Oil smashed US$100 a barrel as US-Israeli strikes on Iran shut down the Strait of Hormuz, triggering the biggest single-day crude spike since the Russian invasion of Ukraine.

Quick facts

- Brent Crude intraday peak: US$119.50/bbl (up ~50% in 10 days)

- Reported vessel traffic through the Strait of Hormuz fell to <20% of average

- Analysts estimate up to ~20% of global seaborne oil flows could be affected if disruption persists (largest since the 1956 Suez Crisis)

Why have oil prices spiked?

Oil markets woke up on 9 March 2026 to joint U.S.-Israeli strikes on Iranian oil depots that sent Brent crude to an intraday peak of US$119.50 a barrel (its highest level since the start of the Russia-Ukraine war) before settling back near US$90.

Iran's Revolutionary Guard has threatened to target any tanker transiting the Strait of Hormuz, collapsing vessel traffic to near-zero.

The strait carries roughly 20% of the world's daily seaborne oil supply, and analysts are describing the disruption as the largest since the Suez Crisis of 1956–57. Crude had already risen around 16% in the week before the strikes as markets priced in escalating tensions.

Middle East escalation: oil, VIX and volatility scenarios

ExxonMobil's chief economist, Tyler Goodspeed, has said the distribution of probable outcomes skews heavily toward the Strait remaining effectively closed for longer than markets currently expect.

Meanwhile, Donald Trump has played down the need to release strategic petroleum reserves, calling any short-term price pain a small cost for global safety. The G7 is discussing a coordinated SPR release, which briefly pulled prices back toward US$110 before late-session trading moved them lower on fresh Trump commentary about a potentially “swift end” to the conflict.

Biggest single day crude oil spike since 2022 | TradingView

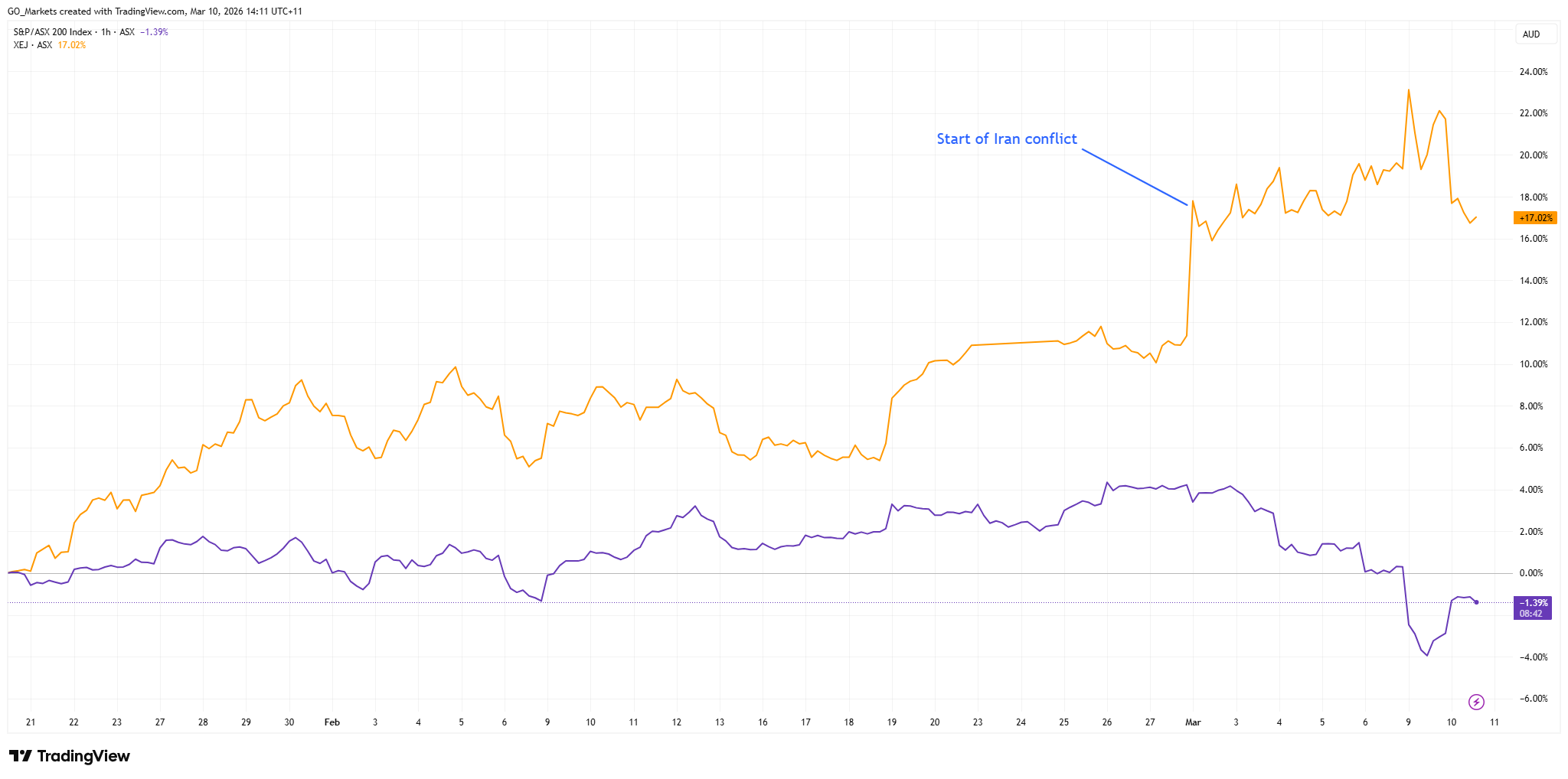

Market Reaction

The ASX response has been sharply split. The broader ASX 200 fell as investors priced in inflation and potential demand destruction, with materials stocks like BHP sinking close to 6%. Energy was the only sector in the green. The IMF estimates that every sustained 10% rise in oil prices adds 0.4% to global inflation and reduces global growth by 0.15%.

If oil holds above US$100 for an extended period, recession risk in major importing economies could rise materially. ASX energy investors are navigating a world where the same tailwind for producers could become a headwind for global demand.

S&P/ASX 200 vs S&P/ASX 200 Energy Index | TradingView

Top 5 ASX energy stocks to watch

1. Woodside Energy Group (ASX: WDS)

Woodside is Australia’s largest listed oil and gas producer and is often closely watched when energy prices rise. Woodside operates Pluto LNG in the Pilbara with a 90% stake, the North West Shelf LNG project, and a growing international portfolio. Shares hit a fresh 52-week high and have risen 33% since January.

Fully franked dividends add yield support; the company recently paid an 83.4-cent-per-share final dividend. For cautious investors, Woodside is a potential entry point in the sector right now.

2. Santos Ltd (ASX: STO)

Santos is the ASX's second-largest oil and gas producer with a market cap of nearly A$23 billion, and it offers a compelling production growth story on top of the price tailwind.

The Barossa gas project shipped its first LNG cargo in January 2026, and production is expected to grow around 30% by 2027 as Barossa and the Pikka project in Alaska ramp up together.

CEO Kevin Gallagher sold A$5.6 million in stock in late February to cover personal tax obligations, which some investors have flagged as a caution signal, but the growth fundamentals remain intact.

3. Karoon Energy (ASX: KAR)

A mid-cap pure-play oil producer with 100% interests in the Bauna and Patola offshore oil fields in Brazil's Santos Basin, plus the Who Dat assets in the Gulf of Mexico, it was the biggest mover on the entire ASX 200 in recent sessions.

With a market cap near A$1.25 billion and a Price to Earnings (P/E) ratio of 7, the stock is extraordinarily sensitive to oil price movements. Karoon generated a free cash flow margin of approximately 45% against a base case of US$65 per barrel. At current prices, the cash flow profile could improve dramatically.

A new dividend of A$0.031 per share has been declared alongside 2026 production guidance. The risk is symmetrical: if the war premium fades and oil drifts back toward the mid-US$60s, the pullback could be as sharp as the rally.

4. Ampol Ltd (ASX: ALD)

Ampol is Australia's largest integrated fuel company, operating the Lytton oil refinery in Brisbane alongside a national fuel retail and distribution network and Z Energy in New Zealand.

Higher oil prices are a double-edged sword for Ampol. They improve crude inventory value and refining margins, but can compress consumer demand over time.

A planned A$1.1 billion acquisition of EG Australia's fuel and convenience network adds a structural growth catalyst independent of the oil price. A 100%-franked trailing yield of 3.2% could also provide income support.

5. Beach Energy (ASX: BPT)

Beach Energy has underperformed the broader ASX energy sector over the past year, weighed down by reserve replacement challenges and a difficult recent earnings period.

However, the company beat half-year FY2026 estimates by 13.5%, and management maintained full-year production guidance of 19.7–22.0 million barrels of oil equivalent.

Beach's asset base spans the Cooper and Eromanga Basins, the Otway Basin, the Perth Basin's Waitsia LNG export project, and New Zealand.

A 6.1% dividend yield with a payment due in March 2026, and the stock's low beta of 0.20 means it could offer materially less volatility than peers.

CEO Brett Woods has flagged M&A interest in East Coast gas assets and a target of 35% emissions intensity reduction by 2030. A sustained high-oil environment could arrest Beach's production decline trend.

What to watch next

Energy markets are moving on fear and geopolitics rather than fundamentals, which means the trade can reverse as fast as it started. The key question is whether this is a brief war premium or the start of a sustained structural disruption.

A prolonged Hormuz closure could push Brent even higher and keep ASX energy stocks elevated. A swift diplomatic resolution or coordinated G7 SPR release could snap oil back downwards and reverse much of the recent move.

Sitting over both scenarios is the question of recession: if oil holds above US$100 for six to eight weeks, markets may begin pricing in central bank responses and demand destruction, which could ultimately weigh on the Energy sector that is outperforming today.

The information provided is of general nature only and does not take into account your personal objectives, financial situations or needs. Before acting on any information provided, you should consider whether the information is suitable for you and your personal circumstances and if necessary, seek appropriate professional advice. All opinions, conclusions, forecasts or recommendations are reasonably held at the time of compilation but are subject to change without notice. Past performance is not an indication of future performance. Go Markets Pty Ltd, ABN 85 081 864 039, AFSL 254963 is a CFD issuer, and trading carries significant risks and is not suitable for everyone. You do not own or have any interest in the rights to the underlying assets. You should consider the appropriateness by reviewing our TMD, FSG, PDS and other CFD legal documents to ensure you understand the risks before you invest in CFDs. These documents are available here.

Any references to Australian or international shares, sectors, indices, ETFs, crypto-related stocks or other instruments are provided for market commentary and watchlist purposes only and do not constitute a recommendation, offer or solicitation to buy, sell or hold any financial product or adopt any investment strategy. International markets may involve additional risks, including currency fluctuations, regulatory differences, market structure differences, reduced liquidity and higher volatility. Company-specific, sector-specific and macroeconomic risks may also affect performance.

Commentary on geopolitical developments, economic data, central bank decisions, earnings, policy changes and other global or financial market events is based on information available at the time of publication and may change without notice. Such events can lead to sudden market moves, price gaps, reduced liquidity, wider spreads and increased volatility, particularly in leveraged products such as CFDs. Forward-looking statements, expectations and scenario analysis are inherently uncertain and should not be relied on as guarantees of future market behaviour or outcomes.