.jpg)

US markets are eyeing all-time highs following strong data and earnings reports. Whether these records are achieved will depend on the news flow over the coming days, particularly from the Federal Reserve.

Fed Decision Incoming

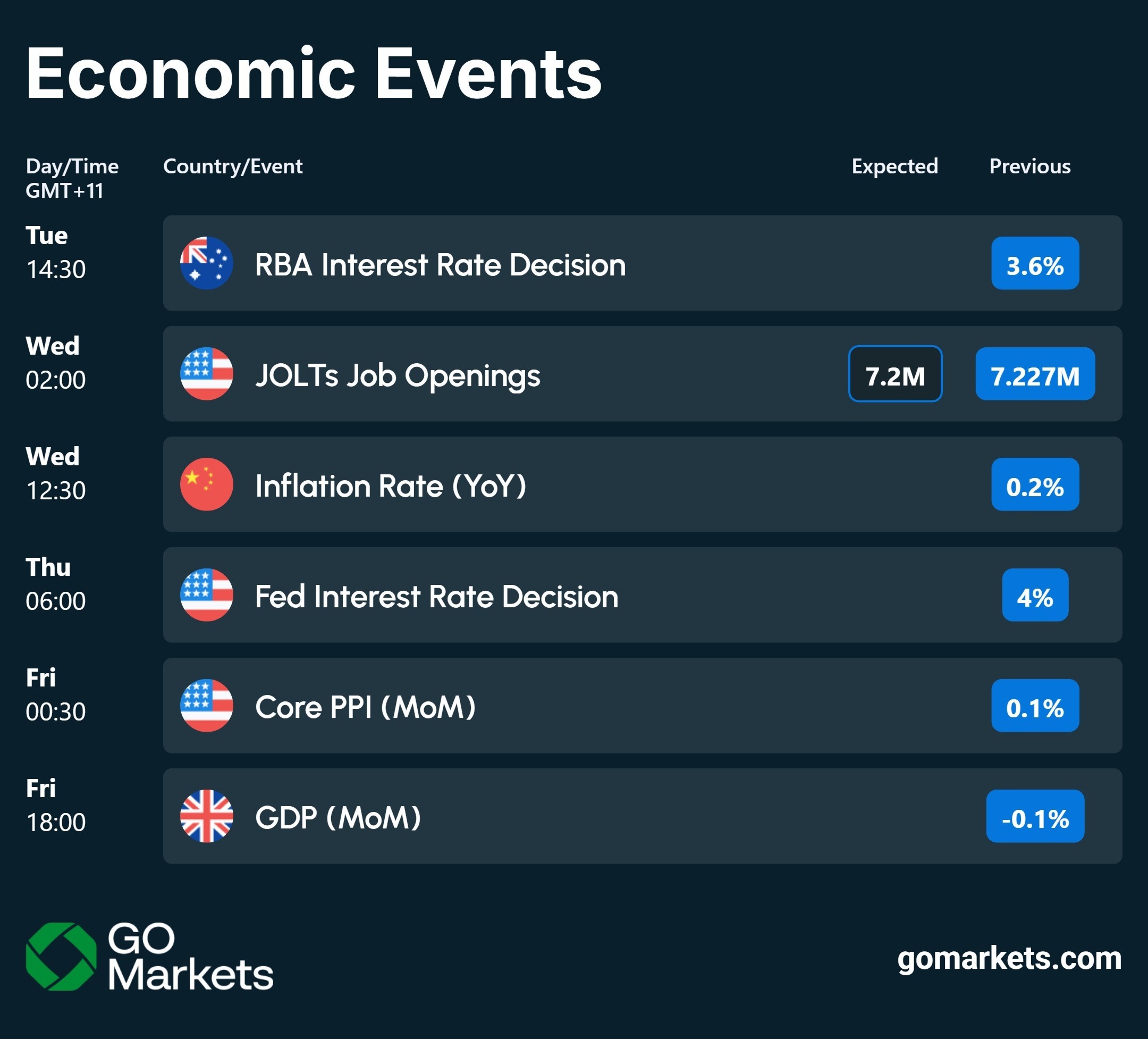

The Federal Reserve's two-day meeting will end this Wednesday with a 0.25% rate cut widely expected. But following Friday's encouraging PCE numbers, the bigger question is “Will there be a January cut?” The Fed press conference post-decision will likely the highest signal event for the rest of 2025.

Central Bank Decisions Everywhere

Beyond the Fed, the Reserve Bank of Australia meets tomorrow with a pause expected, as recent data hasn't provided sufficient incentive for another cut. The ECB, Bank of England, and Bank of Japan will also all announce decisions within the next ten days, creating potential volatility across both equity and FX markets.

Big Tech Earnings

Two major AI infrastructure players report earnings this week: Broadcom and Oracle. These reports come at a time when AI valuations are under heavy public scrutiny, however, they will likely take a backseat to whatever the Fed signals about its 2026 path.

Copper Breaks Out

Copper has rallied to a four-month high and is now testing the $5.50 level. After breaching the key $5.25 support level, the market is showing some hesitation in Asia ahead of major data releases and the Fed decision. The July record highs of $5.50 are now within reach, though it is still to be seen if this level holds or if we pull back toward $5.25 support.

Market Insights

Watch Mike Smith's analysis of the week ahead in markets.

Key Economic Events

Stay up to date with the key economic events for the week.

The information provided is of general nature only and does not take into account your personal objectives, financial situations or needs. Before acting on any information provided, you should consider whether the information is suitable for you and your personal circumstances and if necessary, seek appropriate professional advice. All opinions, conclusions, forecasts or recommendations are reasonably held at the time of compilation but are subject to change without notice. Past performance is not an indication of future performance. Go Markets Pty Ltd, ABN 85 081 864 039, AFSL 254963 is a CFD issuer, and trading carries significant risks and is not suitable for everyone. You do not own or have any interest in the rights to the underlying assets. You should consider the appropriateness by reviewing our TMD, FSG, PDS and other CFD legal documents to ensure you understand the risks before you invest in CFDs. These documents are available here.

免责声明:文章来自 GO Markets 分析师和参与者,基于他们的独立分析或个人经验。表达的观点、意见或交易风格仅代表作者个人,不代表 GO Markets 立场。建议,(如有),具有“普遍”性,并非基于您的个人目标、财务状况或需求。在根据建议采取行动之前,请考虑该建议(如有)对您的目标、财务状况和需求的适用程度。如果建议与购买特定金融产品有关,您应该在做出任何决定之前了解并考虑该产品的产品披露声明 (PDS) 和金融服务指南 (FSG)。

.jpg)