Artificial intelligence stocks have begun to waver slightly, experiencing a selloff period in the first week of this month. The Nasdaq has fallen approximately 2%, wiping out around $500 billion in market value from top technology companies.

Palantir Technologies dropped nearly 8% despite beating Wall Street estimates and issuing strong guidance, highlighting growing investor concerns about stretched valuations in the AI sector.

Nvidia shares also fell roughly 4%, while the broader selloff extended to Asian markets, which experienced some of their sharpest declines since April.

Wall Street executives, including Morgan Stanley CEO Ted Pick and Goldman Sachs CEO David Solomon, warned of potential 10-20% drawdowns in equity markets over the coming year.

And Michael Burry, famous for predicting the 2008 housing crisis, recently revealed his $1.1 billion bet against both Nvidia and Palantir, further pushing the narrative that the AI rally may be overextended.

As we near 2026, the sentiment around AI is seemingly starting to shift, with investors beginning to seek evidence of tangible returns on the massive investments flowing into AI, rather than simply betting on future potential.

However, despite the recent turbulence, many are simply characterising this pullback as "healthy" profit-taking rather than a fundamental reassessment of AI's value.

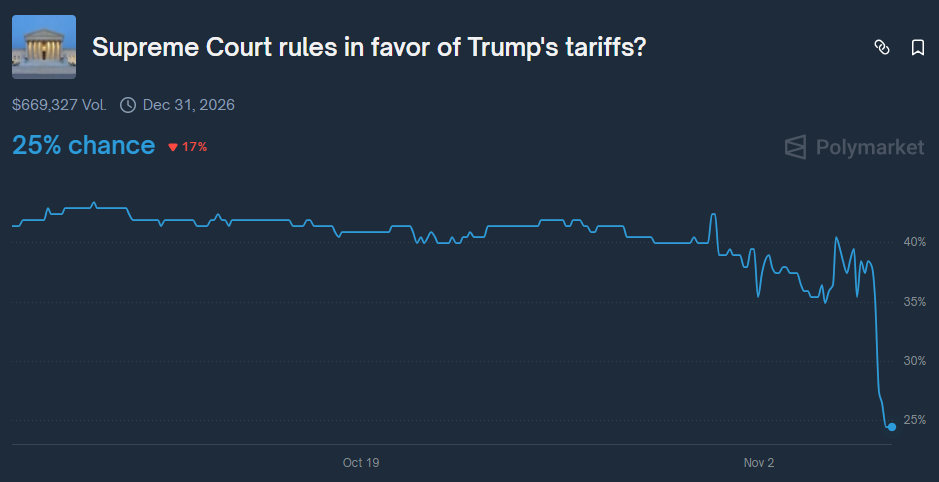

Supreme Court Raises Doubts About Trump’s Tariffs

The US Supreme Court heard arguments overnight on the legality of President Donald Trump's "liberation day" tariffs, with judges from both sides of the political spectrum expressing scepticism about the presidential authority being claimed.

Trump has relied on a 1970s-era emergency law, the International Emergency Economic Powers Act (IEEPA), to impose sweeping tariffs on goods imported into the US.

At the centre of the case are two core questions: whether the IEEPA authorises these sweeping tariffs, and if so, whether Trump’s implementation is constitutional.

Chief Justice John Roberts and Justice Amy Coney Barrett indicated they may be inclined to strike down or curb the majority of the tariffs, while Justice Brett Kavanaugh questioned why no president before Trump had used this authority.

Prediction markets saw the probability of the court upholding the tariffs drop from 40% to 25% after the hearing.

The US government has collected $151 billion from customs duties in the second half of 2025 alone, a nearly 300% increase over the same period in 2024.

Should the court rule against the tariffs, potential refunds could reach approximately $100 billion.

The court has not indicated a date on which it will issue its final ruling, though the Trump administration has requested an expedited decision.

Shutdown Becomes Longest in US History

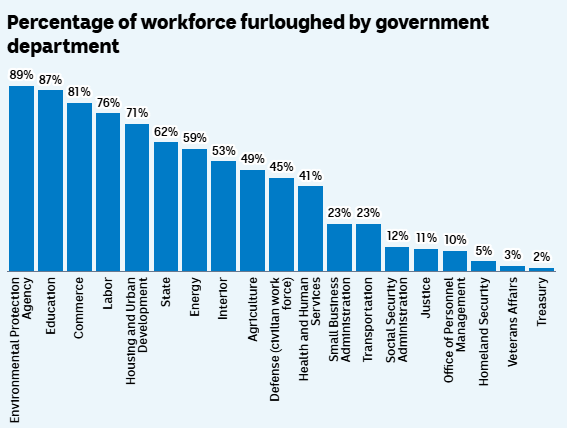

The US government shutdown entered its 36th day today, officially becoming the longest in history. It surpasses the previous 35-day record set during Trump's first term from December 2018 to January 2019.

The Senate has failed 14 times to advance spending legislation, falling short of the 60-vote supermajority by five votes in the most recent vote.

So far, approximately 670,000 federal employees have been furloughed, and 730,000 are currently working without pay. Over 1.3 million active-duty military personnel and 750,000 National Guard and reserve personnel are also working unpaid.

SNAP food stamp benefits ran out of funding on November 1 — something 42 million Americans rely on weekly. However, the Trump administration has committed to partial payments to subsidise the benefits, though delivery could take several weeks.

Flight disruptions have affected 3.2 million passengers, with staffing shortages hitting more than half of the nation's 30 major airports. Nearly 80% of New York's air traffic controllers are absent.

From a market perspective, each week of shutdown reduces GDP by approximately 0.1%. The Congressional Budget Office estimates the total cost of the shutdown will be between $7 billion and $14 billion, with the higher figure assuming an eight-week duration.

Consumer spending could drop by $30 billion if the eight-week duration is reached, according to White House economists, with potential GDP impacts of up to 2 percentage points total.

The information provided is of general nature only and does not take into account your personal objectives, financial situations or needs. Before acting on any information provided, you should consider whether the information is suitable for you and your personal circumstances and if necessary, seek appropriate professional advice. All opinions, conclusions, forecasts or recommendations are reasonably held at the time of compilation but are subject to change without notice. Past performance is not an indication of future performance. Go Markets Pty Ltd, ABN 85 081 864 039, AFSL 254963 is a CFD issuer, and trading carries significant risks and is not suitable for everyone. You do not own or have any interest in the rights to the underlying assets. You should consider the appropriateness by reviewing our TMD, FSG, PDS and other CFD legal documents to ensure you understand the risks before you invest in CFDs. These documents are available here.

Any references to Australian or international shares, sectors, indices, ETFs, crypto-related stocks or other instruments are provided for market commentary and watchlist purposes only and do not constitute a recommendation, offer or solicitation to buy, sell or hold any financial product or adopt any investment strategy. International markets may involve additional risks, including currency fluctuations, regulatory differences, market structure differences, reduced liquidity and higher volatility. Company-specific, sector-specific and macroeconomic risks may also affect performance.

Commentary on geopolitical developments, economic data, central bank decisions, earnings, policy changes and other global or financial market events is based on information available at the time of publication and may change without notice. Such events can lead to sudden market moves, price gaps, reduced liquidity, wider spreads and increased volatility, particularly in leveraged products such as CFDs. Forward-looking statements, expectations and scenario analysis are inherently uncertain and should not be relied on as guarantees of future market behaviour or outcomes.