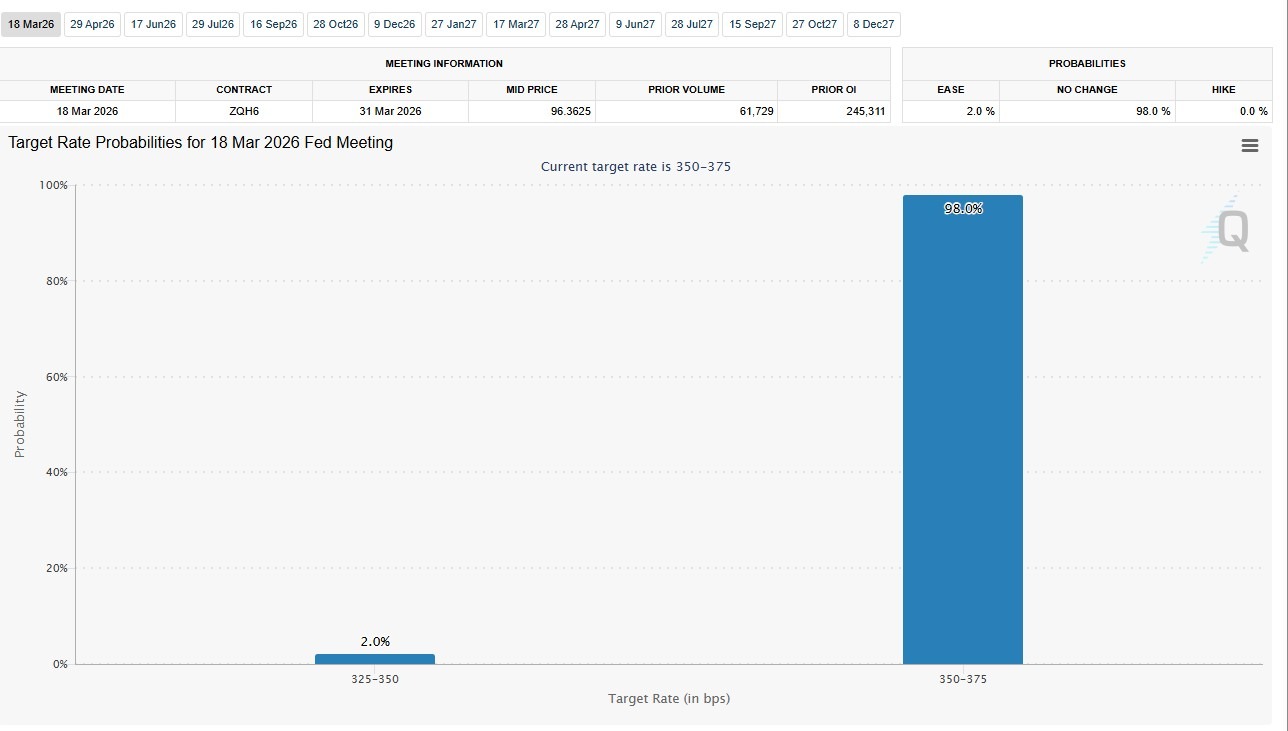

March sets up as a “repricing month” for US assets. The FOMC meeting is the centre point, with CME FedWatch showing a pause as the dominant baseline. Markets could become more sensitive to surprises in such circumstances, especially prints that alter the perceived balance between sticky inflation and slowing demand.

Rates and policy

Key dates

- FOMC meeting (two-day): 18–19 March (AEDT).

- Fed decision (FOMC statement): 5:00 am, 19 March (AEDT).

- Fed press conference: 5:30 am, 19 March (AEDT).

What markets look for

Even if rates are left unchanged, the decision can still move markets through updated projections, the policy statement, and the Chair’s guidance.

With a pause largely priced, attention shifts away from “move vs no move” and toward whether the Fed’s messaging validates the current rate path or nudges expectations toward a higher-for-longer stance or earlier easing.

Any change in the balance of risks (inflation vs growth/financial conditions) can drive a repricing in front-end rates, USD, and equity multiples.

Inflation and the link to FedWatch pricing

Key dates

- Consumer Price Index (CPI): 11:30 pm, 11 March (AEDT).

- Personal Income & Outlays/ PCE (January PCE): 11:30 pm, 13 March (AEDT).

What markets look for

When markets are anchored around a pause, inflation can become a key swing factor for the expected path of policy.

A firmer inflation profile can push the implied rate track higher and tighten financial conditions, while softer prints can reinforce the pause narrative and pull forward cut expectations.

Inflation data that arrives ahead of the policy decision tends to have greater influence on immediate repricing, while the later inflation/consumption pulse can shape end-of-month positioning and the market’s confidence in the disinflation trend.

Jobs data: the next test of rate expectations

Key dates

- ISM Manufacturing PMI: 2:00 am, 3 March (AEDT).

- ISM Services PMI: 2:00 am, 5 March (AEDT).

What markets look for

Payrolls, unemployment and wage signals can reset the tone for yields, USD and equities ahead of the major inflation and policy catalysts.

In practice, surprises often show up first in front-end rates and rate volatility, then filter into broader risk sentiment and equity pricing, especially if the data challenges assumptions about cooling demand and easing wage pressure.

Equities, tariffs and geopolitics

What markets look for

US indices remain highly sensitive to the rate narrative. The S&P 500 Index (SPX) and Nasdaq 100 Index (NDX) have traded at relatively elevated levels in recent weeks, with the VIX providing a read on implied volatility conditions.

Beyond the data calendar, the tail-end of earnings season may still generate stock-specific volatility. Tariffs and trade policy also remain a live macro risk, with official guidance for importers able to affect costs, margins and sector sentiment.

The US Supreme Court has also held that IEEPA does not authorise the imposition of tariffs under that statute. That may add uncertainty around the legal footing of Trump's tariffs.

On the geopolitical front, renewed Middle East tensions have coincided with firmer crude pricing, which may influence inflation expectations and risk appetite around CPI and Fed week (among other drivers).

Disclaimer: Articles are from GO Markets analysts and contributors and are based on their independent analysis or personal experiences. Views, opinions or trading styles expressed are their own, and should not be taken as either representative of or shared by GO Markets. Advice, if any, is of a ‘general’ nature and not based on your personal objectives, financial situation or needs. Consider how appropriate the advice, if any, is to your objectives, financial situation and needs, before acting on the advice.