Llega más lejos con GO Markets

Opera de forma más inteligente con un bróker global de confianza. Spreads bajos, ejecución rápida, sin comisiones por depósito, plataformas potentes y soporte al cliente galardonado.

20 Años de Solidez

Celebramos 20 años de excelencia en trading.

Diseñado para traders desde 2006.

Para principiantes

¿Estás

empezando?

Explora los fundamentos y gana confianza.

Para traders intermedios

Lleva tu estrategia

al siguiente nivel

Accede a herramientas avanzadas para obtener perspectivas más profundas que nunca.

Profesionales

Para traders

profesionales

Descubre nuestra oferta especializada para traders de alto volumen e inversionistas sofisticados.

Obtenga más de cada operación

Explora nuestras ofertas especiales por tiempo limitado

Get Started with GO Markets

Whether you’re new to markets or trading full time, GO Markets has an

account tailored to your needs.

Con la confianza de traders en todo el mundo

Desde 2006, GO Markets ha ayudado a cientos de miles de traders a alcanzar sus objetivos de trading con confianza y precisión, todo ello respaldado por una regulación sólida, un servicio centrado en el cliente y una Educación galardonada.

*Trustpilot reviews are provided for the GO Markets group of companies and not exclusively for GO Markets Ltd.

*Awards were awarded to GO Markets group of companies and not exclusively to GO Markets Ltd.

Explora más de GO Markets

Mercado de CFD

Opera con CFDs en forex, índices, acciones, materias primas, metales, ETF y más.

Plataformas & herramientas

Cuentas de trading con tecnología sin complicaciones, soporte al cliente galardonado y acceso fácil a opciones de fondeo flexibles.

Academia

Aprende las habilidades, estrategias y mentalidad detrás del éxito en el trading a largo plazo.

Cuentas & tarifas

Compara tipos de cuenta, consulta los spreads y elige la opción que se adapte a tus objetivos.

Llega más lejos con GO Markets

Explore miles de oportunidades de negociación con herramientas de nivel institucional, ejecución fluida y Soporte galardonado. Abrir una cuenta es rápido y fácil.

Noticias & análisis

Herramientas potentes para todos los estilos y preferencias de trading.

La semana pasada fue tan consecuente como se anunciaba. El RBA subía, la Fed se mantuvo y los mercados apenas tuvieron tiempo de procesar nada antes de que surgieran informes de que Israel había atacado el campo de gas South Pars de Irán.

La próxima semana trae menos decisiones de los bancos centrales, pero puede ser igual de importante para los mercados. Los PMI Flash ofrecerán la primera lectura amplia sobre si la guerra ya se está mostrando en la confianza empresarial. El IPC de febrero de Australia es el punto de datos interno que más importa para el próximo movimiento del RBA. Y el mercado petrolero sigue siendo la macro variable dominante.

Datos rápidos

- El crudo Brent se repuntó por encima de 110 dólares por barril después de que Israel atacara por primera vez el campo de gas South Pars de Irán.

- Los PMI flash para Australia, Japón, la eurozona, Reino Unido y Estados Unidos aterrizan todos el martes.

- El IPC de febrero de Australia aterriza el miércoles, la primera lectura de inflación desde las alzas del RBA de forma posterior.

Petróleo: De la crisis a la emergencia

La situación petrolera se deterioró significativamente la semana pasada. El crudo Brent ahora ha aumentado aproximadamente un 80% desde que comenzó la guerra el 28 de febrero.

El ataque del 18 de marzo en el campo de gas South Pars de Irán fue la primera vez que la infraestructura de petróleo y gas aguas arriba ha sido atacada.

Irán respondió al ataque amenazando con atacar instalaciones en Arabia Saudita, Emiratos Árabes Unidos y Qatar. Si se ejecuta alguna de estas amenazas, el shock petrolero mundial escalaría de una interrupción del suministro a un ataque directo a la capacidad de producción de la región.

Analistas ahora dicen que el Brent de 150 dólares es alcanzable y 200 dólares no está fuera del ámbito de la posibilidad. El embargo petrolero árabe de la década de 1970 resultó en una cuadruplicación de los precios, y el choque actual ya está siendo descrito en esos términos por altos ejecutivos energéticos.

Para los mercados de esta semana, el petróleo es la variable dominante. Cualquier señal de alto el fuego, progreso diplomático o reanudación del transporte marítimo Ormuz probablemente podría desencadenar una corrección en los precios del petróleo. Cualquier ataque iraní contra la infraestructura del Golfo podría enviarlos más altos.

Monitorear

- Números diarios de tránsito de embarcaciones por el Estrecho de Ormuz.

- Las represalias iraníes contra la infraestructura del Golfo, un ataque a las instalaciones saudíes o de los Emiratos Árabes Unidos serían una escalada importante.

- Cuándo y cómo las reservas de la AIE americanas y europeas llegan al mercado.

- La interrupción de Qatar en South Pars está afectando al mercado europeo de GNL.

- Declaraciones de Trump que podrían causar movimiento intradiario del precio del petróleo.

PMIs Flash globales: La primera lectura sobre una economía en guerra

El martes entrega las estimaciones del PMI flash de S&P Global para marzo en todas las principales economías simultáneamente.

Este será el primer conjunto de datos para capturar cómo los fabricantes y las empresas de servicios están respondiendo al petróleo de más de 100 dólares, el bloqueo del Estrecho de Ormuz y la incertidumbre más amplia creada por la guerra en el Medio Oriente.

La pregunta clave para cada economía es si el aumento del precio del petróleo y la incertidumbre de la guerra han hecho mermas la confianza empresarial, suprimido nuevos pedidos o empujado los índices de precios de los insumos a nuevos máximos multianuales.

Dado que el petróleo cruzó los 100 dólares antes de que se cerrara la ventana de la encuesta para la mayoría de las economías, las lecturas de costos de insumos podrían elevarse significativamente.

Fechas clave

- PMI de S&P Global Flash Australia: martes 24 marzo, 9:00 a.m. AEDT

- PMI de S&P Global Flash Japón: martes 24 marzo, 11:30 h AEDT

- PMI de HSBC Flash India: martes 24 marzo, 16:00 AEDT

- HCOB Flash Francia PMI: martes 24 marzo, 19:15 AEDT

- HCOB Flash Alemania PMI: martes 24 marzo, 19:30 AEDT

- HCOB Flash PMI de la Eurozona: martes 24 marzo, 8:00pm AEDT

- PMI del Reino Unido de S&P Global Flash: martes 24 marzo, 20:30 h AEDT

- S&P Global Flash PMI de EE. UU.: miércoles 25 marzo, 12:45 AEDT

Monitorear

- Componentes de precios de entrada para cualquier máximo de varios años en la fabricación y los servicios.

- Índices de confianza empresarial sobre cuánto el shock bélico ha hecho mermas en las expectativas.

- Nuevos pedidos como indicador de la producción futura; una fuerte caída podría indicar que la destrucción de la demanda está en marcha.

- PMI compuesto estadounidense: ya la más débil de las principales economías en febrero, otra lectura suave podría levantar las campanas de alarma del crecimiento.

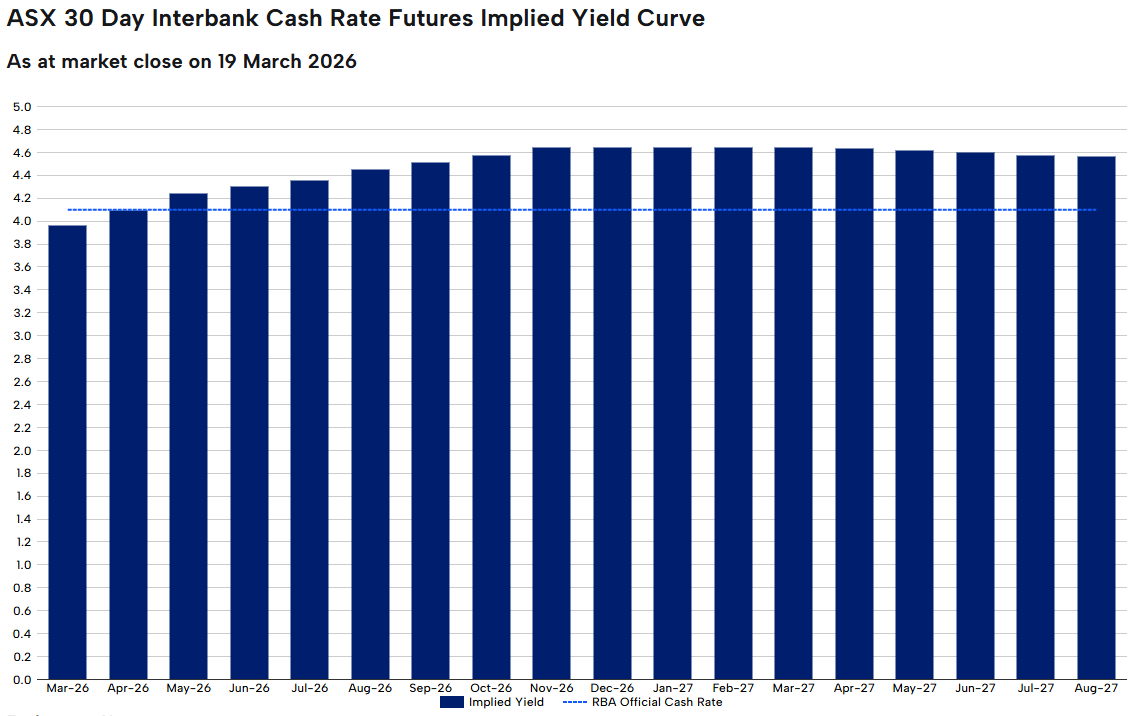

Australia: ¿Se acerca otra subida?

El RBA se elevó para la segunda reunión consecutiva el 17 de marzo, elevando la tasa de efectivo a 4.10% en una estrecha votación de 5-4.

El gobernador Bullock lo describió como una “discusión muy activa” donde no se cuestionaba la dirección de la política, solo el momento.

Esta semana verá la liberación del IPC de febrero como la primera lectura para capturar cualquiera de los choques petroleros. El promedio recortado, que quita elementos volátiles incluido el combustible, será el número que el RBA observa más de cerca. Una lectura superior al 3.5% podría cimentar el caso de una alza en mayo. Un resultado más suave podría revivir el argumento para una pausa.

ANZ y NAB han declarado expectativas de una tercera alza en mayo, llevando la tasa de efectivo a 4.35%.

Fechas clave

- Índice de Precios al Consumidor (IPC) ABS: miércoles 25 marzo, 11:30 h AEDT

Monitorear

- La inflación media recortada como la medida preferida del RBA.

- Componentes de combustible y energía que podrían separar el choque petrolero de la presión interna de los precios.

- La inflación de vivienda y servicios como componentes pegajosos que impulsan la preocupación a largo plazo del RBA.

Fuente: RBA rastreador de tasa ASX

¿Listo para comerciar más allá de las mayores?

Abrir una cuenta · Iniciar sesión

Asia domina la oferta mundial de semiconductores. Cinco empresas, que abarcan Taiwán, Corea del Sur y Japón, se sientan en la coyuntura crítica del Construcción de IA, controlando todo, desde la fabricación hasta el equipo que hace posibles los chips.

Datos rápidos

- TSMC entregó 90 mil millones de dólares en ingresos en 2024, con un margen bruto del 59% y las acciones subiendo 55% en 2025.

- Las acciones de Advantest se duplicaron (+102%) en 2025 a medida que aumentó la demanda de pruebas de chips impulsadas por IA.

- SK Hynix es el principal proveedor de HBM de Nvidia, posicionándolo en el centro del boom del acelerador de IA.

1. Taiwán Semiconductor Manufacturing Co. (TSM)

TSMC es el mayor fabricante de chips por contrato del mundo, produciendo semiconductores avanzados para Apple, Nvidia, AMD y Qualcomm. Al ser una fundición de juego puro, lidera en la producción de chips de 5 nanómetros (5nm) y 3 nanómetros (3nm), con nodos más pequeños en desarrollo.

La compañía registró 90 mil millones de dólares en ingresos para 2024 con un margen bruto de 59% y 36% de retorno sobre el capital.

Las acciones arrojaron un retorno total del 55% en 2025, y los analistas pronosticaron un aumento adicional de ~ 30% en los ingresos en 2026, apuntalado por su programa de expansión de 100 mil millones de dólares en Estados Unidos.

El riesgo clave para la compañía es su exposición geopolítica, y las tensiones del Estrecho de Taiwán siguen siendo el riesgo de cola más visto del sector.

Qué ver

- Progreso de expansión en Estados Unidos: Cualquier retraso, reventada de costos o fricción política con respecto a la inversión de TSMC en Arizona de 100 mil millones de dólares podría pesar sobre el sentimiento.

- Visibilidad de pedidos del cliente: Esté atento a las actualizaciones de orientación de Apple, Nvidia o AMD sobre pedidos de chips, ya que los ingresos de TSMC están altamente concentrados entre un puñado de clientes.

- Evolución geopolítica: Cualquier escalada de las tensiones en el Estrecho de Taiwán podría desencadenar movimientos bruscos independientemente de los fundamentos.

- Rampa de siguiente nodo: El progreso en la producción de 2 nm y las tasas de rendimiento serán una señal clave para la capacidad de TSMC para mantener su liderazgo tecnológico.

2. Samsung Electronics (KR:005930)

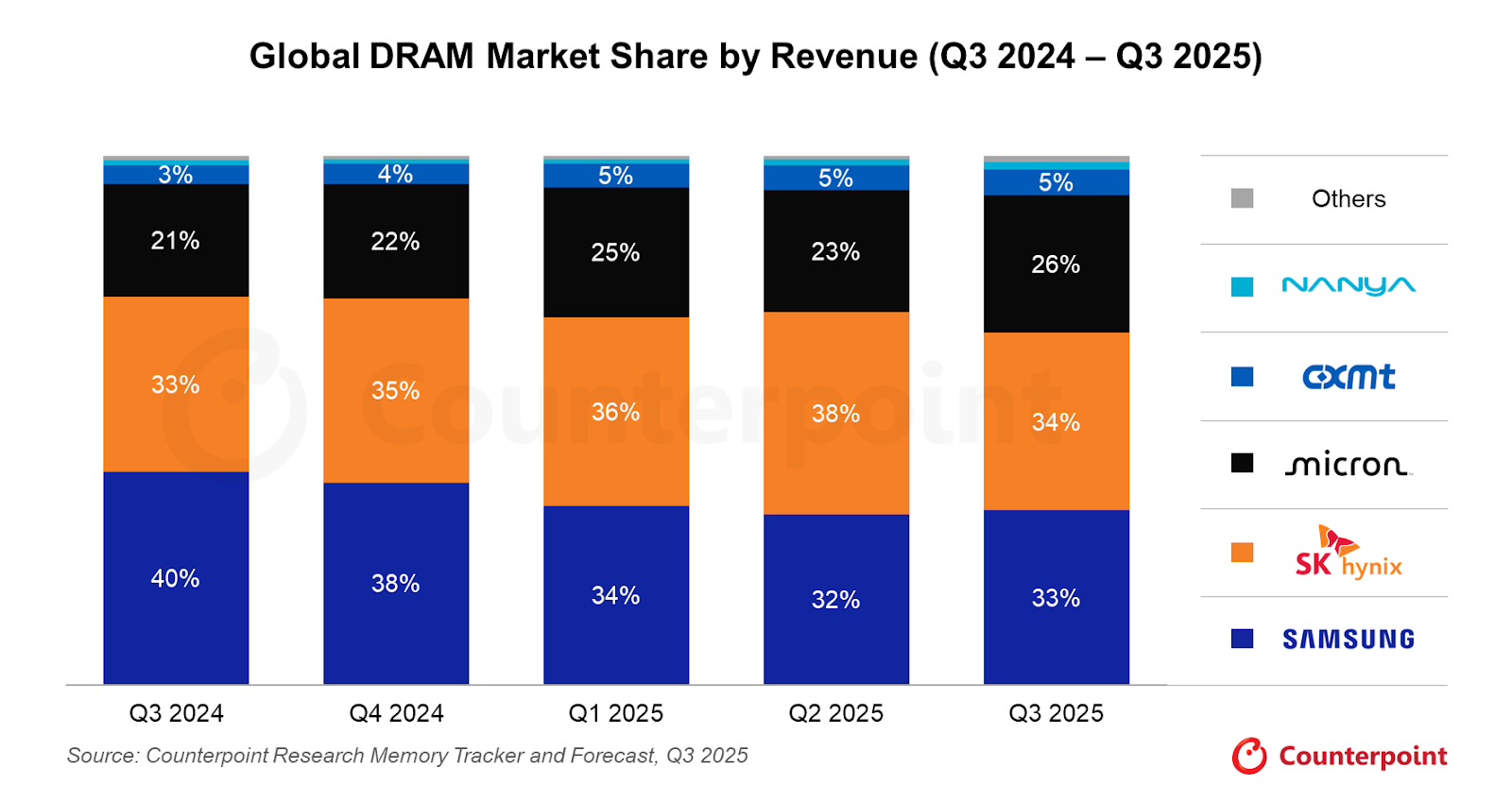

Samsung es una de las pocas empresas a nivel mundial que diseña y fabrica chips a escala. Compite en los segmentos de DRAM, NAND flash y chip lógico, y sigue siendo un proveedor principal para los gigantes tecnológicos globales.

El amplio alcance de Samsung es una fortaleza, pero también una complejidad. Su división de memoria se enfrenta a la presión de los márgenes de los ciclos de inventario, mientras que su negocio de fundición continúa rezagando a TSMC en rendimientos de vanguardia.

El auge de la memoria impulsado por la IA puede proporcionar un viento de cola, aunque la ejecución en la producción de HBM ha sido más lenta que la de su rival local SK Hynix.

Qué ver

- Progreso de la calificación de HBM: Samsung ha estado trabajando para calificar sus chips HBM3E con Nvidia. Cualquier confirmación de una importante ganancia en la oferta podría ser un catalizador significativo.

- Tendencias de precios de memoria: Los precios al contado DRAM y NAND podrían ser un indicador de la trayectoria de margen de Samsung.

- Mejoras en el rendimiento de la fundición: El negocio de fundición lógica de Samsung ha tenido problemas con los rendimientos en nodos avanzados; cualquier progreso creíble aquí podría volver a calificar la división.

- Orientación de administración: Después de un período de volatilidad de las ganancias, se observará de cerca la claridad sobre los planes de capital y los objetivos divisionales en los próximos resultados.

3. Ventajas (ATEYY)

Advantest, con sede en Tokio, fabrica equipos de prueba utilizados para verificar que los chips cumplan con los estándares de rendimiento y calidad.

Suministra a Samsung, Intel, Nvidia, Qualcomm y Texas Instruments, lo que le permite beneficiarse del crecimiento de la industria de chips en general, independientemente de qué fundición gane participación de mercado.

Las acciones de Advantest se duplicaron en 2025 (+102%), y elevó su pronóstico de ventas en 21.8% y su pronóstico de ganancias en 70.6% para el año que termina marzo de 2026.

Qué ver

- Solicitar actualizaciones del backlog: Cualquier contracción en la acumulación de Advantest podría ser una señal de alerta temprana después de la fuerte racha de 2025.

- Demanda de pruebas de chips de IA: A medida que los chips se vuelven más complejos, aumenta el tiempo de prueba por chip. Monitoree si los volúmenes del acelerador de IA de TSMC y Samsung comienzan a impulsar una demanda de pruebas desmedida.

- Orientación para el año fiscal 2026: La próxima actualización del pronóstico será fundamental para confirmar si el ciclo de upgrade de 2025 aún debe ejecutarse.

4. Tokyo Electron (T: 8035)

Tokyo Electron es uno de los mayores proveedores mundiales de equipos de producción de semiconductores, especializado en herramientas de deposición, grabado y limpieza.

Todos los principales fabricante de chips, incluidos TSMC, Samsung y SK Hynix, dependen de los sistemas de TEL para escalar la producción.

A medida que los fabricantes de chips invierten miles de millones para ampliar la capacidad, la libreta de pedidos de TEL crece. El riesgo radica en las posibles restricciones de exportación de Estados Unidos a la venta de equipos avanzados a China, que sigue siendo uno de los principales segmentos de ingresos para la compañía.

Qué ver

- Política de control de exportaciones de Estados Unidos: China representa una parte significativa de los ingresos de TEL. Cualquier endurecimiento de las normas de exportación de equipos es el riesgo más inmediato de vigilar.

- Anuncios de Capex de Chipmaker: Los planes de gastos de capital de TSMC, Samsung y SK Hynix para 2026 se traducen directamente en pedidos de equipos. Cualquier corte podría fluir a través de la libreta de pedidos de TEL.

- Nuevos ciclos de adopción de herramientas: Supervisar si las herramientas de deposición y deposición de próxima generación de TEL se están adoptando en las instalaciones de vanguardia.

5. SK Hynix (KR:000660)

SK Hynix es el segundo fabricante de chips de memoria más grande del mundo y se ha convertido en posiblemente el beneficiario más claro de la era de la IA en el espacio de la memoria.

Es el principal proveedor de chips de memoria de ancho de banda alto (HBM) de Nvidia, la memoria especializada utilizada en aceleradores de IA como el H100 y el B200.

La demanda de HBM ha impulsado una recalificación dramática del perfil de ingresos y la posición en el mercado de SK Hynix. Con el gasto en infraestructura de IA mostrando pocas señales de desaceleración de cara a 2026, la franquicia HBM de la compañía podría seguir siendo un diferenciador clave.

No obstante, las limitaciones de capacidad y el riesgo de que Samsung y Micron cierren la brecha de HBM son las principales preocupaciones a tener en cuenta.

Qué ver

- Relación de suministro de Nvidia: Cualquier cambio en la mezcla de proveedores de Nvidia hacia Samsung o Micron podría ser un evento de riesgo clave.

- Desarrollo HBM4: La carrera hacia la próxima generación de HBM ya está en marcha. Esté atento a las actualizaciones sobre la preparación HBM4 de SK Hynix y si puede mantener su liderazgo.

- Precios de memoria convencionales: SK Hynix aún obtiene ingresos significativos de DRAM y NAND estándar. Las tendencias de los precios al contado podrían ser un indicador del ciclo de memoria más amplio.

Conclusión

TSMC, SK Hynix, Samsung, Advantest y Tokyo Electron controlan colectivamente los puntos de choque de la construcción de IA.

El aumento esperado en la infraestructura de IA puede soportar la demanda, pero los inversores deben sopesar los riesgos cuidadosamente.

La exposición geopolítica, las restricciones a la exportación de Estados Unidos y el ritmo de competencia de HBM podrían mover la aguja.

¿Listo para comerciar más allá de las mayores?

Abrir una cuenta · Iniciar sesión

So, here’s the thing...

If you have been following the tech story for the last decade, you have been trained to look at a very specific, very small patch of real estate in Northern California. But as we sit here in early 2026, the "connect-the-dots" moment for investors is this: the AI trade has stopped being about shiny software demos in Palo Alto and has started being about the physical industrialisation of compute.

Want to know more? Read our 2026 AI playbook

What changed, and why it matters

We have entered the "Year of Proof". The world’s largest companies, the hyperscalers, are projected to spend a staggering US$650 billion on capital expenditures this year. But here’s the part most people miss: that money is not staying in Silicon Valley. It’s flowing to the "picks and shovels" players in Idaho, Washington, Colorado and even overseas.

If you want to understand where the actual return on investment (ROI) may be landing this earnings season, you have to look outside the 650 area code. The shift from AI hype to AI industrialisation is changing the map.

Five companies · AI infrastructure play · 2026

The full AI stack: from capex to consulting

Infrastructure builders compared to the implementation bridge across the AI value chain

Hyperscaler CapEx: Early 2026 analyst estimates, midpoint of ranges. Amazon approx. 100% YoY, Alphabet approx. 100%, Meta approx. 87%, Microsoft approx. 50%.

Accenture: Cumulative advanced AI bookings $11.5B through Q1 FY2026. Q1 AI bookings $2.2B (up 76% YoY), AI revenue $1.1B (up 120% YoY) across 1,300+ clients.

Five companies shaping the next phase of AI

Micron Technology (MU), Boise, Idaho

Micron is the "memory backbone" of the current cycle. While everyone was watching the chip designers, many overlooked the fact that AI chips are far less useful without high-bandwidth memory (HBM). Micron is currently viewed by some analysts as a strong buy because its capacity is reportedly sold out through the end of 2026. Analysts are also eyeing a 457% jump in earnings per share (EPS) as the memory cycle reaches what some describe as a robust peak.

Microsoft (MSFT), Redmond, Washington

Microsoft is the enterprise backbone of this transition. It has moved beyond simple chatbots and is now building what analysts call "Intelligence Factories". While the stock has faced pressure recently over capacity constraints, underlying demand for Azure AI is reportedly still running ahead of capacity. The broader bull case is that Microsoft is moving into "Agentic AI", systems that do not just talk to users but may also execute multi-step business workflows.

Which Asian companies are betting big on artificial intelligence?

Amazon (AMZN), Seattle, Washington

Amazon is playing a long-term game of vertical integration. To reduce its reliance on expensive third-party hardware, it’s building its own AI chips in-house. Amazon Web Services (AWS) remains the primary driver of profitability, and the company is using its retail data to train specialised models that many Silicon Valley start-ups may struggle to replicate.

Palantir Technologies (PLTR), Denver, Colorado

If Micron provides the memory and Microsoft the platform, Palantir provides the "operating system" for the modern AI factory. The company has posted strong momentum, with US commercial sales recently growing 93% year over year. It’s often framed as a bridge between raw data and corporate profitability, which remains a key focus for investors in 2026.

Accenture (ACN), Dublin, Ireland

You cannot just "plug in" AI. Businesses often need to redesign processes around it, and that’s where Accenture comes in.

The company is viewed as an implementation bridge, with one analyst arguing that "GenAI needs Accenture" to move from pilot programs to production though the cautionary angle is that the AI story has not fully excited investors here yet because consulting revenue can take longer to show up than chip sales.

What could happen next?

The chart maps the three time horizons likely to shape the next phase of the AI industrialisation trade.

In the near term, markets are still reacting to chipmaker earnings, guidance, and any signs of capacity strain. Over the next month, attention shifts to the real-world inputs behind AI growth, especially power, financing, and infrastructure. By the 60-day window, the key question is whether AI spending is broadening into a wider market re-rating or running ahead of near-term returns.

Across all three periods, the focus is the same: proof. Investors are looking for signs that AI capital expenditure is translating into real demand for energy, land, and industrial capacity. That is why updates from companies tied to power and data centre buildout matter more than ever.

Scenario planning · March 2026

What could happen next

Three time horizons, three scenarios to watch across the AI industrialisation cycle

Chipmaker reports

Possible

Market volatility continues as traders digest the latest reports from chipmakers like Micron

Upside scenario

"Bulletproof" guidance from remaining infrastructure names triggers a sector-wide relief rally

Watch for

Any mention of "capacity constraints" or "supply bottlenecks" in earnings calls

Energy and rates

Possible

Focus shifts to "real economy" energy players like NextEra that power the data centres

Downside scenario

Rising oil prices from Middle East conflict act as a tax on tech margins, rotating into defensives

Action point

Monitor Fed language on rates. Higher for longer makes $650B capex bills far more expensive to finance

The great dispersion

Possible

Market rewards companies with real AI revenue and punishes those still stuck in experimentation

Upside scenario

NextEra Energy (NEE) data centre announcements in late April/May trigger a utility renaissance rally

Downside scenario

An "air pocket" in profits occurs where debt-funded investment outpaces revenue gains

Watch

May reports from Texas Pacific Land (TPL) — is data centre land demand still "red hot"?

Action point

Review your portfolio for geographic diversity. The AI story is now a global power race

The psychological trap

The emotional trap many traders fall into right now is recency bias. You have seen NVIDIA and the "Magnificent 7" win for so long that it feels like they are the only way to play this. But the "obvious" trade is often the one that has already been priced in. Before acting, ask yourself: "Am I buying this stock because I understand its role in the physical AI supply chain, or because I’m afraid of missing the next leg of a rally that started two years ago?"

Ready to trade beyond the majors?

Open an account · Log in

Disclaimer: This content is general information only and should not be relied on as personal financial advice or a recommendation to buy, sell, or hold any financial product. References to companies or themes, including AI-related stocks, are illustrative only. Share and derivative markets can move sharply, and concentrated sectors such as AI and technology may experience elevated volatility, valuation risk, and liquidity risk. If you trade derivatives such as CFDs, leverage can magnify both gains and losses. Past performance is not a reliable indicator of future performance.