GO Markets,让交易更进一步

智慧交易,从选择值得信赖的全球券商开始。低点差、快速成交、零入金手续费、功能强大的交易平台,以及屡获殊荣的客户支持,让您的交易更进一步

二十年稳健实力,成就值得信赖。

二十年专注打造极致交易体验。

自2006年起,致力缔造卓越的交易环境。

初学者

新手上路?

从基础知识入手,循序渐进,逐步建立交易信心。

中级交易者

让策略更进一步

使用先进的交易工具,获取更深入的市场洞察。

专业交易者

专业交易者专区

为专业投资者与高净值客户提供量身定制的专属服务。

每笔交易,尽享超值回馈

即刻查看我们的限时优惠

开始使用 GO Markets

无论你是市场新手还是全职交易,GO Markets 都有一个

根据您的需求量身定制的账户。

全球交易者共同的选择

自 2006 年起,GO Markets 已帮助全球数十万交易者实现他们的投资目标。凭借严格监管、以客户为本的服务,以及屡获殊荣的教育资源,我们始终是交易者值得信赖的合作伙伴。

*Trustpilot reviews are provided for the GO Markets group of companies and not exclusively for GO Markets Ltd.

*Awards were awarded to GO Markets group of companies and not exclusively to GO Markets Ltd.

探索更多 GO Markets 的产品与服务

差价合约市场

外汇、指数、股票、商品、贵金属、数字货币、ETF 等全品类交易,一站式管理。

交易平台与工具

尖端技术支持、优质客服团队、灵活资金管理,让您的交易更轻松。

学习中心

系统化学习交易技能与策略,培养稳健投资心态,助力长期稳健交易。

账户与定价

对比账户类型、查看点差,选择最适合您交易目标的方案。

GO Markets

让交易更进一步

探索上千种交易机会,享受专业机构水准的交易工具、流畅稳定的交易体验,以及屡获殊荣的客户支持。开户流程简单快捷,让您轻松开启交易之旅。

市场新闻与分析

用专业工具和市场分析助力您的每一步交易决策

上周的影响与广告一样重要。澳洲联储加息,美联储坚持加息,在有报道称以色列袭击伊朗南帕尔斯天然气田之前,市场几乎没有时间处理任何加息。

未来一周的央行决策将减少,但对市场可能同样重要。Flash PMI将首次广泛了解这场战争是否已经出现在商业信心中。澳大利亚2月份的消费者价格指数是对澳洲联储下一步行动最重要的国内数据点。而石油市场仍然是主要的宏观变量。

事实速览

- 在以色列首次袭击伊朗南帕尔斯天然气田后,布伦特原油价格飙升至每桶110美元以上。

- 澳大利亚、日本、欧元区、英国和美国的初步采购经理人指数均在周二公布。

- 澳大利亚2月份消费者价格指数周三公布,这是自澳洲联储连续加息以来的首次通胀数据。

石油:从危机到紧急情况

上周石油局势严重恶化。自2月28日战争爆发以来,布伦特原油已经飙升了约80%。

3月18日对伊朗南帕尔斯天然气田的袭击是上游石油和天然气基础设施首次成为攻击目标。

伊朗对袭击的回应是威胁要瞄准沙特阿拉伯、阿联酋和卡塔尔各地的设施。如果这些威胁中的任何一个得到实施,全球石油冲击将从供应中断升级为对该地区产能的直接攻击。

分析师现在表示,150美元的布伦特原油是可以实现的,200美元不在可能范围之内。1970年代的阿拉伯石油禁运导致价格翻了三番,高级能源主管已经用这些术语描述了当前的冲击。

对于本周的市场而言,石油是主要变量。任何停火、外交进展或恢复霍尔木兹航运的信号都可能引发油价的回调。伊朗对海湾基础设施的任何袭击都可能使它们走高。

监视器

- 通过霍尔木兹海峡的每日船只过境次数。

- 伊朗对海湾基础设施的报复,对沙特或阿联酋设施的袭击将是重大升级。

- 美国和欧洲的IEA储备何时以及如何进入市场。

- 卡塔尔南帕尔斯的中断正在影响欧洲液化天然气市场。

- 特朗普的言论可能导致盘中油价波动。

全球采购经理人指数快报:关于处于战争状态的经济的第一篇读物

周二同时公布了所有主要经济体3月份的标准普尔全球采购经理人指数初值估计。

这将是第一个记录制造商和服务公司如何应对超过100美元的石油、霍尔木兹海峡封锁以及中东战争造成的更广泛不确定性的数据集。

每个经济体的关键问题是,油价飙升和战争的不确定性是否削弱了商业信心,抑制了新订单或将投入价格指数推至多年来的新高。

鉴于在大多数经济体的调查窗口关闭之前,石油价格已突破100美元,因此投入成本读数可能会大幅上升。

关键日期

- 标普全球快报澳大利亚采购经理人指数: 澳大利亚东部夏令时间3月24日星期二上午9点

- 标普全球快报日本采购经理人指数: 澳大利亚东部夏令时间3月24日星期二上午11点30分

- 汇丰银行印度采购经理人指数简报: 澳大利亚东部夏令时间3月24日星期二下午 4:00

- HCOB Flash 法国采购经理人指数: 澳大利亚东部夏令时间3月24日星期二晚上 7:15

- HCOB Flash 德国采购经理人指数: 澳大利亚东部夏令时间3月24日星期二晚上 7:30

- HCOB 欧元区采购经理人指数简报: 澳大利亚东部夏令时间3月24日星期二晚上 8:00

- 标普全球快报英国采购经理人指数: 澳大利亚东部夏令时间3月24日星期二晚上 8:30

- 标普全球快报美国采购经理人指数: 澳大利亚东部夏令时间3月25日星期三上午12点45分

监视器

- 制造业和服务业中任何多年高点的输入价格组成部分。

- 衡量战争冲击在多大程度上削弱了前瞻预期的商业信心指数。

- 新订单是未来产出的指标;急剧下降可能预示着需求正在受到破坏。

- 美国综合采购经理人指数:已经是2月份主要经济体中最疲软的数据,另一个软数据可能会敲响增长的警钟。

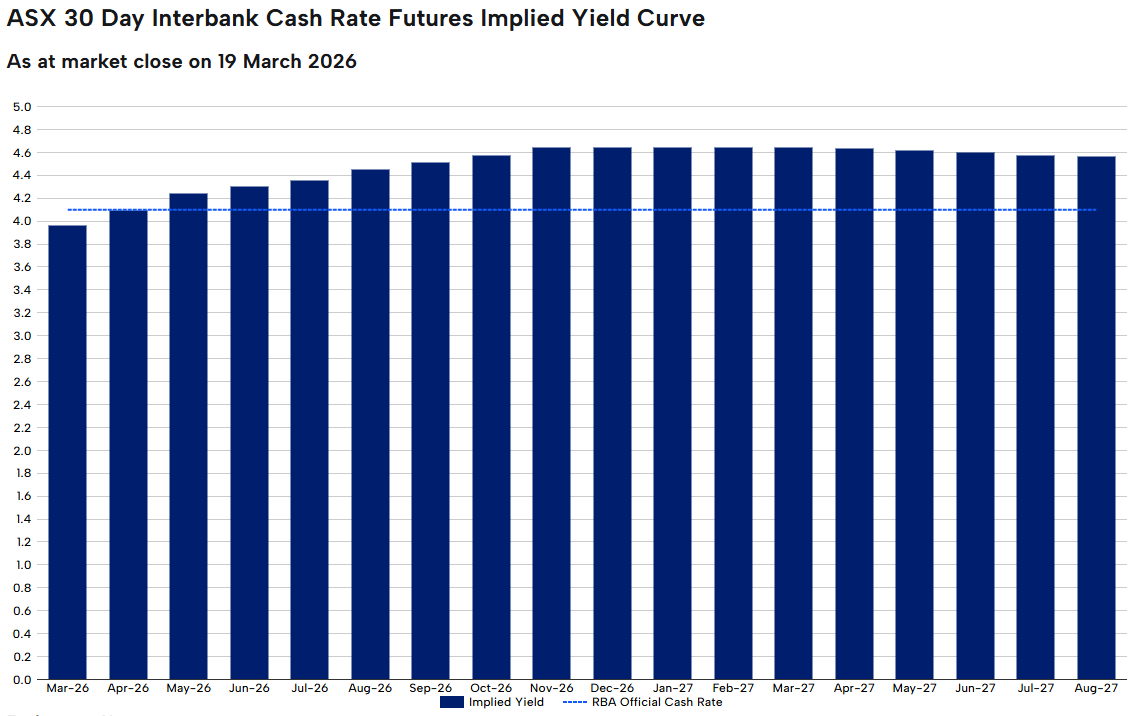

澳大利亚:又一次加息了吗?

澳洲联储于3月17日连续第二次会议上调,以5票对4票的微弱票数将现金利率提高至4.10%。

布洛克州长将其描述为一场 “非常活跃的讨论”,政策方向不成问题,只是时机问题。

本周将公布的2月份消费者价格指数作为反映任何石油冲击的第一手数据。扣除包括燃料在内的挥发性物质的调整后的均值将是澳洲联储最密切关注的数字。高于3.5%的读数可能会巩固5月份加息的理由。较为温和的结果可能会使暂停的论点死灰复燃。

澳新银行和澳大利亚国民银行都表示预计5月份将进行第三次加息,使现金利率达到4.35%。

关键日期

- ABS 消费者价格指数(CPI): 澳大利亚东部夏令时间3月25日星期三上午11点30分

监视器

- 削减后的平均通货膨胀率是澳洲联储的首选衡量标准。

- 可以将石油冲击与国内价格压力区分开来的燃料和能源成分。

- 住房和服务通货膨胀是推动澳洲联储长期担忧的粘性因素。

来源: ASX 澳洲联储利率追踪器

准备好在主要交易之外进行交易了吗?

开设一个账户 · 登录

亚洲在全球半导体供应中占据主导地位。横跨台湾、韩国和日本的五家公司正处于关键时刻 AI 扩建,控制从制造到使芯片成为可能的设备的所有方面。

事实速览

- 台积电在2024年实现了900亿美元的收入,毛利率为59%,股价在2025年增长了55%。

- 随着人工智能驱动的芯片测试需求激增,爱德万测试的股价在2025年翻了一番(+ 102%)。

- SK海力士是英伟达的主要HBM供应商,将其定位为人工智能加速器热潮的中心。

1。台湾半导体制造有限公司(TSM)

台积电是全球最大的合同芯片制造商,为苹果、英伟达、AMD和高通生产先进的半导体。作为一家纯粹的代工厂,它在5纳米(5nm)和3纳米(3nm)芯片生产方面处于领先地位,较小的节点正在开发中。

该公司公布的2024年收入为900亿美元,毛利率为59%,股本回报率为36%。

2025年,股票的总回报率为55%,分析师预测,在其1,000亿美元的美国扩张计划的支持下,2026年的收入将进一步增长约30%。

该公司面临的主要风险是其地缘政治风险,台海紧张局势仍然是该行业最受关注的尾部风险。

要看什么

- 美国扩张进展:与台积电在亚利桑那州的1000亿美元投资有关的任何延误、成本井喷或政治摩擦都可能打压市场情绪。

- 客户订单可见性:请留意苹果、英伟达或AMD关于芯片订单的任何最新指导,因为台积电的收入高度集中在少数客户身上。

- 地缘政治事态发展:无论基本面如何,台海紧张局势的任何升级都可能引发急剧走势。

- 下一节点斜坡:2纳米生产和良率的进展将是台积电保持其技术领先地位的关键信号。

2。三星电子 (KR: 005930)

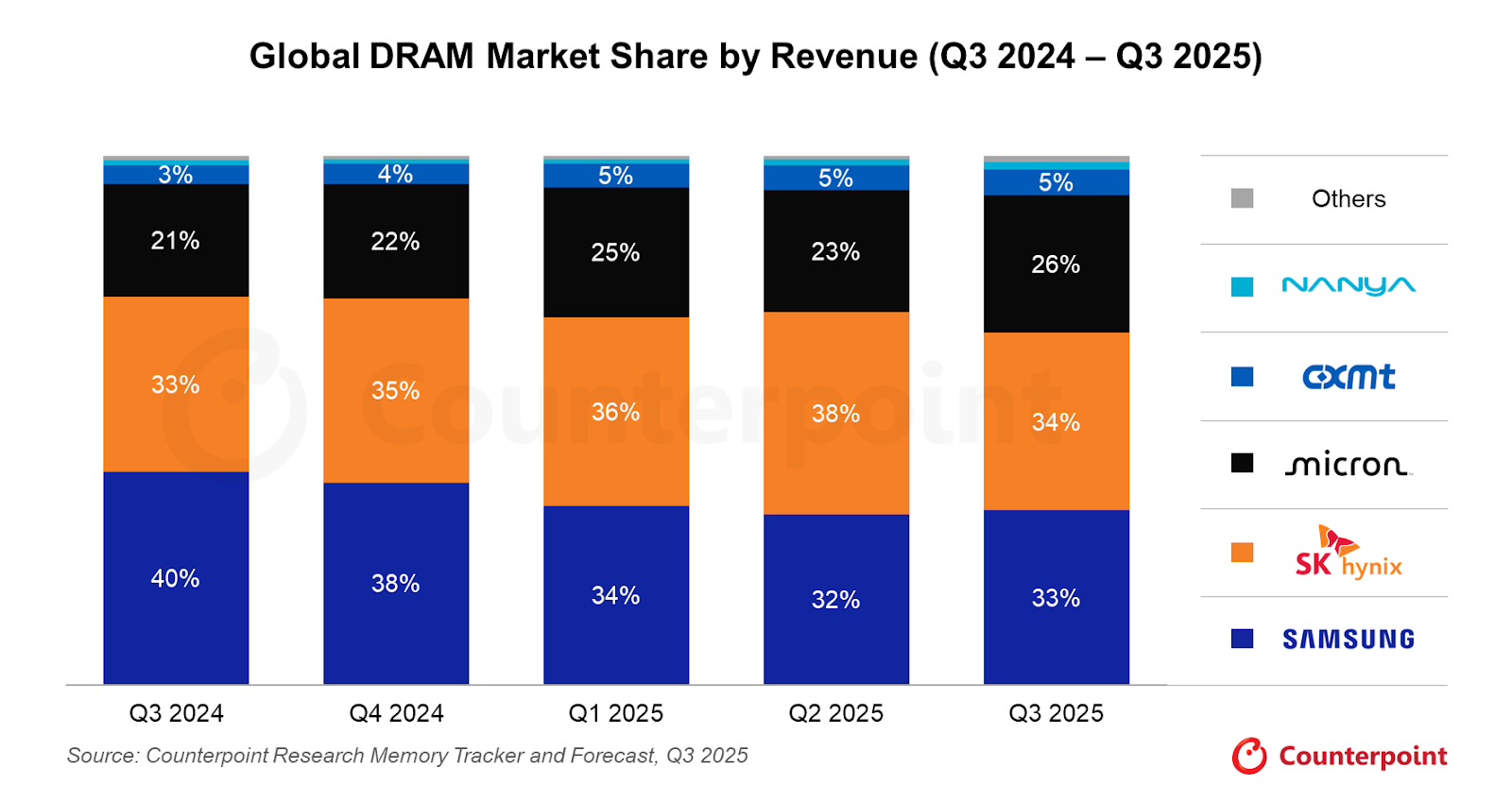

三星是全球为数不多的同时进行大规模设计和制造芯片的公司之一。它在DRAM、NAND闪存和逻辑芯片领域竞争,并且仍然是全球科技巨头的核心供应商。

三星的广泛范围是一种优势,但也是一种复杂性。其存储器部门面临库存周期带来的利润压力,而其代工业务在领先的收益率方面继续落后于台积电。

尽管HBM生产的执行速度比本地竞争对手海力士要慢,但人工智能驱动的内存热潮可能会带来不利影响。

要看什么

- HBM 资格认证进度:三星一直在努力使其的 HBM3E 芯片获得英伟达的认证。任何对重大供应中断的确认都可能是一个有意义的催化剂。

- 内存定价趋势:DRAM和NAND现货价格可能是三星利润率走势的指标。

- 提高铸造厂产量:三星的逻辑代工业务在高级节点的收益率方面一直处于困境;这里的任何可信进展都可能对该部门进行重新评估。

- 管理指导:在收益波动一段时间之后,资本支出计划和部门目标的明确性将受到密切关注。

3.爱德万测试 (ATEYY)

总部位于东京的Advantest生产用于验证芯片是否符合性能和质量标准的测试设备。

它向三星、英特尔、英伟达、高通和德州仪器供货,使其无论哪个代工厂赢得市场份额,都能从芯片行业的广泛增长中受益。

爱德万测试的股价在2025年翻了一番(+102%),并将截至2026年3月的年度的销售预测上调了21.8%,收益预期提高了70.6%。

要看什么

- 订单积压更新:在2025年强劲表现之后,爱德万测试待办事项的任何缩减都可能是一个预警信号。

- AI 芯片测试需求:随着芯片变得越来越复杂,每个芯片的测试时间也会增加。监控台积电和三星的人工智能加速器数量是否开始推动庞大的测试需求。

- FY2026 指南:下一次预测更新对于确认2025年的升级周期是否还有更长的路要走至关重要。

4。东京电子 (T: 8035)

东京电子是全球最大的半导体生产设备供应商之一,专门生产沉积、蚀刻和清洁工具。

包括台积电、三星和海力士在内的所有主要芯片制造商都依赖TEL的系统来扩大生产。

随着芯片制造商投资数十亿美元扩大产能,TEL的订单量不断增长。风险在于美国可能对向中国销售先进设备的出口限制,而中国仍然是该公司的主要收入领域之一。

要看什么

- 美国出口管制政策: 中国占TEL收入的很大一部分。任何收紧设备出口规定都是最直接的风险。

- 芯片制造商资本支出公告:台积电、三星和海力士2026年的资本支出计划直接转化为设备订单。任何削减都可能流入TEL的订单簿。

- 新的工具采用周期:监测 TEL 的下一代沉积和蚀刻工具是否被前沿晶圆厂采用。

5。SK 海力士 (KR: 000660)

SK 海力士是全球第二大存储芯片制造商,可以说是存储器领域最明显的人工智能时代受益者。

它是英伟达高带宽内存(HBM)芯片的主要供应商,高带宽存储器(H100和B200)等人工智能加速器中使用的专用内存。

HBM的需求推动了对SK海力士收入状况和市场地位的重大重新评级。进入2026年,人工智能基础设施支出几乎没有放缓的迹象,该公司的HBM特许经营权可能仍然是关键的差异化因素。

但是,产能限制以及三星和美光缩小HBM差距的风险是需要关注的主要问题。

要看什么

- Nvidia 的供应关系:英伟达的供应商结构向三星或美光的任何转变都可能是一个关键的风险事件。

- HBM4 开发: 下一代 HBM 的竞赛已经在进行中。请留意有关SK海力士HBM4准备情况的最新消息,以及它能否保持领先地位。

- 传统内存定价: SK 海力士仍然从标准 DRAM 和 NAND 中获得可观的收入。现货价格趋势可以衡量更广泛的存储周期。

底线

台积电、海力士、三星、爱德万测试和东京电子共同控制了人工智能建设的阻塞点。

人工智能基础设施的预期增长可能会支撑需求,但投资者应谨慎权衡风险。

地缘政治风险、美国的出口限制以及HBM的竞争步伐都可能起到推动作用。

准备好在主要交易之外进行交易了吗?

开设一个账户 · 登录

所以,事情是这样的...

如果你在过去的十年里一直在关注科技故事,那么你已经受过培训,可以研究北加州一块非常具体的、非常小的房地产。但是,当我们在2026年初坐在这里时,投资者的 “点滴连接” 时刻是:人工智能交易已不再是帕洛阿尔托闪亮的软件演示,而是开始关注计算的物理工业化。

发生了什么变化,为什么它很重要

我们已经进入 “证明之年”。全球最大的公司,即超大规模公司,预计今年将在资本支出上花费惊人的6,500亿美元。但这是大多数人错过的部分:那笔钱不是留在硅谷。它流向了爱达荷州、华盛顿州、科罗拉多州甚至海外的 “精挑细选” 玩家。

如果您想了解本财报季的实际投资回报率(ROI)可能达到何处,则必须将目光投向650区号之外。从人工智能炒作到人工智能工业化的转变正在改变地图。

Five companies · AI infrastructure play · 2026

The full AI stack: from capex to consulting

Infrastructure builders compared to the implementation bridge across the AI value chain

Hyperscaler CapEx: Early 2026 analyst estimates, midpoint of ranges. Amazon approx. 100% YoY, Alphabet approx. 100%, Meta approx. 87%, Microsoft approx. 50%.

Accenture: Cumulative advanced AI bookings $11.5B through Q1 FY2026. Q1 AI bookings $2.2B (up 76% YoY), AI revenue $1.1B (up 120% YoY) across 1,300+ clients.

五家公司塑造下一阶段的人工智能

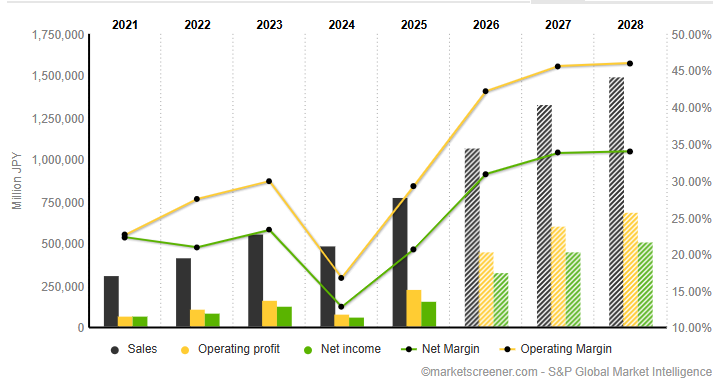

美光科技(MU),爱达荷州博伊西

美光是当前周期的 “存储器支柱”。当每个人都在关注芯片设计师时,许多人忽略了这样一个事实,即如果没有高带宽内存 (HBM),人工智能芯片的用处要小得多。一些分析师目前将美光视为强劲的买盘,因为据报道,到2026年底,其产能已售罄。随着存储周期达到某些人所说的强劲峰值,分析师还预计每股收益(EPS)将增长457%。

微软(MSFT),华盛顿州雷德蒙德

微软是这一转型的企业支柱。它已经超越了简单的聊天机器人,现在正在建造分析师所谓的 “情报工厂”。尽管该股最近因容量限制而面临压力,但据报道,对Azure AI的潜在需求仍超过容量。更广泛的牛市案例是,微软正在进入 “Agentic AI”,该系统不仅可以与用户交谈,还可以执行多步业务工作流程。

亚马逊(AMZN)、华盛顿州西雅图

亚马逊正在玩纵向整合的长期游戏。为了减少对昂贵的第三方硬件的依赖,它正在内部构建自己的人工智能芯片。亚马逊网络服务(AWS)仍然是盈利的主要驱动力,该公司正在利用其零售数据来训练许多硅谷初创企业可能难以复制的专业模型。

帕兰蒂尔科技(PLTR),科罗拉多州丹佛市

如果美光提供内存,微软提供平台,Palantir则为现代人工智能工厂提供 “操作系统”。该公司表现强劲,最近美国商业销售同比增长93%。它通常被描述为原始数据和企业盈利能力之间的桥梁,这仍然是投资者在2026年的主要关注点。

埃森哲(ACN),爱尔兰都柏林

你不能只是 “插入” 人工智能。企业经常需要围绕它重新设计流程,而这正是埃森哲的用武之地。

该公司被视为实施桥梁,一位分析师认为,“GenAI需要埃森哲” 从试点项目转向生产,尽管谨慎的角度是,人工智能的故事尚未让这里的投资者完全兴奋不已,因为咨询收入的出现可能比芯片销售更长。

接下来会发生什么?

该图表描绘了可能塑造下一阶段人工智能工业化交易的三个时间范围。

在短期内,市场仍在对芯片制造商的收益、指导以及任何产能紧张的迹象做出反应。在接下来的一个月中,注意力将转移到人工智能增长背后的现实世界投入上,尤其是电力、融资和基础设施。在60天窗口期之前,关键问题是人工智能支出是扩大到更广泛的市场重新评级,还是超过近期回报。

在这三个时期,重点都是一样的:证据。投资者正在寻找迹象,表明人工智能资本支出正在转化为对能源、土地和工业产能的实际需求。这就是为什么与电力和数据中心建设相关的公司的最新消息比以往任何时候都更加重要的原因。

Scenario planning · March 2026

What could happen next

Three time horizons, three scenarios to watch across the AI industrialisation cycle

Chipmaker reports

Possible

Market volatility continues as traders digest the latest reports from chipmakers like Micron

Upside scenario

"Bulletproof" guidance from remaining infrastructure names triggers a sector-wide relief rally

Watch for

Any mention of "capacity constraints" or "supply bottlenecks" in earnings calls

Energy and rates

Possible

Focus shifts to "real economy" energy players like NextEra that power the data centres

Downside scenario

Rising oil prices from Middle East conflict act as a tax on tech margins, rotating into defensives

Action point

Monitor Fed language on rates. Higher for longer makes $650B capex bills far more expensive to finance

The great dispersion

Possible

Market rewards companies with real AI revenue and punishes those still stuck in experimentation

Upside scenario

NextEra Energy (NEE) data centre announcements in late April/May trigger a utility renaissance rally

Downside scenario

An "air pocket" in profits occurs where debt-funded investment outpaces revenue gains

Watch

May reports from Texas Pacific Land (TPL) — is data centre land demand still "red hot"?

Action point

Review your portfolio for geographic diversity. The AI story is now a global power race

心理陷阱

许多交易者现在陷入的情感陷阱是近期偏见。你已经看到 NVIDIA 和 “Magnificent 7” 获胜了很长时间,感觉他们是玩这个游戏的唯一途径。但是,“显而易见” 的交易通常是已经定价的交易。在采取行动之前,问问自己:“我买入这只股票是因为我了解它在物理人工智能供应链中的作用,还是因为我害怕错过两年前开始的涨势的下一站?”

准备好在主要交易之外进行交易了吗?

开设一个账户 · 登录

免责声明: 此内容仅为一般信息,不应作为个人理财建议或购买、出售或持有任何金融产品的推荐。提及公司或主题,包括与人工智能相关的股票,仅供参考。股票和衍生品市场可能会大幅波动,而人工智能和技术等集中的行业可能会面临更高的波动性、估值风险和流动性风险。如果您交易差价合约等衍生品,杠杆可以放大收益和亏损。过去的表现不是未来表现的可靠指标。