Markets move into the week ahead with inflation data across Australia and Japan, alongside elevated geopolitical tensions that continue to influence energy prices and broader risk sentiment.

- Australia Consumer Price Index (CPI): Inflation data may influence the Reserve Bank of Australia (RBA) policy path, with the Australian dollar (AUD) and local yields sensitive to any surprise.

- Japan data cluster: Tokyo CPI (preliminary) plus industrial production and retail sales provide an inflation-and-activity pulse that could shape Bank of Japan (BoJ) normalisation expectations.

- Eurozone & Germany CPI: Flash inflation readings will test the disinflation narrative and influence ECB rate-cut timing expectations.

- Oil and geopolitics: Brent crude has posted its highest close since 8 August 2025 amid renewed Middle East tensions, reinforcing energy-driven inflation risk.

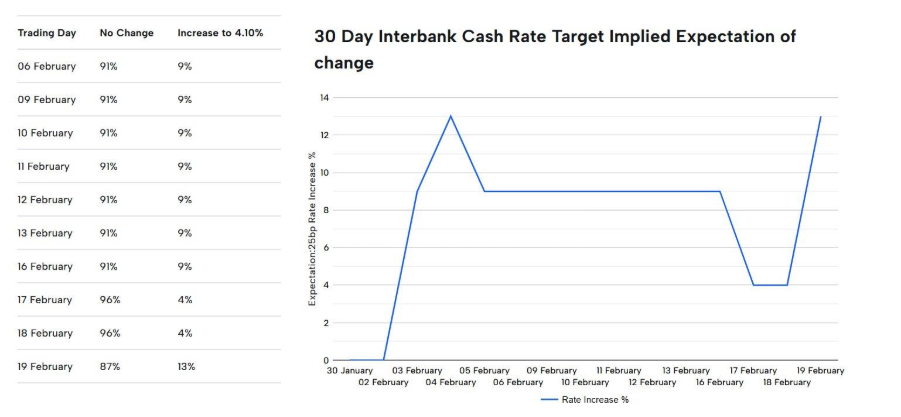

Australia CPI: RBA expectations to change?

Australia’s upcoming CPI release will be closely watched for signals on whether inflation is stabilising or proving more persistent than expected.

A stronger-than-expected print could be associated with higher yields and a firmer AUD as rate expectations adjust. A softer outcome could support expectations for a steadier policy stance.

Key dates

- Inflation Rate (MoM): 11:30 am Wednesday, 25 February (AEDT)

- CPI: 11:30 am Wednesday, 25 February (AEDT)

Monitor

- AUD volatility around the release.

- Local bond yield reactions.

- Interest rate pricing shifts.

Japan inflation and growth data

Japan’s late-week releases combine Tokyo CPI (preliminary) with industrial production and retail sales, offering a broader read on price pressures and domestic demand.

Tokyo CPI is often watched as a timely signal for national inflation dynamics and BoJ debate. Industrial output and retail spending add context on activity.

Surprises across this cluster can drive sharp moves in the JPY, particularly if results shift perceptions around the pace and persistence of BoJ normalisation.

Key dates

- Tokyo CPI: 10:30 am Friday, 27 February (AEDT)

- Industrial Production: 10:50 am Friday, 27 February (AEDT)

- Retail Sales: 10:50 am Friday, 27 February (AEDT)

Monitor

- JPY sensitivity to inflation surprises

- Bond yield moves in response to activity data

- Equity reactions if growth momentum expectations shift

Energy and safe-haven flows

Oil prices have climbed to their highest close since 8 August 2025 amid renewed Middle East tensions.

Recent reporting on heightened regional military activity and shipping-risk headlines near the Strait of Hormuz has reinforced energy security as a market focus. The Strait of Hormuz remains a widely watched chokepoint for global energy flows.

Higher oil prices can feed into inflation expectations and influence bond yields. At the same time, geopolitical uncertainty can support the USD through safe-haven demand and relative rate positioning.

Monitor

- Brent crude price levels

- USD strength versus major currencies

- Yield movements as inflation risk premiums adjust

Eurozone and Germany inflation

Flash inflation readings from Germany and the broader eurozone (HICP) will test whether the region’s disinflation trend remains intact.

Germany’s release can influence expectations ahead of the aggregated eurozone figure. If core inflation proves sticky, expectations around the timing and pace of potential European Central Bank easing could shift.

Key dates

- Germany Inflation Rate: 12:00 am Saturday, 28 February (AEDT)

Monitor

- EUR volatility around inflation releases

- European sovereign bond yields

- Rate-cut probability adjustments

Key economic events

Disclaimer: Articles are from GO Markets analysts and contributors and are based on their independent analysis or personal experiences. Views, opinions or trading styles expressed are their own, and should not be taken as either representative of or shared by GO Markets. Advice, if any, is of a ‘general’ nature and not based on your personal objectives, financial situation or needs. Consider how appropriate the advice, if any, is to your objectives, financial situation and needs, before acting on the advice.