Three data levers dominate the US markets in February: growth, labour and inflation. Beyond those, policy communication, trade headlines and geopolitics can still matter, even when they are not tied to a scheduled release date.

Growth: business activity and trade

Early to mid-month indicators provide a read on whether US momentum is stabilising or softening into Q1.

Key dates

- Advance monthly retail sales: 10 Feb, 8:30 am (ET) / 11 Feb, 12:30 am (AEDT)

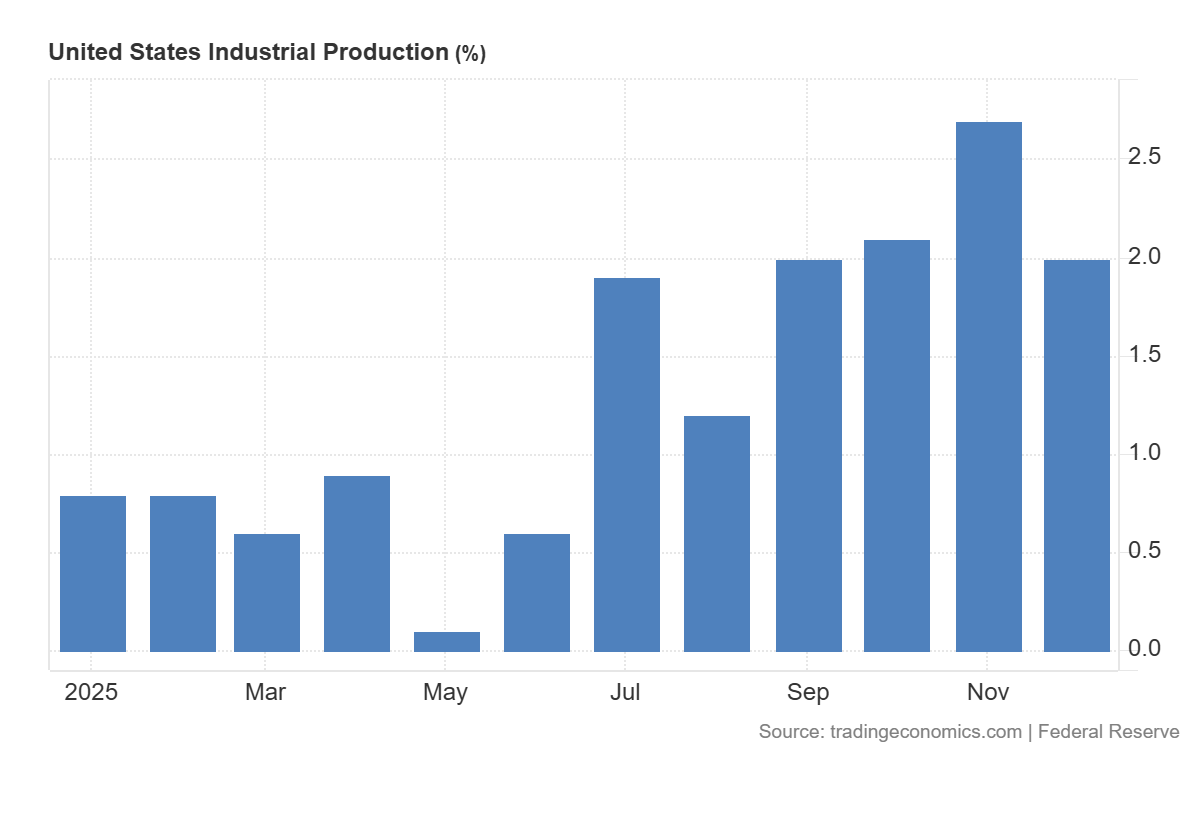

- Industrial Production and Capacity Utilisation: 18 Feb, 9:15 am (ET) / 19 Feb, 1:15 am (AEDT)

- International Trade in Goods and Services: 19 Feb, 8:30 am (ET) / 20 Feb, 12:30 am (AEDT)

What markets look for

Markets will be watching new orders and output trends in PMIs to gauge underlying demand momentum. Export and import data will offer insights into global trade flows and domestic consumption patterns. Traders will also assess whether manufacturing and services sectors remain in expansionary territory or show signs of contraction.

Market sensitivities

- Stronger growth can be associated with higher yields and a firmer USD, though inflation and policy expectations often dominate the rate response.

- Softer activity can be associated with lower yields and improved risk appetite, depending on inflation, positioning, and broader risk conditions.

Payrolls data

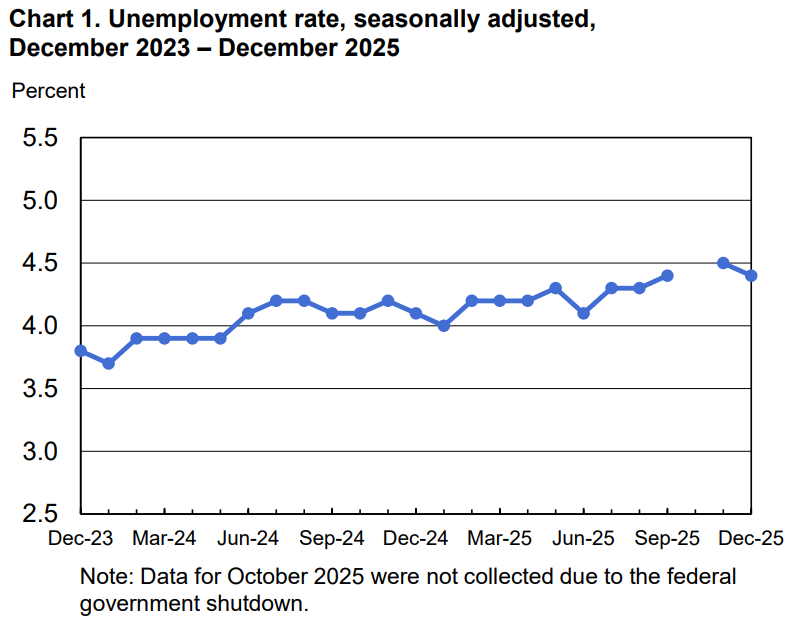

Labour conditions remain a direct input into rate expectations. The monthly NFP report, alongside the weekly jobless claims released every Thursday, is typically watched for signs of cooling or renewed tightness.

Key dates

- Employment Situation (nonfarm payrolls, unemployment, wages): 6 Feb, 8:30 am (ET) / 7 Feb, 12:30 am (AEDT)

What markets look for

Markets will focus on headline payrolls to assess the pace of job creation, the unemployment rate for signals of labour market slack, and average hourly earnings as a gauge of wage pressures. A gradual cooling can support the idea that wage pressures are easing. Persistent tightness may push out expectations for policy easing.

Market sensitivities

Payroll surprises frequently move Treasury yields and the USD quickly, with knock-on effects for equities and commodities.

Inflation: CPI, PPI and PCE

Inflation releases remain a key input into expectations for the Fed’s policy path.

Key dates

- Consumer Price Index (CPI): 11 Feb, 8:30 am (ET) / 12 Feb, 12:30 am (AEDT)

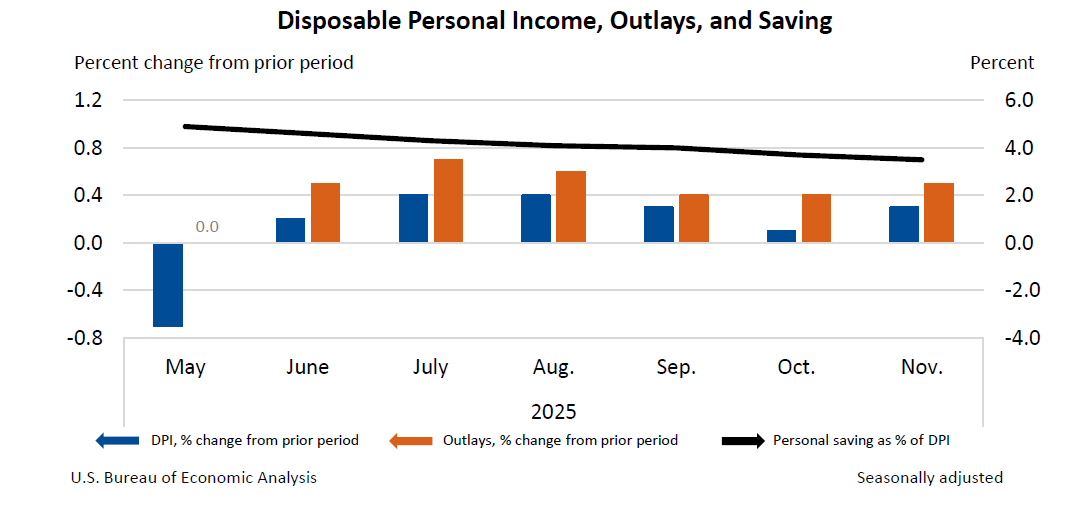

- Personal Income and Outlays, including the PCE price index): 20 Feb, 8:30 am (ET) / 21 Feb, 12:30 am (AEDT)

- Producer Price Index (PPI): 27 Feb, 8:30 am (ET) / 28 Feb, 12:30 am (AEDT)

What markets look for

Producer prices can act as a pipeline signal. CPI and the PCE price index can help confirm whether inflation pressures are broadening or fading at the consumer level.

How rates and the USD can react

- Cooling inflation can support lower yields and a softer USD, though market reactions can vary.

- Sticky inflation can keep upward pressure on yields and financial conditions, especially if it shifts policy expectations.

Other influencing factors

Policy and communication

There is no scheduled February FOMC meeting, but speeches and other Fed communication, as well as the minutes cycle from prior meetings, can still influence expectations around the policy path. Without a decision event, markets often react to shifts in tone, or renewed emphasis on inflation persistence and labour conditions.

Trade and geopolitics

Trade flows and energy markets can remain secondary, and the risk profile is typically headline-driven rather than linked to scheduled releases.

The Office of the United States Trade Representative has published fact sheets and policy updates (including on US-India trade engagement) that may occasionally influence sector and supply-chain sentiment at the margin, depending on the substance and market focus at the time.

Separately, volatility tied to Middle East developments and any impact on energy pricing can filter into inflation expectations and bond yields. Weekly petroleum market data from the US Energy Information Administration is one input that markets often monitor for near-term signals.

Disclaimer: Articles are from GO Markets analysts and contributors and are based on their independent analysis or personal experiences. Views, opinions or trading styles expressed are their own, and should not be taken as either representative of or shared by GO Markets. Advice, if any, is of a ‘general’ nature and not based on your personal objectives, financial situation or needs. Consider how appropriate the advice, if any, is to your objectives, financial situation and needs, before acting on the advice. If the advice relates to acquiring a particular financial product, you should obtain our Disclosure Statement (DS) and other legal documents available on our website for that product before making any decisions.