New U.S. Sanctions on Russia as Putin Conducts Nuclear Tests

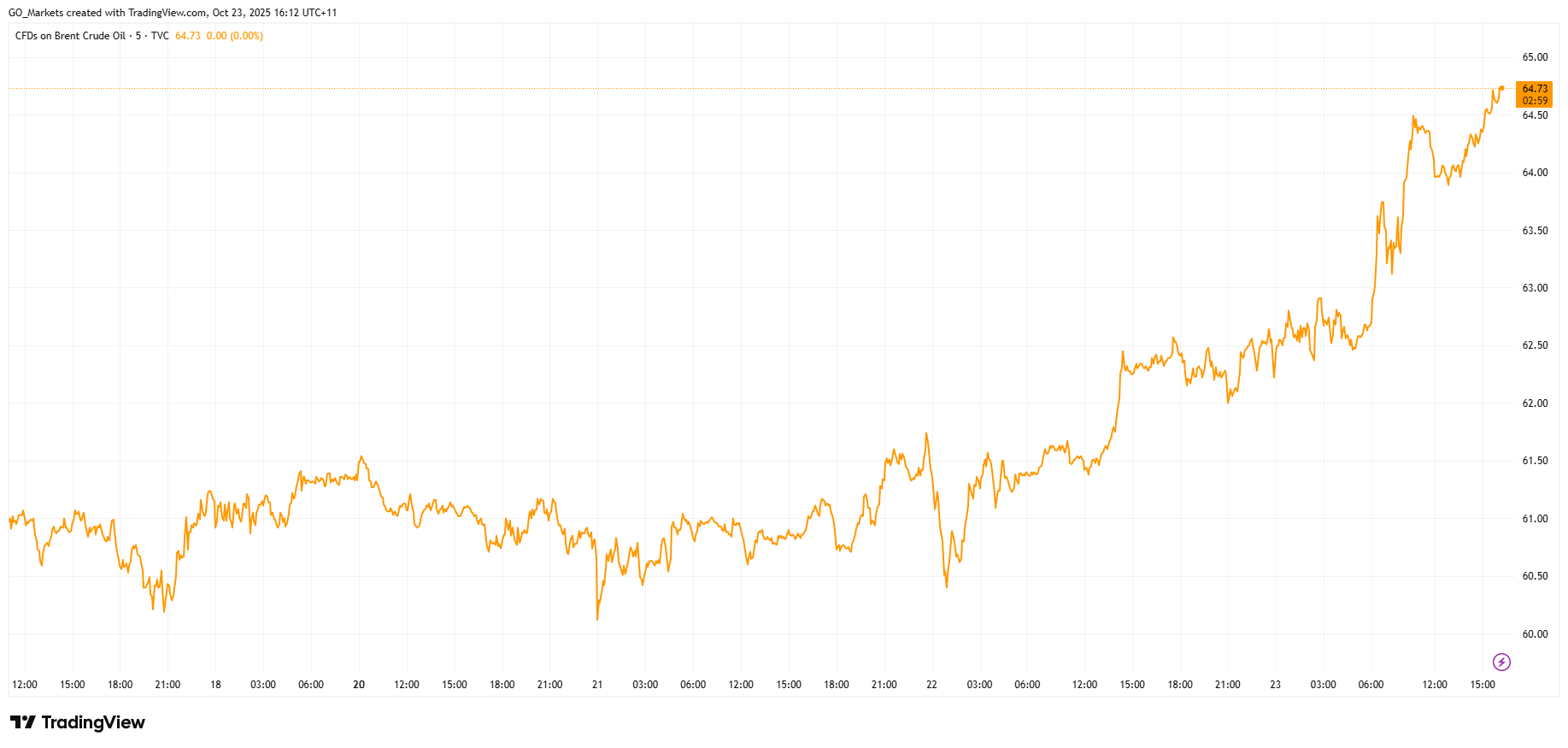

The U.S. has imposed new sanctions on Russia's two largest oil companies, Rosneft and Lukoil, after planned peace talks between Trump and Putin collapsed on Wednesday.

Oil prices spiked 3% after the announcement, with Brent crude hitting $64 per barrel.

The targeted companies are among the world's largest energy exporters, collectively shipping about three million barrels of oil daily and accounting for nearly half of Russian production.

The sanctions build on recent European measures, as the UK targeted the same companies last week and the EU approved its own sanctions package on Wednesday.

In a show of force coinciding with the new sanctions, Putin supervised strategic nuclear exercises on Wednesday involving intercontinental ballistic missile launches from land and submarine platforms.

While the Kremlin emphasised these were routine drills, the highly coincidental timing is notable.

For markets, the key question now is whether secondary sanctions will follow, and if Trump’s enforcement remains strict. Traders will watch closely for any TACO signals that see Trump ease pressure in an attempt to restart negotiations.

Historic PM Wasting No Time on Celebrations

Sanae Takaichi made history this week as Japan's first female Prime Minister. The 64-year-old conservative leader, dubbed the "Iron Lady,” is already rolling out an aggressive policy agenda that could reshape Japan's economic and geopolitical position.

Her first major move is an economic stimulus package expected to exceed US $92 billion. The package includes abolishing the provisional gasoline tax and raising the tax-free income threshold from ¥1.03 million ($6,800), moves designed to put more money in consumers' pockets and battle inflation.

Her next move will come when Trump arrives in Tokyo next week, as the Japanese government is finalising a purchase package including Ford F-150 pickup trucks, US soybeans, and liquefied natural gas as sweeteners for trade talks.

Takaichi has campaigned on being a champion for expansionary fiscal policy, monetary easing, and heavy government investment in strategic sectors, including AI, semiconductors, biotechnology, and defence.

Critical Workers to Miss First Paycheck Due to Shutdown

The U.S. government shutdown is on the verge of creating a crisis for aviation safety, with 60,000 workers set to miss their first full paycheck this week.

These essential workers, who earn an average of $40,000 annually, already saw shortened paychecks last week. By Thursday, many will receive pay stubs showing zero compensation for the coming period, forcing impossible choices between basic necessities and reporting to work.

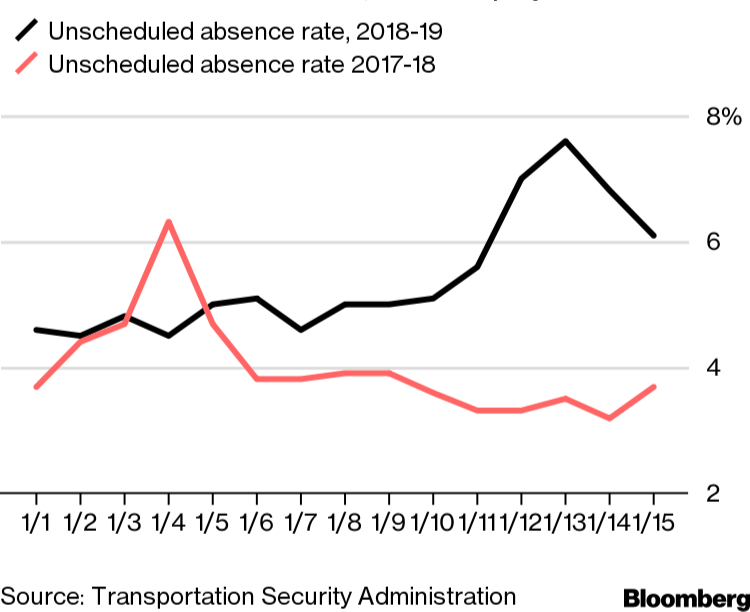

During the last extended shutdown, TSA sick-call rates tripled by Day 31, causing major delays at checkpoints and reduced air traffic in major hubs like New York — disruptions which are directly attributed to pressuring the end of the previous shutdown.

The National Air Traffic Controllers Association warns that similar pressures are building, with many workers soon to be facing a decision between attending their shift or putting food on the table.

The information provided is of general nature only and does not take into account your personal objectives, financial situations or needs. Before acting on any information provided, you should consider whether the information is suitable for you and your personal circumstances and if necessary, seek appropriate professional advice. All opinions, conclusions, forecasts or recommendations are reasonably held at the time of compilation but are subject to change without notice. Past performance is not an indication of future performance. Go Markets Pty Ltd, ABN 85 081 864 039, AFSL 254963 is a CFD issuer, and trading carries significant risks and is not suitable for everyone. You do not own or have any interest in the rights to the underlying assets. You should consider the appropriateness by reviewing our TMD, FSG, PDS and other CFD legal documents to ensure you understand the risks before you invest in CFDs. These documents are available here.

免责声明:文章来自 GO Markets 分析师和参与者,基于他们的独立分析或个人经验。表达的观点、意见或交易风格仅代表作者个人,不代表 GO Markets 立场。建议,(如有),具有“普遍”性,并非基于您的个人目标、财务状况或需求。在根据建议采取行动之前,请考虑该建议(如有)对您的目标、财务状况和需求的适用程度。如果建议与购买特定金融产品有关,您应该在做出任何决定之前了解并考虑该产品的产品披露声明 (PDS) 和金融服务指南 (FSG)。

.jpg)