上周的影响与广告一样重要。澳洲联储加息,美联储坚持加息,在有报道称以色列袭击伊朗南帕尔斯天然气田之前,市场几乎没有时间处理任何加息。

未来一周的央行决策将减少,但对市场可能同样重要。Flash PMI将首次广泛了解这场战争是否已经出现在商业信心中。澳大利亚2月份的消费者价格指数是对澳洲联储下一步行动最重要的国内数据点。而石油市场仍然是主要的宏观变量。

事实速览

- 在以色列首次袭击伊朗南帕尔斯天然气田后,布伦特原油价格飙升至每桶110美元以上。

- 澳大利亚、日本、欧元区、英国和美国的初步采购经理人指数均在周二公布。

- 澳大利亚2月份消费者价格指数周三公布,这是自澳洲联储连续加息以来的首次通胀数据。

石油:从危机到紧急情况

上周石油局势严重恶化。自2月28日战争爆发以来,布伦特原油已经飙升了约80%。

3月18日对伊朗南帕尔斯天然气田的袭击是上游石油和天然气基础设施首次成为攻击目标。

伊朗对袭击的回应是威胁要瞄准沙特阿拉伯、阿联酋和卡塔尔各地的设施。如果这些威胁中的任何一个得到实施,全球石油冲击将从供应中断升级为对该地区产能的直接攻击。

分析师现在表示,150美元的布伦特原油是可以实现的,200美元不在可能范围之内。1970年代的阿拉伯石油禁运导致价格翻了三番,高级能源主管已经用这些术语描述了当前的冲击。

对于本周的市场而言,石油是主要变量。任何停火、外交进展或恢复霍尔木兹航运的信号都可能引发油价的回调。伊朗对海湾基础设施的任何袭击都可能使它们走高。

监视器

- 通过霍尔木兹海峡的每日船只过境次数。

- 伊朗对海湾基础设施的报复,对沙特或阿联酋设施的袭击将是重大升级。

- 美国和欧洲的IEA储备何时以及如何进入市场。

- 卡塔尔南帕尔斯的中断正在影响欧洲液化天然气市场。

- 特朗普的言论可能导致盘中油价波动。

全球采购经理人指数快报:关于处于战争状态的经济的第一篇读物

周二同时公布了所有主要经济体3月份的标准普尔全球采购经理人指数初值估计。

这将是第一个记录制造商和服务公司如何应对超过100美元的石油、霍尔木兹海峡封锁以及中东战争造成的更广泛不确定性的数据集。

每个经济体的关键问题是,油价飙升和战争的不确定性是否削弱了商业信心,抑制了新订单或将投入价格指数推至多年来的新高。

鉴于在大多数经济体的调查窗口关闭之前,石油价格已突破100美元,因此投入成本读数可能会大幅上升。

关键日期

- 标普全球快报澳大利亚采购经理人指数: 澳大利亚东部夏令时间3月24日星期二上午9点

- 标普全球快报日本采购经理人指数: 澳大利亚东部夏令时间3月24日星期二上午11点30分

- 汇丰银行印度采购经理人指数简报: 澳大利亚东部夏令时间3月24日星期二下午 4:00

- HCOB Flash 法国采购经理人指数: 澳大利亚东部夏令时间3月24日星期二晚上 7:15

- HCOB Flash 德国采购经理人指数: 澳大利亚东部夏令时间3月24日星期二晚上 7:30

- HCOB 欧元区采购经理人指数简报: 澳大利亚东部夏令时间3月24日星期二晚上 8:00

- 标普全球快报英国采购经理人指数: 澳大利亚东部夏令时间3月24日星期二晚上 8:30

- 标普全球快报美国采购经理人指数: 澳大利亚东部夏令时间3月25日星期三上午12点45分

监视器

- 制造业和服务业中任何多年高点的输入价格组成部分。

- 衡量战争冲击在多大程度上削弱了前瞻预期的商业信心指数。

- 新订单是未来产出的指标;急剧下降可能预示着需求正在受到破坏。

- 美国综合采购经理人指数:已经是2月份主要经济体中最疲软的数据,另一个软数据可能会敲响增长的警钟。

霍尔木兹危机解释

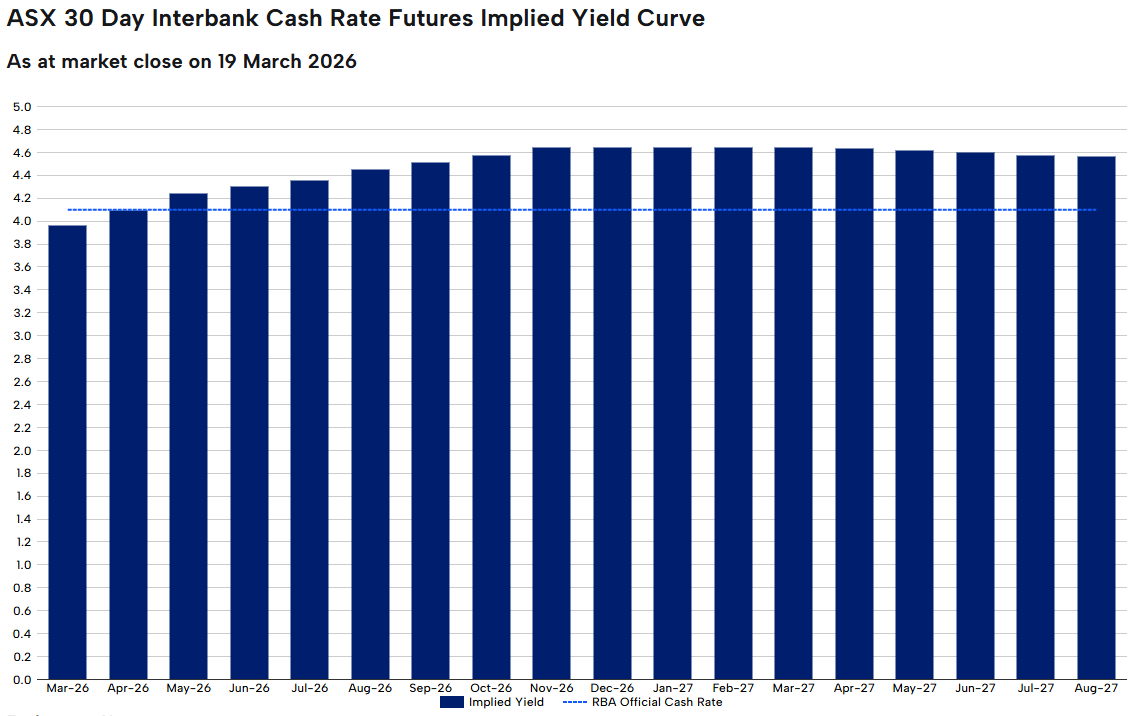

澳大利亚:又一次加息了吗?

澳洲联储于3月17日连续第二次会议上调,以5票对4票的微弱票数将现金利率提高至4.10%。

布洛克州长将其描述为一场 “非常活跃的讨论”,政策方向不成问题,只是时机问题。

本周将公布的2月份消费者价格指数作为反映任何石油冲击的第一手数据。扣除包括燃料在内的挥发性物质的调整后的均值将是澳洲联储最密切关注的数字。高于3.5%的读数可能会巩固5月份加息的理由。较为温和的结果可能会使暂停的论点死灰复燃。

澳新银行和澳大利亚国民银行都表示预计5月份将进行第三次加息,使现金利率达到4.35%。

关键日期

- ABS 消费者价格指数(CPI): 澳大利亚东部夏令时间3月25日星期三上午11点30分

监视器

- 削减后的平均通货膨胀率是澳洲联储的首选衡量标准。

- 可以将石油冲击与国内价格压力区分开来的燃料和能源成分。

- 住房和服务通货膨胀是推动澳洲联储长期担忧的粘性因素。

准备好在主要交易之外进行交易了吗?

开设一个账户 · 登录

The information provided is of general nature only and does not take into account your personal objectives, financial situations or needs. Before acting on any information provided, you should consider whether the information is suitable for you and your personal circumstances and if necessary, seek appropriate professional advice. All opinions, conclusions, forecasts or recommendations are reasonably held at the time of compilation but are subject to change without notice. Past performance is not an indication of future performance. Go Markets Pty Ltd, ABN 85 081 864 039, AFSL 254963 is a CFD issuer, and trading carries significant risks and is not suitable for everyone. You do not own or have any interest in the rights to the underlying assets. You should consider the appropriateness by reviewing our TMD, FSG, PDS and other CFD legal documents to ensure you understand the risks before you invest in CFDs.