ตั้งแต่โครงสร้างพื้นฐาน AI ไปจนถึงการดูแลสัตว์เลี้ยง เซมิคอนดักเตอร์ และการสำรวจทองคำ ต่อไปนี้คือผู้สมัครชั้นนำห้าคนที่มีแนวโน้มที่จะอยู่ในรายชื่อมากที่สุด แอ็กซ์ ในปี พ.

การเสนอขายสาธารณะเบื้องต้น (IPO) คืออะไร?

1.เฟอร์มุส เทคโนโลยี

Firmus Technologies กำลังสร้างโครงสร้างพื้นฐานศูนย์ข้อมูลที่ขับเคลื่อนด้วย AI ในแทสเมเนีย และอาจเป็นหนึ่งในบริษัทเทคโนโลยีที่มีตำแหน่งเชิงกลยุทธ์ที่สุดในออสเตรเลียในขณะนี้

Firmus เป็นพันธมิตรคลาวด์ Nvidia และได้เข้าร่วมตลาด Lepton ของผู้ผลิต GPUบริษัท ได้ออกแบบแพลตฟอร์ม AI Factory แบบแยกส่วนที่เหลวทุกที่เพื่อพัฒนาด้วยสถาปัตยกรรมล่าสุดของ Nvidia รวมถึงเครือข่ายอีเธอร์เน็ต Nvidia Spectrum-X

การระดมทุนในเดือนกันยายน 2025 จำนวน 330 ล้านเหรียญสหรัฐปิดโดยการประเมินมูลค่าหลังการเงิน 1.85 พันล้านเหรียญสำหรับ บริษัทภายในเดือนพฤศจิกายน 2025 หลังจากเพิ่มขึ้นอีก 500 ล้านเหรียญสหรัฐ การประเมินมูลค่าดังกล่าวเพิ่มขึ้นเป็นสามเท่าโดยประมาณ 6 พันล้านเหรียญสหรัฐ.

การลงทุน A$100 ล้านต่อมาจาก Maas Group ในช่วงต้นปี 2026 ยืนยันการประเมินมูลค่าเดือนพฤศจิกายนรายงานว่า Firmus กำลังพิจารณา ASX IPO ภายใน 12 เดือนข้างหน้า และเนื่องจากการประเมินมูลค่าส่วนตัวจำนวน 6 พันล้านเหรียญสหรัฐ การเพิ่มขึ้นของสาธารณะคาดว่าจะสูงกว่ามาก เหรียญพันล้านเหรียญ

ด้วยความต้องการที่เพิ่มขึ้นของออสเตรเลียสำหรับกำลังการคำนวณ AI และความได้เปรียบด้านสภาพอากาศเย็นและพลังงานหมุนเวียนของแทสเมเนียสำหรับการดำเนินงานศูนย์ข้อมูลขนาดใหญ่ Firmus ถือเป็นหนึ่งในผู้สมัคร ASX IPO ที่มีขนาดใหญ่ที่สุดในปี 2026

อย่างไรก็ตาม แม้ว่าความสนใจของตลาดใน Firmus ดูเหมือนจะเพิ่มขึ้น แต่เวลาคือทุกอย่างเมื่อพูดถึง IPOตรวจสอบการยืนยันเวลา IPO ที่แน่นอน ความเชื่อมั่นของศูนย์ข้อมูล AI และ Nvidia ส่งสัญญาณการมีส่วนร่วมมากขึ้นในฐานะนักลงทุนเชิงกลยุทธ์หลังการจดทะเบียนหรือไม่

2.ร็อคต์

Rokt ที่ก่อตั้งขึ้นในซิดนีย์ได้กลายเป็นหนึ่งในบริษัทเทคโนโลยีเอกชนที่มีค่าที่สุดของออสเตรเลียอย่างเงียบ ๆแพลตฟอร์ม Adtech อีคอมเมิร์ซที่มีวัตถุประสงค์เพื่อช่วยให้แบรนด์สร้างรายได้จาก “ช่วงเวลาการทำธุรกรรม” มีมูลค่าอยู่ที่ ~7.9 พันล้านเหรียญสหรัฐ.

เอกสารระยะเวลาที่จัดทำโดย MA Financial คาดการณ์การออก ราคาหุ้น 72 เหรียญสหรัฐ ภายใต้สถานการณ์พื้นฐานเมื่อหุ้นถูกปลดปล่อยจากเงินฝากในเดือนพฤศจิกายน 2027

Rokt คาดว่าจะมีรายชื่อคู่ในสหรัฐอเมริกาและใน ASX ในปี 2026 ซึ่งอาจเป็นไปได้ทันทีในช่วงครึ่งแรกของปีIG โครงสร้างที่กล่าวถึงอย่างกว้างขวางที่สุดคือการจดทะเบียน Nasdaq หลักที่มีโครงสร้าง ASX CDI (CHESS Depository Interest) สำหรับนักลงทุนชาวออสเตรเลีย แทนที่จะเป็นรายการคู่เต็มรูปแบบ

รายได้ของ Rokt สำหรับปีสิ้นสุดเดือนสิงหาคม 2025 คาดว่าจะอยู่ที่ 743 ล้านเหรียญสหรัฐ (เพิ่มขึ้น 48% เมื่อเทียบเป็นรายปี) โดยคาดการณ์ว่า EBITDA อยู่ที่ 100 ล้านเหรียญสหรัฐและอัตรากำไรขั้นต้นประมาณ 43%ปัจจุบันคาดว่าจะข้ามก้าวข้ามรายได้ต่อปีจำนวน 1 พันล้านเหรียญสหรัฐภายในเดือนสิงหาคม 2026

Amazon, Live Nation และ Uber ล้วนรายงานว่าเป็นลูกค้า Rokt และ บริษัท ได้ขยายตัวอย่างรวดเร็วทั่วอเมริกาเหนือและยุโรป

ไม่ว่าRokt จะเลือกจดทะเบียน Nasdaq หลักที่มีโครงสร้าง ASX CDI หรือการจดทะเบียนคู่เต็มรูปแบบอาจส่งผลต่อสภาพคล่องและการเข้าถึงนักลงทุนในท้องถิ่นอย่างมีนัยสำคัญ

3.กรีนครอส

กรีนครอสซึ่งเป็นธุรกิจที่อยู่เบื้องหลัง Petbarn, City Farmers และ Greencross Vets กำลังเตรียมที่จะกลับมาใช้ ASX หลังจากถูกยึดครองส่วนตัวโดย บริษัท ไพรเวทอิควิตี้ของสหรัฐฯ TPG ในปี 2019

ปัจจุบันทีพีจี เป็นเจ้าของกรีนครอส 55% ในขณะที่ออสเตรเลียนซุปเปอร์และแผนบำนาญสุขภาพแห่งออนแทรีโอ (HOOPP) ถือหุ้นส่วนที่เหลือ 45%

บริษัท รายงานรายได้ 2 พันล้านเหรียญสหรัฐสำหรับปีการเงิน 2025 เพิ่มขึ้นเล็กน้อยจาก 1.95 พันล้านเหรียญในปี 2024TPG จ่ายมูลค่าหุ้นจำนวน 675 ล้านเหรียญสหรัฐสำหรับธุรกิจในปี 2019 ขายหุ้น 45% ในปี 2022 โดยมูลค่ามากกว่า 3.5 พันล้านเหรียญสหรัฐIPO ที่เสนอหมายถึงการประเมินมูลค่ามากกว่า 4 พันล้านเหรียญสหรัฐ.

TPG กำหนดเป้าหมายการเสนอขายสาธารณะครั้งแรกอย่างน้อย 700 ล้านเหรียญสหรัฐIPO จะทำเครื่องหมายการกลับมาที่ ASX ของ Greencross หลังจากการขาดงานแปดปีขนาดการเพิ่มขึ้นที่ค่อนข้างเล็กของ TPG แสดงให้เห็นว่าบริษัทมีผลการดำเนินงานหลังการตลาดที่แข็งแกร่งก่อนที่จะออกไปอย่างเต็มที่

การประกาศไทม์ไลน์การออกของ TPG ยังคงเป็นข้อสังเกตว่าการเสนอขายหุ้นประจำปี 2026 จะมีการ์ดหรือไม่และไม่ว่าบริษัทจะดำเนินการ IPO แบบดั้งเดิมหรือการขายการค้าซึ่งยังคงเป็นทางเลือกอื่น

4.มอร์สไมโคร

Morse Micro เป็น บริษัท เซมิคอนดักเตอร์ในซิดนีย์ที่พัฒนาชิป Wi-Fi HaLow ที่ออกแบบมาสำหรับการใช้งาน IoT ในด้านการเกษตร โลจิสติกส์ เมืองอัจฉริยะ และการตรวจสอบอุตสาหกรรม

Morse Micro จัดรอบซีรีส์ C ในเดือนกันยายน 2025 โดยระดมทุน 88 ล้านเหรียญสหรัฐ ตามมาในเดือนพฤศจิกายน 2025 โดยมีการระดมทุนก่อนIPO จำนวน 32 ล้านเหรียญสหรัฐ ทำให้เงินทุนรวมสูงสุดลง 300 ล้านเหรียญสหรัฐ.

กำลังกำหนดเป้าหมายรายการ ASX ในอีก 12—18 เดือนข้างหน้าซีรีส์ C นำโดย MegaChips ยักษ์ใหญ่ชิปญี่ปุ่น และ บริษัท กองทุนฟื้นฟูแห่งชาติ

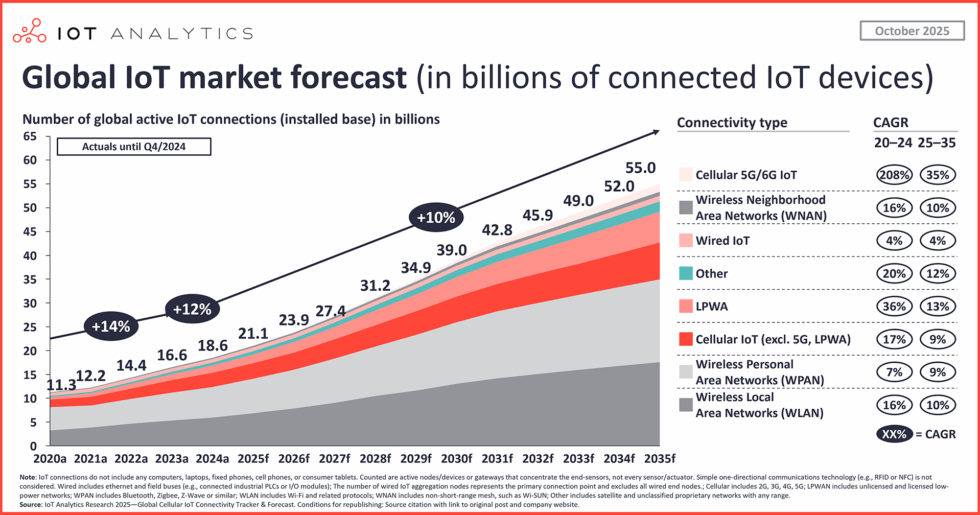

การเชื่อมต่ออุปกรณ์ IoT ทั่วโลกคาดการณ์ว่าจะเกิน 30 พันล้านภายในปี 2030 และ Morse Micro จะเป็น บริษัท เซมิคอนดักเตอร์แบบเล่นแบบแท้จริง ASX ซึ่งอาจดึงดูดความสนใจอย่างมากจากผู้จัดการกองทุนที่เน้นเทคโนโลยี

การดึงดูดรายได้ของ Morse Micro กับพันธมิตรฮาร์ดแวร์ระดับหนึ่งก่อนการลงทะเบียนเป็นสิ่งที่ต้องระวัง และบริษัทจะแสวงหาการจดทะเบียนในสหรัฐอเมริกาพร้อมกันหรือไม่ เนื่องจากความอยากของนักลงทุนเซมิคอนดักเตอร์ของสหรัฐฯ

5.ทรัพยากรไบสัน

Bison Resources เป็นนักสำรวจทองคำและโลหะมีค่าที่เน้นสหรัฐฯที่เพิ่งเข้าจดทะเบียนใหม่ซึ่งปัจจุบันอยู่ในช่วงกลางของการเสนอขายหุ้นสามัญของ ASX

ข้อเสนอปิดในวันที่ 20 มีนาคม 2026 โดยมีเป้าหมายการลงทะเบียน ASX ในช่วงกลางเดือนเมษายน 2026ในฐานะการลงทุนทางการตลาดที่บ่งชี้ของ 13.25 ล้านเหรียญสหรัฐ เมื่อสมัครสมาชิกเต็มรูปแบบ Bison เป็นชื่อเก็งกำไรมากที่สุดในรายการนี้โดยมีส่วนต่างที่สำคัญ

บริษัทมีโครงการสำรวจสี่โครงการในภาคตะวันออกเฉียงเหนือของเนวาดาภายใน Carlin Trend (หนึ่งในสายพานที่ผลิตทองคำที่อุดมสมบูรณ์ที่สุดในโลก) ซึ่งรับผิดชอบในการผลิตทองคำประมาณ 75% ของสหรัฐฯ

IPO พยายามระดมทุน A$4.5 เป็น 5.5 ล้านเหรียญสหรัฐ (22.5 ถึง 27.5 ล้านหุ้น ที่ 0.20 เหรียญสหรัฐต่อหุ้น)ทีมนี้มีประสบการณ์ก่อนหน้านี้ที่ Sun Silver (ASX: SS1) และ Black Bear Minerals ทำให้มีประวัติการแข่งขันในรายชื่อเหมืองแร่เยาวชน ASX จากเนวาดา

IPO ทั่วโลก: IPO ที่ใหญ่ที่สุดที่เกิดขึ้นทั่วโลกในปี 2026 คืออะไร

บรรทัดล่าง

ปฏิทิน IPO 2026 ของออสเตรเลียครอบคลุมถึงสเปกตรัมความเสี่ยงเต็มรูปแบบการเล่นโครงสร้างพื้นฐาน AI ที่รองรับ NVIDIA แพลตฟอร์มอีคอมเมิร์ซมูลค่าพันล้านดอลลาร์ และนักสำรวจทองคำรุ่นเยาวชนที่มีการเสนอขายหุ้น IPO อยู่แล้ว

ผู้สมัครแต่ละคนสะท้อนถึงระยะเวลาที่แตกต่างกันและโปรไฟล์นักลงทุนที่แตกต่างกันพวกเขาร่วมกันแนะนำว่า ASX สามารถเห็นการฉีดรายการใหม่ที่มีความหมายในทุกภาคส่วนที่ส่วนใหญ่ขาดจากตลาดท้องถิ่นในช่วงไม่กี่ปีที่ผ่านมา

Reportingdates and release times are based on company investor relations calendars whereconfirmed. Where dates or times are not marked confirmed, they are GO Marketsestimates. Consensus EPS, revenue and analyst-range data are sourced fromBloomberg and Earnings Whispers, as at 09 July 2026 (AEST). Company guidance,backlog and operating metrics are sourced from the latest company filings orresults presentations, unless stated otherwise. Any scenario analysis reflectsGO Markets analysis. Figures and schedules may change without notice.

The information provided is of general nature only and does not take into account your personal objectives, financial situations or needs. Before acting on any information provided, you should consider whether the information is suitable for you and your personal circumstances and if necessary, seek appropriate professional advice. All opinions, conclusions, forecasts or recommendations are reasonably held at the time of compilation but are subject to change without notice. Past performance is not an indication of future performance. Go Markets Pty Ltd, ABN 85 081 864 039, AFSL 254963 is a CFD issuer, and trading carries significant risks and is not suitable for everyone. You do not own or have any interest in the rights to the underlying assets. You should consider the appropriateness by reviewing our TMD, FSG, PDS and other CFD legal documents to ensure you understand the risks before you invest in CFDs.