มีนาคมเปิดด้วยข้อมูลกิจกรรมและอัตราเงินเฟ้อของจีนในช่วงต้นเดือน ตามด้วยรายงานข้อมูลที่เกี่ยวข้องกับตลาดไหลเข้ามาจากประเทศญี่ปุ่น ในขณะที่ธนาคารกลางออสเตรเลีย (RBA) พบกันกลางเดือน โดยตลาดปัจจุบันกำหนดราคาอัตรากรมธรรม์หยุดชั่วคราว

ประเทศจีน

แนวโน้มของจีนมีนาคมเต็มไปด้วยกิจกรรมเงินเฟ้อและการเผยแพร่ทางการค้าที่สามารถกำหนดโทนความเสี่ยงระดับภูมิภาคได้อย่างรวดเร็วปฏิกิริยาของตลาดอาจขึ้นอยู่กับการตีความนโยบายและเงื่อนไขสภาพคล่องเช่นเดียวกับข้อมูลที่ทำให้เกิดความประหลาดใจของตนเอง

วันที่สำคัญ

- PMI การผลิตและไม่ใช่การผลิตของจีน: 12:30 น., 2 มีนาคม (AEDT)

- ไชน่าเคซิน PMI: 5 มีนาคม (AEDT)

- CPI ของจีน: 9 มีนาคม 12:30 น. (AEDT)

- จีน PPI: 9 มีนาคม 12:30 น. (AEDT)

- ดุลการค้าของจีน: 10 มีนาคม (AEDT)

ความเกี่ยวข้องของตลาด

โปรไฟล์ในเดือนมีนาคมของจีนมีการโหลดหน้าและขับเคลื่อนด้วยข้อมูล โดยที่ 10 วันแรกน่าจะเน้นความเชื่อมั่นในระดับภูมิภาคที่กว้างขึ้น

ข้อมูล PMI สามารถให้สัญญาณเบื้องต้นเกี่ยวกับโมเมนตัมอุตสาหกรรมและบริการในขณะที่ CPI สามารถอ่านความต้องการในประเทศและความกดดันด้านราคาได้

เนื่องจากเซี่ยงไฮ้คอมโพสิตยังคงซื้อขายใกล้ระดับที่เห็นในช่วงกลางปี 2010 ปฏิกิริยาของตลาดอาจขึ้นอยู่กับการตีความนโยบายและเงื่อนไขสภาพคล่องเช่นเดียวกับความประหลาดใจในหัวข้อ

ประเทศญี่ปุ่น

เดือนของญี่ปุ่นมุ่งเน้นไปที่การยืนยันการเติบโตตามด้วยสัญญาณนโยบายที่อาจปรับระดับโมเมนตัมของเงินเยนอีกครั้ง

วันที่สำคัญ

- PMI ของญี่ปุ่น: 2มีนาคม 11:30 น. (AEDT)

- GDP ไตรมาสที่ 4 เบื้องต้นของญี่ปุ่น: 10:50 น., 10 มีนาคม (AEDT)

- การตัดสินใจนโยบาย BOJ: 19 มีนาคม (AEDT)

ความเกี่ยวข้องของตลาด

ขณะนี้ Nikkei 225 อยู่ใกล้ระดับสูงสุดตลอดกาล ซึ่งอาจเพิ่มความอ่อนไหวต่อโทนของนโยบาย

GDP สามารถช่วยตรวจสอบความยั่งยืนของการเติบโตและแนวโน้มอุปสงค์ภายในประเทศ ในขณะที่แนวทาง BOJ สามารถกำหนดเส้นโค้งผลตอบแทนและความคาดหวังของอัตราได้

ออสเตรเลีย

ปฏิทินเดือนมีนาคมของออสเตรเลียมุ่งเน้นไปที่สัญญาณการเติบโต นโยบาย และอัตราเงินเฟ้อที่อาจกำหนดความคาดหวังสำหรับแนวโน้มในประเทศและ AUDหากนโยบายคงที่ การมุ่งเน้นมีแนวโน้มที่จะเปลี่ยนไปสู่การเติบโตที่คงทนและอัตราเงินเฟ้อยังคงอยู่แค่ไหน

วันที่สำคัญ

- GDP ของออสเตรเลีย (บัญชีแห่งชาติ): 4 มีนาคม 11:30 น. (AEDT)

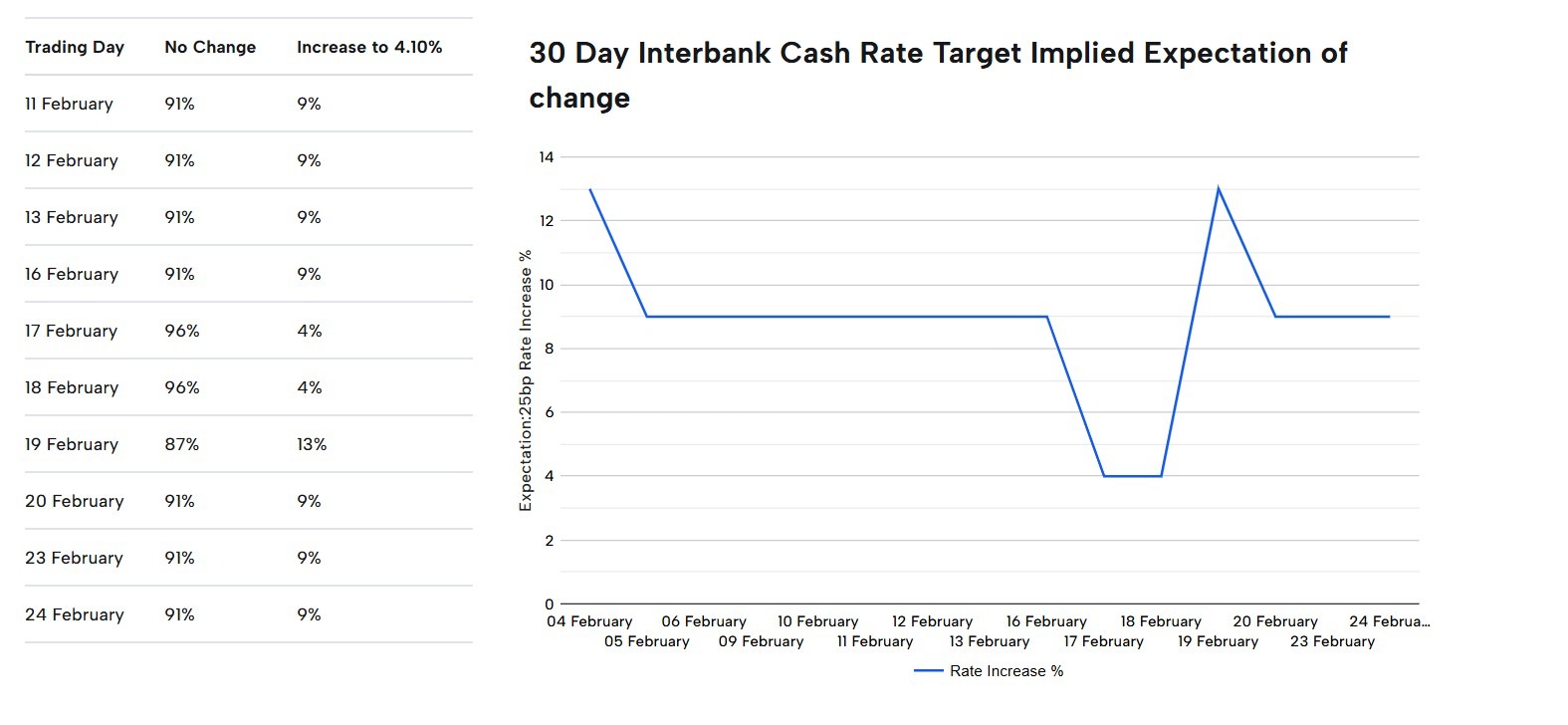

- การตัดสินใจนโยบายการเงิน RBA: 17 มีนาคม 14:30 น. (AEDT)

- แรงงานออสเตรเลีย: วันที่ 19 มีนาคม 11:30 น. (AEDT)

- CPI ของออสเตรเลีย: 25มีนาคม 23:30 น. (AEDT)

ความเกี่ยวข้องของตลาด

ในขณะที่การตัดสินใจของ RBA กำหนดความคาดหวังของเส้นทางอัตราและแนวทางด้านข้างหน้า ข้อมูลแรงงานจะแจ้งแนวโน้มค่าจ้างและการบริโภค และ CPI ยืนยันหรือท้าทายวิถีเงินเฟ้อ

ASX 200 กำลังซื้อขายใกล้ระดับสูงสุดเป็นประวัติการณ์ และ AUD ได้แสดงให้เห็นถึงความแข็งแกร่งสัมพัทธ์หลายปีเมื่อเทียบกับการข้ามที่สำคัญหลายปีหาก RBA หยุดชั่วคราว โฟกัสอาจเปลี่ยนจากทิศทางอัตราดอกเบี้ยไปสู่ความทนทานต่อการเติบโตและความคงอยู่ของอัตราเงินเฟ้อ

Reportingdates and release times are based on company investor relations calendars whereconfirmed. Where dates or times are not marked confirmed, they are GO Marketsestimates. Consensus EPS, revenue and analyst-range data are sourced fromBloomberg and Earnings Whispers, as at 09 July 2026 (AEST). Company guidance,backlog and operating metrics are sourced from the latest company filings orresults presentations, unless stated otherwise. Any scenario analysis reflectsGO Markets analysis. Figures and schedules may change without notice.

The information provided is of general nature only and does not take into account your personal objectives, financial situations or needs. Before acting on any information provided, you should consider whether the information is suitable for you and your personal circumstances and if necessary, seek appropriate professional advice. All opinions, conclusions, forecasts or recommendations are reasonably held at the time of compilation but are subject to change without notice. Past performance is not an indication of future performance. Go Markets Pty Ltd, ABN 85 081 864 039, AFSL 254963 is a CFD issuer, and trading carries significant risks and is not suitable for everyone. You do not own or have any interest in the rights to the underlying assets. You should consider the appropriateness by reviewing our TMD, FSG, PDS and other CFD legal documents to ensure you understand the risks before you invest in CFDs.

.jpeg)