Markets retreated last week, pulling back about 2.5-3% from record levels. While the decline is modest, it is marked by several headwinds that could create further pressure this week.

Government Shutdown Reaches Historic Length

The ongoing shutdown has now reached record duration, and there's still no clear resolution in sight. Healthcare remains the primary sticking point between the two sides. Some reports suggest potential progress, but the jury's still out on whether any deal will materialise or gain bipartisan support before the Thanksgiving holiday season.

Key Economic Data May Be Delayed

The shutdown's impact extends to data releases. Market-influencing government reports, including jobs numbers and CPI data, may be delayed this week — CPI is still technically scheduled, but the shutdown could affect its release. This data delay will make it harder to gauge the economy's true direction and could inject further volatility into markets.

Earnings Season Continues to Impress

Despite these macro headwinds, corporate America is delivering exceptional results. We're seeing an 82% EPS beat rate and 77% of companies exceeding revenue expectations. While we're in the final 10% of S&P 500 reports, some important retail stocks are still due. These consumer-facing companies could provide valuable insights into spending patterns and economic health.

NVIDIA Tests Critical Support Level

AI stocks are facing pressure, with NVIDIA testing a key technical level around $180-$185. The stock experienced five consecutive days of losses before bouncing strongly on Friday with a major wick rejection. If support at $180 breaks, we could see a drop to $165. However, Friday's bounce suggests a possible retest of $193. This is a crucial moment for the AI sector leader, and its direction could influence broader tech sentiment.

Market Insights

Watch the latest video from Mike Smith for the week ahead in markets.

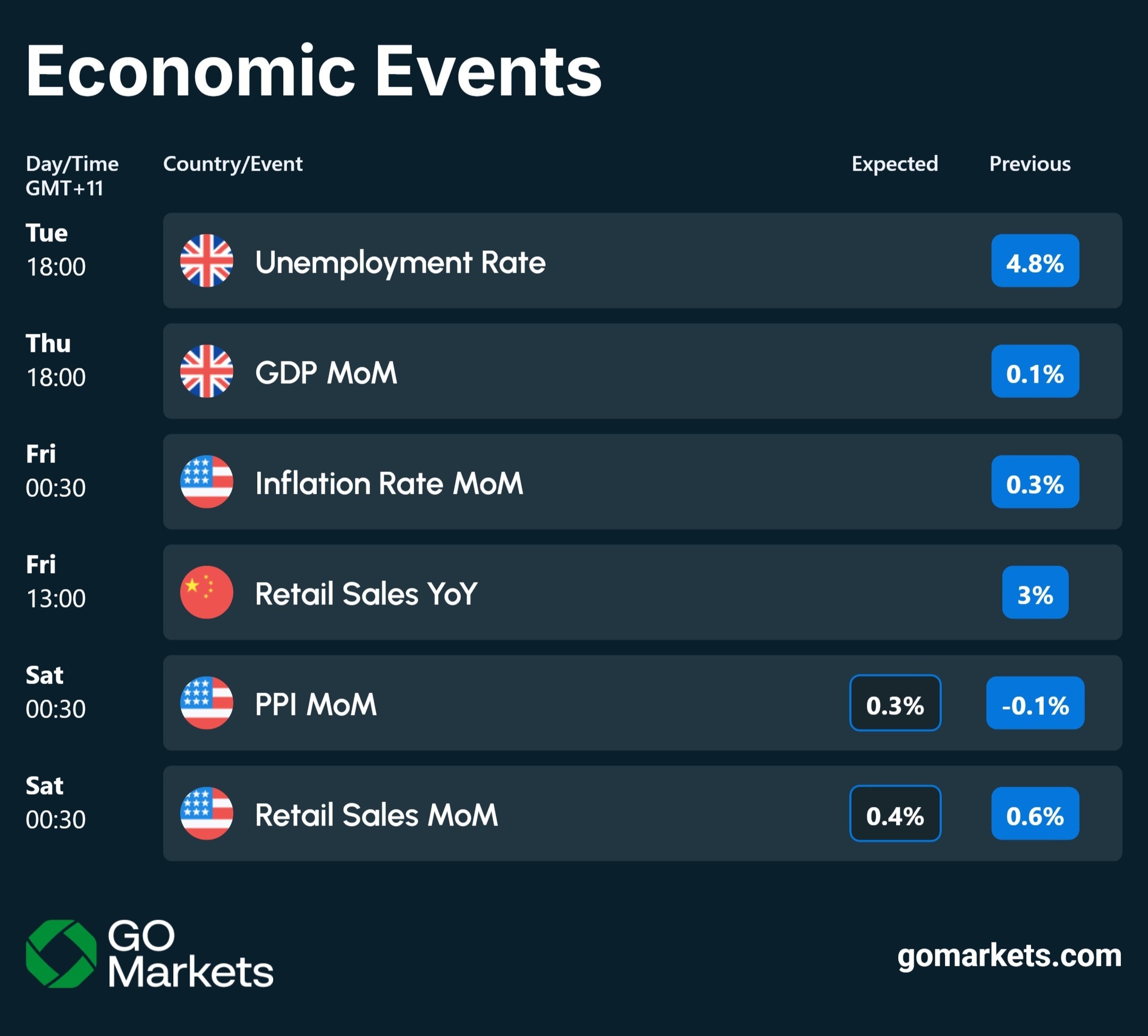

Key economic events

Keep up to date with the upcoming economic events for the week.

The information provided is of general nature only and does not take into account your personal objectives, financial situations or needs. Before acting on any information provided, you should consider whether the information is suitable for you and your personal circumstances and if necessary, seek appropriate professional advice. All opinions, conclusions, forecasts or recommendations are reasonably held at the time of compilation but are subject to change without notice. Past performance is not an indication of future performance. Go Markets Pty Ltd, ABN 85 081 864 039, AFSL 254963 is a CFD issuer, and trading carries significant risks and is not suitable for everyone. You do not own or have any interest in the rights to the underlying assets. You should consider the appropriateness by reviewing our TMD, FSG, PDS and other CFD legal documents to ensure you understand the risks before you invest in CFDs. These documents are available here.

免责声明:文章来自 GO Markets 分析师和参与者,基于他们的独立分析或个人经验。表达的观点、意见或交易风格仅代表作者个人,不代表 GO Markets 立场。建议,(如有),具有“普遍”性,并非基于您的个人目标、财务状况或需求。在根据建议采取行动之前,请考虑该建议(如有)对您的目标、财务状况和需求的适用程度。如果建议与购买特定金融产品有关,您应该在做出任何决定之前了解并考虑该产品的产品披露声明 (PDS) 和金融服务指南 (FSG)。

.jpg)