Welcome to 2026. Inflation is still sticky, real yields still matter, and markets can reprice fast when policy, geopolitics, and risk sentiment shift.

With the next RBA decision approaching, the ASX can feel less like a local story and more like a window into the broader macro regime.

- The next rate decision is about balancing inflation control, growth risks, and how the Australian dollar (AUD) responds to yield differentials and risk sentiment.

- Lenders can act as real-time signals for household and small and medium enterprise (SME) credit conditions as funding costs and competition shift.

- Names like MQG and GMG can be highly sensitive to global liquidity, risk appetite, and changes in discount rates. That can amplify moves when conditions change.

1. Commonwealth Bank (ASX: CBA)

CBA is often viewed as a bellwether for domestic mortgage and funding conditions. It can react to funding costs and any early hints of arrears pressure, rather than just the “rates up/rates down” trigger.

Traders track the yield curve and bank funding spreads as it’s often the first tell when the story flips from net interest margin (NIM) to credit (bad debts).

In a higher-for-longer setup, banks may rally first on “better margins” until the market starts pricing credit risk instead.

In the past, CBA hit record highs in early 2026, up roughly 11% year to date (YTD), before a mid-February pullback amid broader market volatility.

What traders watch

- Broker handling: Every broker call listed is on the bearish side: 4 Sells, 1 Underperform, and 1 Underweight.

- Targets and implied move: Target prices range from A$120 to A$140. Using the “% to reach target” column, that implies a last close of about A$178.68, which equates to roughly 22% to 33% downside versus the targets shown (targets are estimates, often set on a 12-month basis, and are not guarantees).

- Broker tone: Citi stays Sell (“in-line quarter/limited revisions”), while Morgan Stanley argues the hurdle is higher after the stock’s outperformance, as “good” may no longer be good enough.

Risks: 2:30 pm (AEDT) event gaps, sharp reversals, and quick sell-offs when too many traders are on the same side.

2. National Australia Bank (ASX: NAB)

NAB is where you look when you’re trying to figure out whether the engine room of the economy is purring or quietly overheating.

When policy stays tight, lenders can look fine right up until they don’t. Margins can defend, deposit competition can bite, and the comfort line, “defaults are contained”, gets stress-tested by reality.

NAB tends to trade more like an invoice: what businesses are paying, what they are delaying, and how fast conditions change when confidence turns.

What traders watch

NAB is up about +15.46% YTD, with the stock recently around A$49. In the latest print, traders are watching how NAB’s A$2.02 billion Q1 cash profit shows resilience even as expense inflation starts to creep in.

- Broker handling: Mixed but skewed cautious. 3 Sells (Morgans, Citi, Ord Minnett), 1 Equal-weight (Morgan Stanley), 1 Outperform (Macquarie), 1 Buy (UBS).

- Targets and implied move: Targets run from A$35.00 to A$50.50, and the implied last price is about A$49.10, so most targets sit below the market, with UBS as the modest upside call.

- Broker tone: UBS is the lone Buy with a A$50.50 target (about +2.85%). Macquarie is Outperform, but its A$47.00 target is still below the implied last. Citi, Morgans and Ord Minnett stay Sell, with targets clustered A$35.00 to A$39.25. Morgan Stanley sits Equal-weight at A$43.50.

Risks: margin squeeze from deposit competition, a turn in business credit quality, and fast repricing if “contained defaults” stops being credible.

3. Macquarie Group (ASX: MQG)

Macquarie is what you get when you blend markets, asset management, deal-making, and a global appetite for volatility... and then you hand it a very expensive suit.

Macquarie doesn’t just listen to the RBA; it listens to the entire room. Global rates, risk appetite, and market plumbing often matter as much as anything said in Martin Place.

What traders watch

While Macquarie is about +1.93% since Jan 1, traders are watching global yields, volatility regime shifts, plus any read-through to deal flow and trading conditions.

- Broker handling: The table shows a mostly supportive mix, with no outright sells.

- Targets and implied move: The implied last price is about A$207.12. The average target across the brokers shown is about A$229.70 (around +10.9%), with targets ranging A$210.00 to A$255.00.

- Broker tone: Ord Minnett and UBS sit at Buy, Citi is Neutral, Morgans is Hold, and Morgan Stanley is Equal-weight. Supportive, but not unanimous.

Risks: liquidity shocks, volatility “air pockets,” and a fast downgrade cycle if global conditions sour.

4. QBE Insurance Group (ASX: QBE)

Insurers can look unusually “clean” in higher-rate regimes because their float finally earns something again. When yields rise, investment income can start doing real work and can offset a lot… until the world reminds everyone why insurance exists in the first place.

QBE is a tug-of-war between higher rates helping the portfolio and catastrophe risk plus claims inflation trying to take it back with interest.

What traders watch

QBE is about +10.06% since Jan 1, and in the latest print, traders are watching investment yield trends, catastrophe loss headlines, and any sign that the pricing cycle is cooling.

- Broker handling: The broker calls shown lean positive: Outperform (Macquarie), Buy (Citi, UBS), Overweight (Morgan Stanley), plus two upgrades to Buy from Hold (Ord Minnett, Bell Potter).

- Targets and implied move: The table implies a last price around A$21.89. Targets range from A$21.80 to A$26.00. The average target across the brokers shown is about A$24.06 (around +9.9%).

- Broker tone: Ord Minnett has the highest target at A$26.00 (about +18.78%). Bell Potter is also shown as an upgrade to Buy, but with a target fractionally below the implied last (-0.41%).

Risks: major catastrophe events, claims inflation and the market pricing “peak rates” too early.

5. Goodman Group (ASX: GMG)

Goodman Group is where the rate story meets the valuation story. When yields rise, long-duration equities get repriced as the discount rate stops being theoretical.

GMG can still execute operationally, but the stock often trades like a referendum on the cost of capital, cap rates, and whether the market thinks the future is getting cheaper or more expensive.

What traders watch

GMG is about +2.86% YTD with traders watching 10-year yields, cap rate chatter, funding conditions, and data-centre narrative momentum.

- Broker handling: The broker calls shown skew positive, with no sells. 3 Buys (Bell Potter, Citi, UBS), plus Accumulate (Morgans), Outperform (Macquarie), Overweight (Morgan Stanley), and 1 Hold (Ord Minnett).

- Targets and implied move: Targets range from A$31.25 to A$41.50. The implied last close is about A$28.42, and the simple average target in the table is about A$36.35 (around +27.9% above the implied last close).

- Broker tone: Morgan Stanley is the most bullish on target price at A$41.50 (+46.02%). Citi is also constructive at Buy with A$40.00 (+40.75%). Ord Minnett is the cautious outlier at Hold with A$31.25 (+9.96%).

Risks: valuation compression if yields rise, refinancing narratives, and cap rate repricing.

6. JB Hi-Fi (ASX: JBH)

JB Hi-Fi tends to move with the mood of the household budget. When the consumer is steady, and promotions stay manageable, the story can look simple.

When spending tightens and discounting ramps up, the market quickly shifts to margin risk and guidance risk.

What traders watch

As JB Hi-Fi is about -12.64% since Jan 1, traders are keenly watching sales momentum vs consumer confidence, promo intensity, and margin resilience.

- Broker handling: The mix is constructive overall, but not unanimous. The table shows 2 Buys (Citi, Bell Potter) plus 1 Upgrade to Buy from Neutral (UBS), 1 Outperform (Macquarie), 1 Upgrade to Hold from Trim (Morgans), and two more cautious calls, Underweight (Morgan Stanley) and Lighten (Ord Minnett).

- Targets and implied move: Targets range from A$72.90 to A$119, with the implied last close about A$84.06. The simple average target in the table is about A$96.56 (around +14.9% above the implied last close).

- Broker tone: Bell Potter is the most bullish on target price at A$119.00 (+41.57%). Macquarie is also positive at Outperform with A$106.00 (+26.10%). On the cautious side, Morgan Stanley is Underweight with A$72.90 (-13.28%). The latest change notes in the table show UBS upgraded to Buy from Neutral and Morgans upgraded to Hold from Trim (both dated 17/02/2026).

Risks: unemployment surprises, margin damage from discounting, and fast sentiment reversals around consumer data.

7. Judo Capital (ASX: JDO)

Judo Capital is the cleanest expression of “small and medium enterprise (SME) credit plus funding competition” you can put on a screen.

It is a focused lender, a floating-rate loan book, and growth that looks heroic right up until funding costs and defaults decide to start a conversation at the same time.

In an RBA-sensitive tape, Judo can move like a thesis you cannot pause. Spreads, deposits, credit quality, and sentiment all reprice in real time.

What traders watch

Judo is down about -0.58% since Jan 1, meaning traders are watching net interest margin (NIM) versus deposit competition, SME arrears and default signals, and any shift in funding pressure.

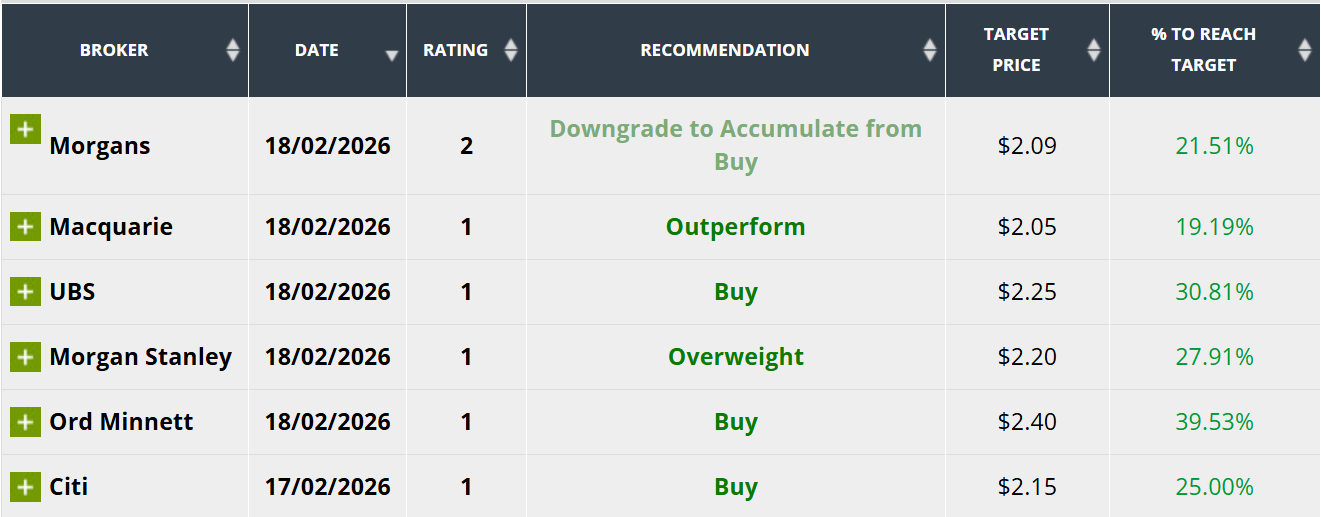

- Broker handling: The calls shown are all positive. Morgans is Accumulate (noted as a downgrade from Buy). Macquarie is Outperform. Morgan Stanley is Overweight. UBS, Ord Minnett, and Citi are all Buy.

- Targets and implied move: Targets range from A$2.05 to A$2.40, the implied last close is about A$1.72. The simple average target in the table is about A$2.19 (around +27% above the implied last close).

- Broker tone: Ord Minnett is the most bullish on target price at A$2.40 (+39.53%). UBS is Buy at A$2.25 (+30.81%). Morgan Stanley is Overweight at A$2.20 (+27.91%). Citi is Buy at A$2.15 (+25.00%). Morgans sits at A$2.09 (+21.51%) after the downgrade to Accumulate. Macquarie is Outperform at A$2.05 (+19.19%).

Risks: SME credit turns quickly in a slowdown, and funding competition can squeeze spreads faster than loan yields reprice.

Disclaimer: Articles are from GO Markets analysts and contributors and are based on their independent analysis or personal experiences. Views, opinions or trading styles expressed are their own, and should not be taken as either representative of or shared by GO Markets. Advice, if any, is of a ‘general’ nature and not based on your personal objectives, financial situation or needs. Consider how appropriate the advice, if any, is to your objectives, financial situation and needs, before acting on the advice. If the advice relates to acquiring a particular financial product, you should obtain our Disclosure Statement (DS) and other legal documents available on our website for that product before making any decisions.