Venezuela commands the world's largest proven oil reserves at 303 billion barrels. Yet political turmoil, global sanctions, and recent US intervention show that being the biggest isn’t always best.

Quick facts:

- Venezuela holds 18% of the world's total proven oil reserves despite producing less than 1% of global consumption.

- Just four countries (Venezuela, Saudi Arabia, Iran, and Canada) control over half the planet's proven reserves.

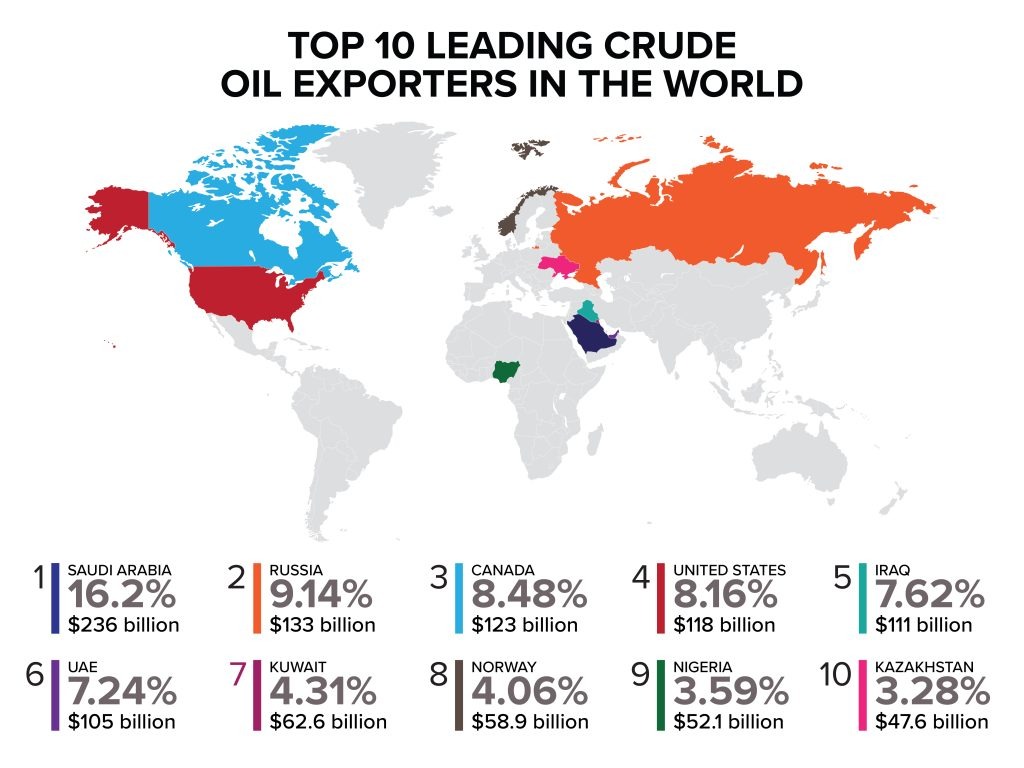

- Saudi Arabia dominates crude oil production contributing to over 16% of global exports.

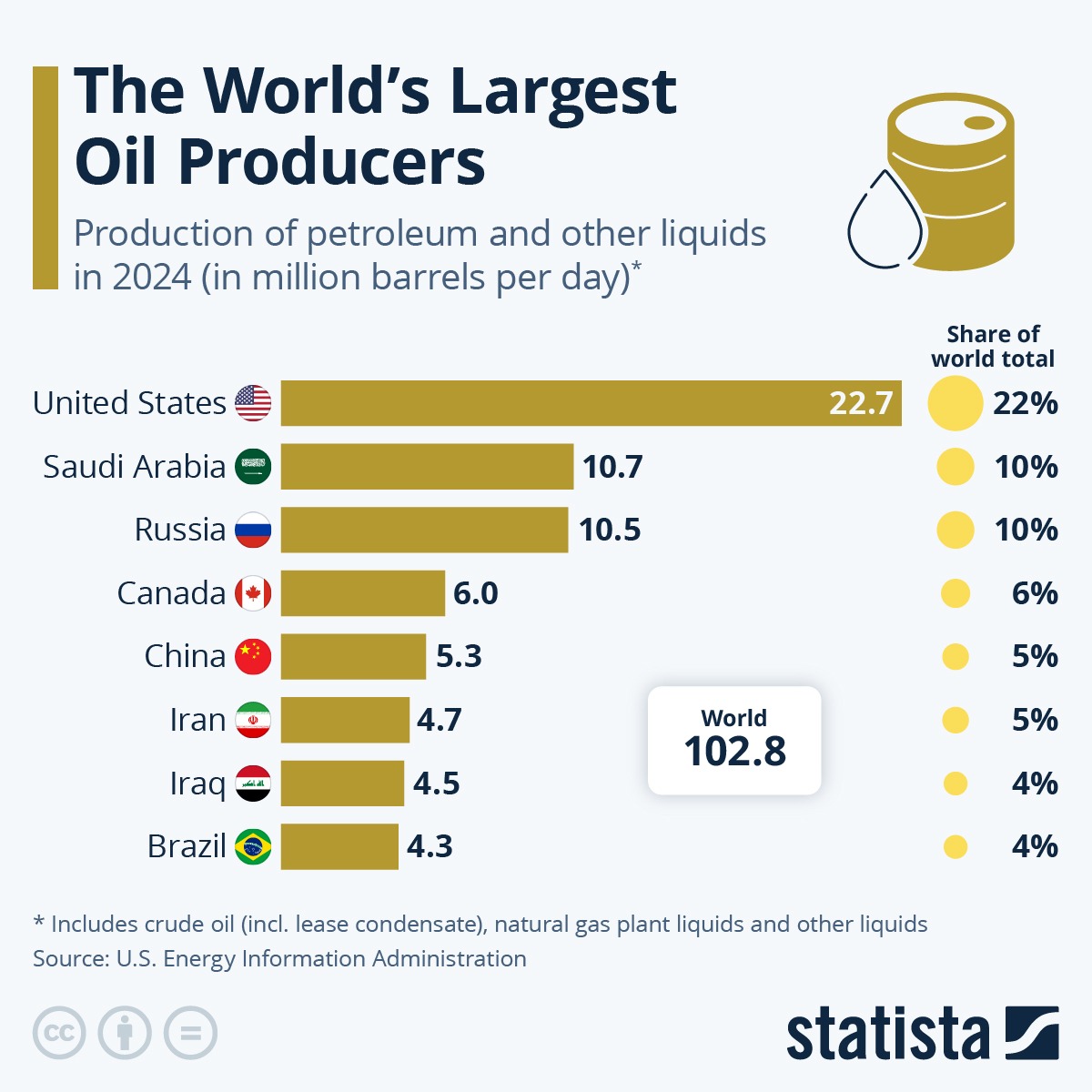

- US shale technology has enabled America to lead in production despite ranking ninth in reserves.

Top 10 countries by proven oil reserves

1. Venezuela – 303 billion barrels

- Controls 18% of global reserves, primarily extra-heavy crude in the Orinoco Belt requiring specialised refining.

- Heavy crude trades $15-20 below Brent benchmarks due to high sulphur content and complex processing requirements.

- Output crashed 60% from 2.5 million bpd in 2014 to less than 1.0 million bpd last year.

- Approximately 80% of exports flow to China as loan repayment, with export revenues dwarfed by reserve potential.

2. Saudi Arabia – 267 billion barrels

- Majority light, sweet crude oil requires minimal refining and commands premium prices, contributing to world-leading exports of $191.1 billion in 2024.

- Maintains 2-3 million bpd of spare production capacity, providing market stabilisation capability during supply disruptions.

- Oil comprises roughly 50% of the country’s GDP and 70% of its export earnings.

- Production decisions significantly impact international oil prices due to market dominance.

3. Iran – 209 billion barrels

- Heavy Western sanctions severely limit the country’s ability to monetise and access international markets.

- Production estimates vary significantly (2.5-3.8 million bpd) due to sanctions, limited transparency, and restricted international reporting.

- Significant crude volumes flow to China through discount arrangements and sanctions-evading mechanisms.

- Sanctions relief could rapidly boost production toward 4-5 million bpd, though domestic consumption (12th globally) reduces export potential.

4. Canada – 163 billion barrels

- Approximately 97% of reserves are oil sands (bitumen) requiring steam-assisted extraction and significant upfront capital investment.

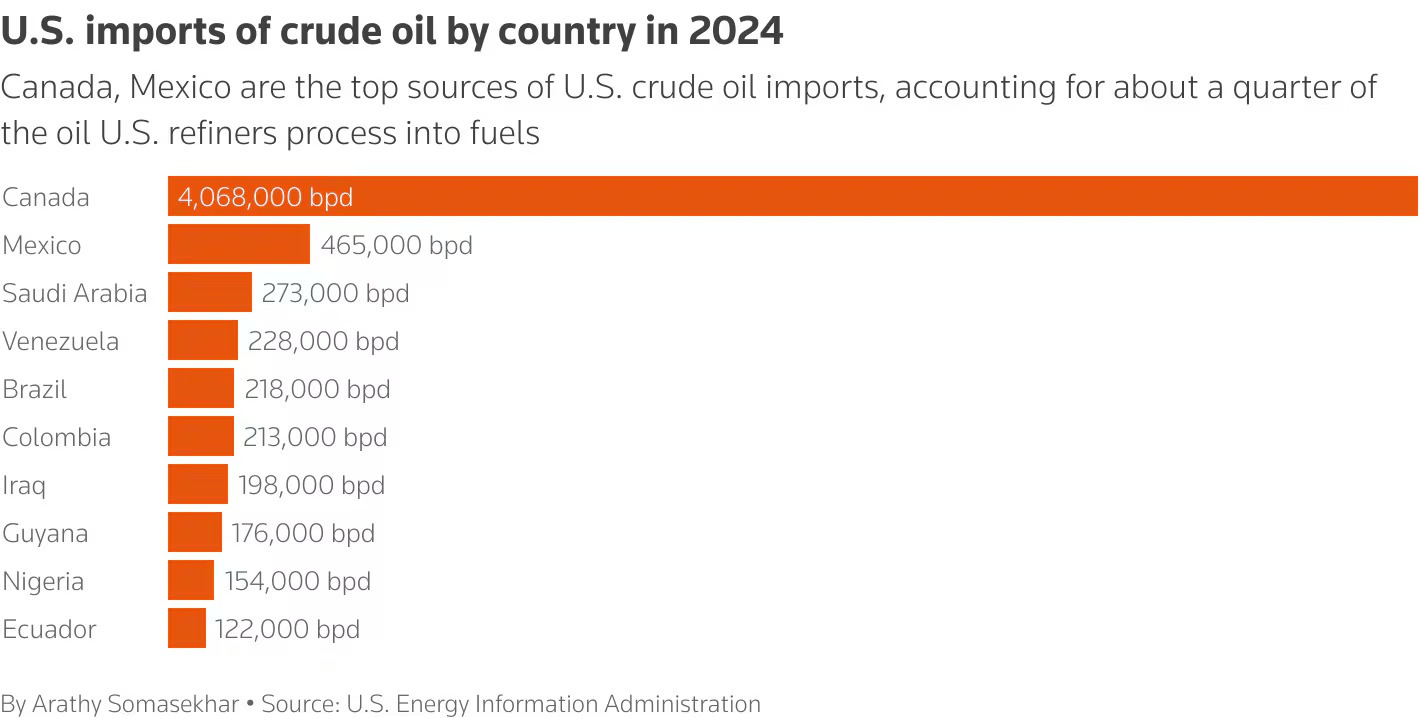

- Political stability and regulatory frameworks position Canada as a secure source compared to volatile producers, with direct pipeline access to US refineries.

- Supplied over 60% of U.S. crude oil imports in 2024, making Canada America's top source by far.

5. Iraq – 145 billion barrels

- Decades of war and sanctions have prevented optimal field development and infrastructure modernisation.

- Improved security conditions since 2017 have enabled production recovery, but pipeline attacks and aging facilities continue to constrain output.

- Oil revenue comprises over 90% of government income, creating extreme fiscal vulnerability.

- Exports flow primarily to China, India, and Asian buyers seeking a reliable Middle Eastern supply, with most production from super-giant southern fields near Basra.

6. United Arab Emirates – 113 billion barrels

- Produces primarily medium-to-light sweet crude commanding premium prices, ranking fourth globally in export value at $87.6 billion.

- Has successfully diversified its economy through tourism, finance, and trade, reducing oil's GDP share compared to Gulf peers.

- Strategic location near the Strait of Hormuz and openness to international oil companies help facilitate efficient global distribution.

7. Kuwait – 101.5 billion barrels

- Reserves are concentrated in aging super-giant fields like Burgan, which require enhanced recovery techniques.

- Favourable geology enables extraction costs around $8-10 per barrel, with proven reserves providing 80+ years of supply at current production rates.

- Oil comprises 60% of GDP and over 95% of export revenue.

8. Russia – 80 billion barrels

- World's third-largest producer despite ranking eighth in reserves.

- Post-2022 Western sanctions redirected crude flows from Europe to Asia, with China and India now absorbing the majority at discounted prices.

- Despite export restrictions and G7 price cap at $60/barrel, it posted the second-highest global export value at $169.7 billion in 2024.

- Russian Urals crude typically trades $15-30 below Brent due to quality, sanctions, and logistics, with November 2024 revenues declining to $11 billion.

9. United States – 74.4 billion barrels

- The shale revolution through horizontal drilling and hydraulic fracturing has made the U.S. the world's #1 oil producer despite holding only the 9th-largest reserves.

- The Permian Basin accounts for nearly 50% of production, with shale/tight oil representing 65% of total output.

- Achieved net petroleum exporter status in 2020 for the first time since 1949, with crude exports growing from near-zero in 2015 to over 4 million bpd in 2024.

- The U.S. government maintains a 375+ million barrel strategic reserve.

10. Libya – 48.4 billion barrels

- Holds Africa's largest proven oil reserves at 48.4 billion barrels, producing light sweet crude commanding premium prices.

- Rival bordering governments compete for oil revenue control, causing production to fluctuate based on political conditions.

- Oil facilities face blockades, militia attacks, and political leverage tactics, preventing consistent returns.

- Favourable geology enables extraction costs around $10-15 per barrel, with geographic proximity making Libya a natural supplier to European refineries.

What does this mean for oil markets?

The concentration of reserves among OPEC members (60% of the global total) ensures the organisation has continued influence over pricing, even as US shale provides a production counterweight.

Venezuela's potential return as a major exporter post-U.S. occupation could eventually ease supply constraints, though most analysts view significant production increases as years away.

Sanctions could create a situation where discounted crude seeks buyers willing to navigate compliance risks. Refiners with heavy crude processing capability may benefit from price differentials if Venezuelan barrels increase.

While reserves appear abundant, economically recoverable volumes depend on sustained high prices. If renewable adoption accelerates and demand peaks sooner than projected, stranded assets become a material risk for reserve-heavy producers.

Disclaimer: Articles are from GO Markets analysts and contributors and are based on their independent analysis or personal experiences. Views, opinions or trading styles expressed are their own, and should not be taken as either representative of or shared by GO Markets. Advice, if any, is of a ‘general’ nature and not based on your personal objectives, financial situation or needs. Consider how appropriate the advice, if any, is to your objectives, financial situation and needs, before acting on the advice. If the advice relates to acquiring a particular financial product, you should obtain our Disclosure Statement (DS) and other legal documents available on our website for that product before making any decisions.

.jpeg)