Trading FOREX, equities, commodities, and any other asset can be an emotional rollercoaster. With so many different emotions and external factors difficulties impacting a trade, it is crucial that before any trade is executed a trading plan is produced to minimise the impact of the ‘noise’. Generating the Idea The first step to any plan is to generate a trading idea.

Trade ideas, come from one of three sources. A fundamental source, a technical source, or a mix of both. What does this mean exactly?

Well, when generating ideas from a fundamental perspective, a trader can generate idea based on economic events, monetary policy from a Central bank or company relevant information just to name a few. From a technical perspective, a trader may find that an asset is trading near a potential support or resistance level or developing into a breakout pattern. Alternatively, the price may have touched an important moving average which indicates it may be ready to trade.

Traders can also put these ideas together to come up with even more robust trading ideas. Background economic factors and sector analysis Before entering a trade, a good trader should have at the very least a rudimentary understanding of the relevant sector or economic factors that may influence the trade. For example, a trader decides to trade the AUDUSD currency pair.

The trader has seen that the price is approaching a short-term support point and decides to buy the pair expecting the price to bounce of the level. However, the trader is not aware that the Federal Reserve has just increased interest rates which has increased the value of the USD. Consequently, the price goes against the trader.

Technical breakdown Prior to entering any trade, the trader should analyse the price chart and set up relevant support and resistance levels. This allows the trader to have a clear idea of key supply and demand zones for the asset before the emotions of the actual trade become prevalent. To effectively go about this step, support and resistance levels can be analysed on multiple time frames to gain an even greater edge. [caption id="attachment_272243" align="alignnone" width="2560"] Business Team Investment Entrepreneur Trading discussing and analysis graph stock market trading,stock chart concept[/caption] Entry condition Having a trade idea is one aspect however having a clear entry criterion will help reduce the impact of emotion when watching the trade unfold.

Some examples of potential entries conditions can be related to a break and retest of a certain level for an entry or waiting for a specific candlestick pattern. Furthermore, an entry may also be defined by a disproportionate increase in volume supporting a breakout. Exit Conditions Like determining entry conditions having pre planned exit points can improve the management of emotions during also trade whilst also enhancing risk management.

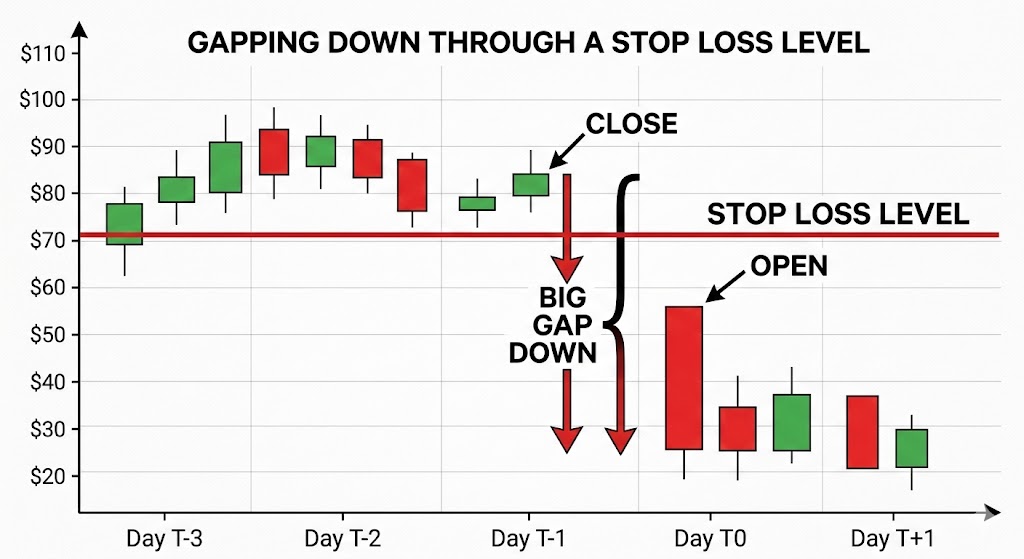

Setting take profit targets/stop loss areas will help ensure that a trade is well structured even before initiating the trade. Having pre-determined exit points can also help determine if a trade is worth entering in the first place as it allows for a determination of the potential risk reward before execution. Risk management No matter whether the trade is a scalp, swing trade or longer-term investment, each should have clear risk management guidelines.

Good risk management involves the use of stop losses and correct sizing of a trade. One method that can be effective is to have a maximum amount of the total account that you are willing to lose per trade. This could be a percentage figure or a fixed amount.

For example, if the total account size is $10,000 and you decide that the maximum loss per trade is 1%. This means that the maximum loss per trade would be $100. The next step is to then set stop loss.

The stop loss in many cases should be independent of the actual maximum risk amount. The stop loss level should be calculated before the sizing. Once the stop loss is set the size of the trade can be determined.

Risk management is perhaps the most crucial element of the trading plan because minimising losses is crucial to any long-term success in trading. Whilst having a clear trading plan will not guarantee success it will help remove many behavioral biases that can impact on a trade.

Disclaimer: Articles are from GO Markets analysts and contributors and are based on their independent analysis or personal experiences. Views, opinions or trading styles expressed are their own, and should not be taken as either representative of or shared by GO Markets. Advice, if any, is of a ‘general’ nature and not based on your personal objectives, financial situation or needs. Consider how appropriate the advice, if any, is to your objectives, financial situation and needs, before acting on the advice.