China data, US inflation updates, earnings, and geopolitics in play | GO Markets week ahead

Mike Smith

16/1/2026

•

0 min read

Share this post

Copy URL

Markets are navigating a familiar mix of macro and event risk with China growth signals, US inflation updates, central-bank guidance and earnings that will help confirm whether the growth narrative is broadening or narrowing.

At a glance

China: Q4 GDP + December activity + PBOC decision

US: PCE inflation (date per current BEA schedule)

Japan: BOJ decision (JPY/carry sensitivity)

Earnings: tech, industrials, energy, materials in focus

Gold: near record highs (yields/USD/geopolitics watch)

Geopolitics remain fluid. Any escalation could shift risk sentiment quickly and produce price action that diverges from current baselines.

China

China Q4 GDP: Monday, 19 January at 1:00 pm (AEDT)

Retail sales: Monday, 19 January at 1:00 pm (AEDT)

PBOC policy decision: Monday, 19 January at 12.30 pm (AEDT)

China’s Q4 GDP and December activity data, together with the PBOC decision, will shape expectations for China's growth momentum and the durability of policy support.

Market impact

Commodity-linked FX: AUD and NZD may react if growth expectations or the policy tone shifts.

Equities: The Shanghai Composite, Hang Seng and ASX 200 could respond to any change in how investors view demand and stimulus traction.

Commodities: Industrial metals and oil may move on any reassessment of China-linked demand.

US

PCE Inflation: Friday, 23 January at 2:00 am (AEDT)

PSI: Friday, 23 January at 2:00 am (AEDT)

S&P Flash (PMI): Saturday, 24 January at 1:45 am (AEDT)

Netflix: Tuesday, 20 January 2026 at 8:00 am (AEDT)

The personal consumption expenditures (PCE) price index is the Federal Reserve’s preferred inflation gauge and a key input for rate expectations and (by extension) Treasury yields, the USD, and growth stocks. Markets are likely to focus on whether the reading changes the inflation path that is currently priced, rather than simply matching consensus.

Market impact

USD: May move if rate expectations shift, particularly against JPY and EUR.

US equities: Growth and small caps, including the Nasdaq and Russell 2000, may be sensitive if the data or interpretation challenge the current rate outlook.

Gold futures: May be influenced indirectly via moves in Treasury yields and the USD.

Japan

Key reports

Inflation: Friday, 23 January at 10:30 am (AEDT)

Bank of Japan (BoJ) Interest Rate Meeting: Friday, 23 January at ~2:00 pm (AEDT)

Markets will focus on what the BOJ signals about inflation, wages and the policy path. A shift in tone can move JPY quickly and flow through to broader risk via carry positioning.

Market impact:

JPY/USD pairs and crosses: Pairs are sensitive to any guidance change and the USD/JPY has broken above 158, but the move could reverse if the BOJ strikes a more hawkish tone.

Japan equities and global sentiment: Could react if the dynamics shift.

Broader risk assets: May be influenced via moves in the USD and volatility conditions.

Netflix: Tuesday, 20 January 2026 at 8:00 am (AEDT)

Johnson & Johnson: Wednesday, 21 January at 10:20 pm (AEDT)

Intel Corporation: Thursday, 22 January at 8:00 am (AEDT)

A busy week of US earnings is expected with large-cap names across multiple sectors reporting. Early results and, importantly, forward guidance may help clarify whether growth is broadening or becoming more selective.

With the S&P 500 close to the psychological 7,000 level, earnings could be a catalyst for a fresh test of highs or a pullback if guidance disappoints.

Market impact

Upside scenario: Results that exceed expectations and are supported by steady guidance could support sector and broader market sentiment.

Downside scenario: Cautious guidance, particularly on margins and capex, could weigh on individual names and spill into broader indices if it becomes a repeated message.

Read-through: Early reporters in each sector may influence expectations for related stocks, especially where peers have not yet provided updated guidance.

Bottom line: This is a week where the market may trade the forward picture more than the rear-view numbers. The key is whether guidance supports the idea of broad, durable growth, or whether it points to a more selective backdrop as 2026 unfolds.

Continued strength in gold may support gold equities and gold-linked ETFs relative to the broader market but geopolitical developments and policy uncertainty may influence demand for defensive assets.

A sustained reversal in gold could be interpreted by some market participants as a sign of improved risk confidence. The driver set matters, especially whether the move is led by yields, USD strength, or a fade in event risk.

Mike Smith (MSc, PGdipEd)

Client Education and Training

Los artículos son elaborados por analistas y colaboradores de GO Markets y se basan en su propio análisis independiente o en sus experiencias personales. Las opiniones, puntos de vista o estilos de trading expresados son propios de los autores y no deben considerarse como representativos de, ni compartidos por, GO Markets. Cualquier consejo proporcionado es de carácter “general” y no tiene en cuenta tus objetivos, situación financiera ni necesidades personales. Considera si dicho consejo es adecuado para tus objetivos, situación financiera y necesidades antes de actuar sobre él. Si el consejo se refiere a la adquisición de un producto financiero en particular, debes obtener nuestra Declaración de Divulgación (Disclosure Statement, DS) y otros documentos legales disponibles en nuestro sitio web antes de tomar cualquier decisión.

La volatilidad no discrimina. Pero puede castigar a los no preparados.

Detiene ser golpeado en movimientos que se invierten en cuestión de minutos. Las primas en opciones de fecha corta están subiendo. Y el yen ya no se comportaba como el seto confiable que alguna vez fue.

Para los comerciantes de toda Asia, navegar por este entorno significa hacer preguntas más difíciles sobre el riesgo, el tiempo y las suposiciones incorporadas en estrategias creadas para mercados más tranquilos.

1. ¿Cómo puedo operar con CFDs VIX durante un choque geopolítico?

El Índice de Volatilidad CBOE (VIX) mide la expectativa del mercado de volatilidad implícita a 30 días en el S&P 500. A menudo se le llama el “indicador del miedo”. Durante los choques geopolíticos como las actuales escaladas de Irán, los anuncios de sanciones y las acciones sorpresa de los bancos centrales, el VIX puede repuntar bruscamente y rápidamente.

¿Qué hace que los CFDs de VIX sean diferentes en un shock?

VIX en sí no es comercializable directamente. Los CFD de VIX suelen tener un precio de los futuros de VIX, lo que significa que tienen un arrastre de contango en condiciones normales.

Durante un choque geopolítico, varias cosas pueden suceder a la vez

El Spot VIX puede repuntar inmediatamente mientras que los futuros a corto plazo se quedan rezagados, creando una desconexión.

Los diferenciales de los CFDs de VIX pueden ampliarse significativamente a medida que disminuye la liquidez.

Los requerimientos de margen pueden cambiar intradiamente a medida que se ajustan los modelos de riesgo de los brókers.

VIX tiende a la reversión promedio después de los picos, por lo que el tiempo y la duración son críticos.

Lo que esto significa para los comerciantes de horas asiáticas

Las horas del mercado asiático significan que muchos eventos geopolíticos pueden romperse mientras los comerciantes locales están activos o apenas comienzan su sesión.

Una conmoción que golpea durante las horas de Tokio ya podría estar cotizada en futuros de VIX antes de la apertura de Sydney.

Algunos operadores utilizan las posiciones VIX CFD como una cobertura a corto plazo contra las carteras de acciones en lugar de una operación direccional. Otros negocian la reversión (el retroceso hacia promedios históricos una vez que el pico inicial se desvanece). Ambos enfoques conllevan riesgos distintos, y ninguno garantiza un resultado específico.

Índice de volatilidad (VIX) durante la escalada del conflicto del 1 de marzo en Irán | TradingView

2. ¿Por qué mis primas de opciones 0DTE son tan caras en este momento?

Las opciones de cero días hasta el vencimiento (0DTE) expiran el mismo día en que se negocian. Se han convertido en uno de los segmentos de más rápido crecimiento del mercado de opciones, representando ahora más del 57% del volumen diario de opciones del S&P 500 según datos de mercados globales de Cboe.

Para los participantes con sede en Asia que acceden a los mercados de opciones de Estados Unidos, las primas elevadas durante períodos volátiles pueden sentirse como un mal precio, pero por lo general reflejan factores estructurales de precios.

¿Por qué las primas se repuntan?

El precio de las opciones está impulsado por el valor intrínseco y el valor de tiempo. Para las opciones 0DTE, casi no queda valor de tiempo, lo que podría sugerir que deberían ser baratas pero el componente implícito de volatilidad compensa eso.

Cuando aumenta la incertidumbre, los vendedores pueden exigir una mayor compensación por el riesgo de movimientos intradía brusca.

Esto puede reflejarse en

Insumos de mayor volatilidad implícita.

Mayor margen de puda-tarea.

Ajustes más rápidos en cobertura delta y gamma.

En entornos de VIX más alto, los flujos de cobertura pueden contribuir a los bucles de retroalimentación a corto plazo en el índice subyacente. Esto puede amplificar las oscilaciones de precios, particularmente en torno a niveles clave.

Lo que esto significa para los comerciantes de horas asiáticas

Muchos contratos de opciones 0DTE ven sus flujos de precios y cobertura más activos durante las horas de negociación de EE. UU. Ingresar posiciones durante la sesión asiática puede significar enfrentar precios obsoletos o diferenciales más amplios.

Si está viendo primas costosas, puede reflejar que el mercado esté valorando con precisión el riesgo de una mudanza grande el mismo día. Si vale la pena pagar esa prima depende de su visión del rango intradiario probable y su tolerancia al riesgo, no solo de la cifra absoluta en dólares.

3. ¿Cómo ajusto mi bot de trading algorítmico para un entorno con alto nivel de VIX?

Muchos sistemas de comercio algorítmico se basan en parámetros calibrados durante regímenes de baja volatilidad. Cuando VIX alcanza picos, esos parámetros pueden quedar obsoletos rápidamente.

El problema del desajuste del régimen

La mayoría de los algoritmos comerciales utilizan datos históricos para establecer tamaños de posición, distancias de parada y umbrales de entrada. Esos datos reflejan las condiciones durante las cuales se probó el sistema. Si VIX pasa de 15 a 35, es posible que las suposiciones estadísticas que sustentan esas configuraciones ya no se mantengan.

Los modos de falla comunes en entornos con alto nivel de VIX incluyen

Se detiene repetidamente provocada por el ruido antes de que se produzca el movimiento direccional previsto.

Dimensionamiento de posiciones basado en el riesgo fijo en dólares, que se vuelve relativamente pequeño en comparación con los rangos intradiarios reales.

Supuestos de correlación entre activos desglosando.

Deslizamiento en la ejecución que erosiona el borde.

Enfoques que algunos comerciantes algorítmicos consideran

En lugar de ejecutar un único conjunto fijo de parámetros, algunos sistemas incorporan un filtro de régimen de volatilidad. Esta es una verificación en tiempo real en VIX o ATR que activa un interruptor a diferentes configuraciones cuando cambian las condiciones.

Ajustes de enfoque que algunos operadores revisan en entornos con alto nivel de VIX

Ampliar las distancias de parada proporcionalmente al ATR para reducir las salidas impulsadas por ruido.

Reducir el tamaño de la posición para mantener el riesgo constante en dólares en relación con rangos esperados más amplios.

Agregue un umbral VIX por encima del cual el sistema hace una pausa o se mueve al modo de comercio en papel.

Reducir el número de posiciones simultáneas, ya que las correlaciones tienden a aumentar durante el estrés del mercado.

Ningún ajuste elimina el riesgo. El backtesting de nuevos parámetros en períodos históricos de alto VIX puede proporcionar alguna indicación del probable desempeño, aunque las condiciones pasadas no son una guía confiable para los resultados futuros.

4. ¿Sigue siendo el yen japonés (JPY) un comercio seguro confiable?

Durante los períodos de aversión al riesgo global, el capital históricamente ha fluido hacia el JPY a medida que los inversores se desenrollan en las operaciones de carry y buscan tenencias de menor volatilidad. No obstante, la confiabilidad de esta dinámica se ha vuelto más condicional.

¿Por qué el yen se ha movido históricamente como un refugio seguro?

Las tasas de interés históricamente bajas de Japón hicieron del JPY la moneda de financiamiento preferida para las operaciones de carry y cuando llega el sentimiento de riesgo, esas operaciones se desenrollan rápidamente, creando demanda de yen.

Además, la gran posición neta de activos extranjeros de Japón significa que los inversores japoneses tienden a repatriar capital durante las crisis, apoyando aún más al JPY.

Lo que ha cambiado

El alejamiento del Banco de Japón de la política monetaria ultra flexible en los últimos años ha complicado la dinámica tradicional de refugio seguro.

A medida que aumentan las tasas de interés japonesas:

La escala de posicionamiento de carry trade puede cambiar.

El USD/JPY puede volverse más sensible a los diferenciales de las tasas de interés.

La comunicación del BoJ y los datos de inflación interna pueden influir en el JPY independientemente del apetito de riesgo global.

El yen aún puede comportarse como un refugio seguro, particularmente durante las fuertes vendas de acciones. Pero puede responder de manera más lenta o inconsistente en comparación con ciclos anteriores cuando la divergencia política entre Japón y el resto del mundo era más extrema.

Qué ver

Para los comerciantes que monitorean el JPY como una señal de refugio seguro, las fechas de reunión del BoJ, las publicaciones del IPC japonés y los datos de spread de tasas entre Estados Unidos y Japón en tiempo real se han convertido en insumos más relevantes que hace unos años.

Las tasas de Japón subieron a lo positivo en 2024 después de años en -0.1% | Economía comercial

5. ¿Cómo evito los 'azotes' en los CFDs sobre energía?

Whipsawing describe la experiencia de ingresar a una operación en una dirección, ser detenido a medida que el precio se invierte, luego ver el precio retroceder en la dirección original.

Los CFDs sobre energía, particularmente el petróleo crudo, son especialmente propensos a esto en los mercados volátiles. Y para los comerciantes en Asia, la combinación de poca liquidez durante el horario local y sensibilidad a los titulares geopolíticos puede hacer que esto sea particularmente desafiante.

¿Por qué los CFDs de energía whipsaw?

El petróleo crudo es sensible a una amplia gama de impulsores generales: decisiones de producción de la OPEP+, datos de inventario de Estados Unidos, interrupciones geopolíticas del suministro y movimientos de divisas.

En entornos de alta volatilidad, el mercado puede reaccionar fuertemente a cada titular antes de dar marcha atrás cuando llegue el siguiente.

Los picos de precios en un titular, las paradas se activan en posiciones cortas.

Los comerciantes vuelven a entrar largo tiempo, esperando continuación.

Un segundo titular o toma de ganancias revierte la jugada.

Se golpean paradas largas. El ciclo se repite.

Enfoques que los comerciantes pueden considerar para administrar el riesgo de Whipsaw

Algunos comerciantes optan por cambiar sus controles de riesgo en condiciones volátiles (por ejemplo, revisar la colocación de stop en relación con las medidas de volatilidad). Sin embargo, estos pueden aumentar las pérdidas; los riesgos de ejecución y deslizamiento pueden aumentar considerablemente en los mercados rápidos.

Otros enfoques que algunos comerciantes revisan:

Evite operar con CFD de petróleo crudo en los 30 minutos antes y después de las principales publicaciones de datos programadas.

Utilice un gráfico de plazos más largo para identificar la tendencia predominante antes de entrar en un período de tiempo más corto, lo que reduce la posibilidad de operar contra flujos institucionales más grandes.

Escale a posiciones en etapas en lugar de comprometer el tamaño completo en la entrada inicial.

Monitoree el interés abierto y el volumen para distinguir entre movimientos con participación genuina y faltas de baja liquidez.

Los latiguillos no se pueden eliminar por completo en los mercados energéticos volátiles. El objetivo de la administración de riesgos en estas condiciones no es predecir qué movimientos se mantendrán, sino asegurar que las pérdidas en movimientos falsos sean menores que las ganancias cuando sigue un movimiento direccional genuino.

Consideraciones prácticas para los mercados asiáticos volátiles

Los mercados asiáticos tienen características estructurales que interactúan con la volatilidad de manera diferente a los mercados estadounidenses o europeos:

Una liquidez más delgada durante el horario local puede exagerar los movimientos en volúmenes delgados, particularmente en CFDs de energía y FX.

Los eventos en China, incluidas las publicaciones del PMI, los datos comerciales y las señales de política del PBOC, pueden mover los índices regionales.

Las decisiones políticas del BoJ se han convertido en un impulsor más activo de la volatilidad del JPY y el Nikkei en los últimos años.

Las brechas de la noche a la mañana de los movimientos de la sesión de Estados Unidos son un riesgo estructural persistente para los operadores que no pueden monitorear las posiciones durante todo el día.

Los requerimientos de margen de los productos apalancados pueden cambiar a corto plazo durante los períodos de alto VIX.

Preguntas frecuentes sobre la volatilidad en los mercados asiáticos

¿Qué significa una lectura alta de VIX para los índices bursátiles asiáticos?

VIX mide la volatilidad esperada en el S&P 500, pero las lecturas elevadas suelen reflejar la aversión global al riesgo que fluye a través de los mercados. Los índices asiáticos como el Nikkei 225, Hang Seng y ASX 200 a menudo pueden ver una mayor volatilidad y correlación negativa con fuertes picos de VIX.

¿Se pueden negociar las opciones de 0DTE durante el horario asiático?

El acceso depende de la plataforma y del instrumento específico. Las opciones del índice de acciones 0DTE de EE. UU. tienen un precio más activo durante las horas de negociación de Estados Unidos. Los comerciantes asiáticos pueden enfrentar diferenciales más amplios y precios menos representativos fuera de esas horas.

¿Las estrategias algorítmicas de trading son inherentemente más riesgosas en condiciones de alta volatilidad?

Las estrategias calibradas durante períodos de baja volatilidad pueden funcionar de manera diferente en entornos de alto VIX. La revisión periódica de los parámetros frente a las condiciones actuales del mercado es prudente para cualquier enfoque sistemático.

¿El comercio de refugio seguro del JPY ha cambiado permanentemente?

La normalización de las políticas del Banco de Japón ha introducido nuevas dinámicas, pero el JPY ha seguido fortaleciéndose durante algunos episodios de riesgo. Puede estar más condicionado a la naturaleza del choque y a la postura concurrente del BoJ.

¿Cuál es la mejor manera de establecer paradas en los CFDs de energía en condiciones de alta volatilidad?

No existe un método universalmente mejor. Muchos comerciantes hacen referencia a ATR para calibrar las distancias de parada a las condiciones prevalecientes en lugar de usar niveles fijos. Esto no garantiza la salida al precio deseado y no elimina el riesgo de whipsaw.

La volatilidad tiene una forma de aparecer sin invitación.

Un día el ASX está a la deriva silenciosamente... y al siguiente, los requisitos de margen aumentan, las paradas no llenan donde se esperaba, y las carteras se abren con incómodas brechas de la noche a la mañana.

Si has estado buscando respuestas, no estás solo. Algunas de las preguntas más buscadas sobre la volatilidad entre los comerciantes australianos se relacionan con llamadas de margen, deslizamiento, brechas nocturnas, fondos cotizados en bolsa apalancados (ETF) y herramientas como promedio true range (ATR).

Esto es lo que está pasando.

Por qué esto es importante ahora

Los mercados mundiales se han vuelto más sensibles a las tasas de interés, los datos de inflación, la geopolítica y los flujos impulsados por la tecnología. Cuando la liquidez se hace más baja y la incertidumbre sube, las oscilaciones de precios se ensanchan. Eso es volatilidad.

Y la volatilidad no solo afecta la dirección de los precios, sino que cambia la forma en que se ejecutan las operaciones, cuánto capital se requiere y cómo se comporta el riesgo debajo de la superficie.

Traducción: La volatilidad no se trata solo de movimientos más grandes, más bien, se trata de movimientos más rápidos y liquidez más delgada, ahí es cuando más importa la mecánica del trading.

¿Por qué mi broker aumentó los requerimientos de margen?

Una de las preguntas más buscadas sobre la volatilidad es por qué los requerimientos de margen aumentan sin previo aviso.

Cuando los mercados se vuelven inestables, los corredores pueden aumentar los requerimientos de margen en los contratos por diferencia (CFDs) y otros productos apalancados. Las oscilaciones de precios mayores pueden aumentar el riesgo de que las cuentas pasen a acciones negativas, por lo que aumentar los requerimientos de margen reduce el apalancamiento disponible y puede ayudar a administrar la exposición durante condiciones extremas.

Lo que esto puede significar en la práctica

-Una llamada de margen puede ocurrir incluso si el precio no se ha movido significativamente. -El apalancamiento efectivo puede caer rápidamente. -Es posible que sea necesario reducir las posiciones con poca antelación.

Los ajustes de margen suelen ser una respuesta al riesgo cambiante del mercado, no una decisión aleatoria. En mercados altamente volátiles, es prudente asumir que los ajustes de margen pueden cambiar rápidamente, por lo tanto, muchos operadores optan por revisar los tamaños de posición y los buffers disponibles a la luz de ese riesgo.

¿Qué es el deslizamiento y por qué mi stop no llenó a mi precio?

Otro tema que se busca con frecuencia es el deslizamiento.

El deslizamiento puede ocurrir cuando una orden de stop se activa y se ejecuta al siguiente precio disponible, el resultado puede depender del tipo de orden, liquidez del mercado y brechas. En los mercados tranquilos, la diferencia puede ser pequeña mientras que en los mercados rápidos, los precios pueden dispararse más allá del nivel de parada.

Ilustración de la brecha de precios a través del nivel stop-loss | GO Markets

Los controladores comunes incluyen

-Principales liberaciones económicas o de ganancias. -Liquidez delgada. -Niveles de parada abarrotados. -Sesiones nocturnas.

Las órdenes stop-loss generalmente priorizan la ejecución en lugar de la certeza del precio y durante los períodos de alta volatilidad, esta distinción se vuelve importante. Ajustar el tamaño de la posición y colocar topes con referencia al movimiento típico del precio puede ser más efectivo que simplemente apretar los topes en condiciones inestables.

¿Cómo administro la división nocturna en el ASX?

Australia comercia mientras Estados Unidos duerme, y viceversa. Esta diferencia de zona horaria es, lamentablemente, una de las razones por las que los comerciantes australianos buscan con frecuencia el riesgo de brecha nocturna. Si los mercados estadounidenses caen bruscamente, el ASX podría abrir a la baja a la mañana siguiente, sin oportunidad de salir entre el cierre y el abierto.

Los ejemplos de enfoques de gestión de riesgos que los comerciantes del mercado pueden utilizar incluyen

-Cobertura de índices mediante futuros ASX 200 o CFD*. -Cobertura parcial durante eventos de alto riesgo. -Reducir la exposición antes de los principales anuncios de macro.

La cobertura puede compensar parte de un movimiento, pero introduce un riesgo de base, ya que las acciones individuales pueden no moverse en línea con el índice más amplio.

No existe una protección perfecta, solo compensaciones entre costo, complejidad y reducción de riesgos.

*Los CFDs son instrumentos complejos y conllevan un alto riesgo de perder dinero debido al apalancamiento.

¿Cuáles son los riesgos clave de los ETF apalancados o inversos en mercados volátiles?

Los ETF apalancados e inversos a menudo se buscan durante períodos de mayor volatilidad.

Si bien estos productos generalmente se restablecen diariamente, su objetivo es ofrecer un múltiplo del rendimiento diario del índice, no su retorno a largo plazo. En un mercado volátil, lateral, la composición diaria puede erosionar el valor aunque el índice termine cerca de su nivel inicial.

Crecimiento de ETF apalancado (2011-2025) | Fuente: Investing.com

Esto ocurre porque las ganancias y pérdidas se combinan asimétricamente. Una caída del 10 por ciento requiere una ganancia de más del 10 por ciento para recuperarse. Cuando ese efecto se multiplica diariamente, los resultados pueden divergir materialmente del índice subyacente a lo largo del tiempo.

Dichos instrumentos pueden ser utilizados tácticamente por algunos participantes en el mercado. Por lo general, no están diseñados como herramientas de cobertura a largo plazo y comprender su estructura es esencial antes de utilizarlos en una estrategia.

¿Cómo se puede utilizar ATR para informar la colocación de paradas??

El rango verdadero promedio (ATR) es un indicador comúnmente utilizado para medir la volatilidad.

ATR estima cuánto se mueve típicamente un activo durante un período determinado, incluidas las brechas. En lugar de establecer una parada en un porcentaje arbitrario, algunos comerciantes hacen referencia a ATR y colocan paradas en un múltiplo, como dos o tres veces ATR, para reflejar las condiciones prevalecientes.

Cuando la volatilidad aumenta, el ATR se expande y eso puede implicar paradas más amplias o tamaños de posición más pequeños si el riesgo general va a permanecer constante. El cambio es de preguntar: “¿Hasta dónde estoy dispuesto a perder?” a preguntar: “¿Qué es una mudanza normal en las condiciones actuales?”

Consideraciones prácticas en mercados volátiles

Durante los períodos de elevada volatilidad, los comerciantes pueden considerar

Permitiendo la posibilidad de cambios de margen

Dimensionamiento de posiciones de manera conservadora si aumenta la volatilidad

Reconocer que las órdenes de stop-loss no garantizan un precio de salida específico

Revisar la exposición antes de los principales eventos económicos

Comprender la mecánica de reinicio diario de los ETF apalancados

Uso de medidas de volatilidad como ATR para informar la colocación de paradas

Mantenimiento de los búferes de efectivo adecuados

La volatilidad no recompensa por sí sola la predicción. La preparación y el conocimiento del riesgo pueden ayudar a los comerciantes a comprender los riesgos potenciales, pero los resultados siguen siendo impredecibles.

Lo que esto significa para los comerciantes australianos

Los mercados australianos enfrentan consideraciones estructurales específicas en comparación con los mercados asiáticos y estadounidenses. El riesgo de brecha durante la noche está influenciado por las horas de negociación de Estados Unidos y los índices con gran cantidad de recursos como el ASX pueden responder rápidamente a los movimientos de los precios de las materias primas y los datos de China. La exposición a la moneda, incluidos los movimientos del AUD y el dólar estadounidense (USD), puede agregar otra capa de variabilidad.

La volatilidad no es uniforme en todas las regiones. Se comporta de manera diferente dependiendo de la estructura del mercado y la profundidad de liquidez.

Preguntas frecuentes sobre volatilidad

¿Qué causa picos repentinos en la volatilidad del mercado? Las decisiones sobre tasas de interés, los datos de inflación, la evolución geopolítica, las sorpresas de ganancias y las limitaciones de liquidez son desencadenantes comunes.

¿Por qué los brokers aumentan el margen durante los mercados volátiles? Para reducir la exposición del apalancamiento y administrar el riesgo cuando las oscilaciones de precios se amplíen.

¿Pueden fallar las órdenes stop-loss durante la volatilidad? Pueden experimentar deslizamiento si los mercados se disparan más allá del nivel stop, lo que significa que la ejecución puede ocurrir a un precio peor de lo esperado. En mercados rápidos o ilíquidos, esta diferencia puede ser significativa.

¿Los ETF apalancados son adecuados para la cobertura a largo plazo? Por lo general, están estructurados para la exposición a corto plazo debido a los reajustes diarios. Si son adecuados depende de tus objetivos, situación financiera y tolerancia al riesgo.

¿Cómo se puede medir la volatilidad antes de realizar una operación? Herramientas como ATR, indicadores de volatilidad implícita y análisis de rango histórico pueden ayudar a cuantificar las condiciones prevalecientes.

Advertencia de riesgo: Los períodos de mayor volatilidad pueden conducir a rápidos movimientos de precios, cambios de margen y ejecución a precios diferentes a los esperados. Las herramientas de gestión del riesgo, como las órdenes de stop-loss y los indicadores de volatilidad, pueden ayudar a evaluar las condiciones del mercado, pero no pueden eliminar el riesgo de pérdida, especialmente cuando se utilizan productos apalancados.

Los mercados entran esta semana enfrentando una densa corrida de datos en Estados Unidos junto con una verificación de crecimiento de APAC a principios de mes. Con las acciones estadounidenses todavía relativamente elevadas y el oro manteniéndolo por encima de los 5.000 dólares, la acción de los precios a corto plazo puede ser particularmente sensible a cualquier cambio basado en datos en las tasas, la dirección del USD y el sentimiento de riesgo.

Cluster de datos de EE. UU.: Para esta semana se espera que ISM Manufacturing, ISM Services y ADP, nóminas no agrícolas (NFP) y ventas minoristas.

Pulso de crecimiento de APAC: El PMI oficial de China y el PMI de Japón, el PIB de Australia y el PMI de China Caixin proporcionan una lectura de actividad regional.

La renta variable: A pesar de una pausa al final de la semana, los principales índices estadounidenses siguen relativamente elevados en general, lo que podría aumentar la sensibilidad a las sorpresas negativas.

Oro: Ha retrocedido por encima de los 5.000 dólares, manteniendo los rendimientos reales y el sentimiento de riesgo en foco.

Geopolítica: La geopolítica de Oriente Medio sigue siendo un riesgo de volatilidad de fondo.

Estados Unidos: crecimiento y nóminas

La semana estadounidense está determinada por una secuencia apretada de señales de actividad, empleo y consumo que pueden cambiar rápidamente las expectativas de tasas a corto plazo.

Los mercados suelen tomar su primer ejemplo del sentimiento manufacturero, luego buscan servicios y nóminas privadas para una lectura más amplia de la demanda y el impulso de contratación.

El punto focal es el informe laboral, con las ventas minoristas agregando una verificación cruzada del consumidor en la misma ventana.

Esta combinación podría ser relevante para los rendimientos del Tesoro, la fijación de precios del USD y el sentimiento de renta variable, especialmente con índices aún en niveles relativamente elevados.

Fechas clave

PMI de fabricación ISM de EE. UU.: 2:00 a.m., 3 de marzo (AEDT)

Servicios ISM de EE. UU. PMI: 2:00 a.m., 5 de marzo (AEDT)

Empleo en US ADP: 12:15 a.m., 5 de marzo (AEDT)

Situación de empleo en Estados Unidos (PNF): 12:30 a.m., 7 de marzo (AEDT)

Ventas minoristas mensuales anticipadas de EE. UU. (Comercio minorista): 12:30 a.m., 7 de marzo (AEDT)

Monitorear

Hacienda rinde reacciones ante ISM y sorpresas de nómina.

Sensibilidad del USD a la refijación de precios de las tarifas.

Desempeño del índice de renta variable, particularmente dentro de la tecnología de gran capitalización.

Cambios en la política comercial, con incertidumbre arancelaria potencialmente influyente.

El calendario APAC de principios de mes proporciona una lectura rápida sobre si la actividad regional se está estabilizando o suavizando.

Los PMI (oficial y Caixin) de China ofrecen perspectivas complementarias entre las empresas vinculadas al estado y del sector privado, mientras que el PMI de Japón puede alimentar directamente el sentimiento del JPY a través de las expectativas de crecimiento.

El PIB de Australia agrega un control macro más amplio que puede influir en los precios locales del rendimiento y la dirección del AUD. En conjunto, este grupo establece la pauta para el apetito de riesgo regional y podría desemparse en materias primas y metales básicos.

Fechas clave

PMI de Japón: 11:30 a.m., 2 de marzo (AEDT)

Australia PIB: 11:30 a.m., 4 de marzo (AEDT)

PMI oficial de China: 12:30 p.m., 4 de marzo (AEDT)

China Caixin PMI: 12:45 p.m., 4 de marzo (AEDT)

Monitorear

AUD y sensibilidad al rendimiento local en torno al PIB.

Respuesta del JPY a los datos del PMI.

Reacciones regionales de equidad y materias primas a las tendencias de la actividad china.

Sensibilidad al oro y a los activos cruzados

Con el oro mantenIéndose por encima del nivel de US$5,000, podría ser altamente reactivo a los cambios en los rendimientos reales, la dirección del USD y un apetito de riesgo más amplio.

Las sorpresas macro que mueven las tasas de front-end pueden traducirse rápidamente en volatilidad del oro, mientras que los desarrollos geopolíticos que influyen en las expectativas de petróleo e inflación también podrían amplificar los movimientos.

En la práctica, el oro puede actuar como un barómetro en tiempo real de cómo los mercados están digiriendo el crecimiento, la inflación y la incertidumbre política a lo largo de la semana.

Monitorear

Movimientos de rendimiento real en Estados Unidos.

Dirección del USD.

Volatilidad de la renta variable y flujos de refugio seguro.

La volatilidad no discrimina. Pero puede castigar a los no preparados.

Detiene ser golpeado en movimientos que se invierten en cuestión de minutos. Las primas en opciones de fecha corta están subiendo. Y el yen ya no se comportaba como el seto confiable que alguna vez fue.

Para los comerciantes de toda Asia, navegar por este entorno significa hacer preguntas más difíciles sobre el riesgo, el tiempo y las suposiciones incorporadas en estrategias creadas para mercados más tranquilos.

1. ¿Cómo puedo operar con CFDs VIX durante un choque geopolítico?

El Índice de Volatilidad CBOE (VIX) mide la expectativa del mercado de volatilidad implícita a 30 días en el S&P 500. A menudo se le llama el “indicador del miedo”. Durante los choques geopolíticos como las actuales escaladas de Irán, los anuncios de sanciones y las acciones sorpresa de los bancos centrales, el VIX puede repuntar bruscamente y rápidamente.

¿Qué hace que los CFDs de VIX sean diferentes en un shock?

VIX en sí no es comercializable directamente. Los CFD de VIX suelen tener un precio de los futuros de VIX, lo que significa que tienen un arrastre de contango en condiciones normales.

Durante un choque geopolítico, varias cosas pueden suceder a la vez

El Spot VIX puede repuntar inmediatamente mientras que los futuros a corto plazo se quedan rezagados, creando una desconexión.

Los diferenciales de los CFDs de VIX pueden ampliarse significativamente a medida que disminuye la liquidez.

Los requerimientos de margen pueden cambiar intradiamente a medida que se ajustan los modelos de riesgo de los brókers.

VIX tiende a la reversión promedio después de los picos, por lo que el tiempo y la duración son críticos.

Lo que esto significa para los comerciantes de horas asiáticas

Las horas del mercado asiático significan que muchos eventos geopolíticos pueden romperse mientras los comerciantes locales están activos o apenas comienzan su sesión.

Una conmoción que golpea durante las horas de Tokio ya podría estar cotizada en futuros de VIX antes de la apertura de Sydney.

Algunos operadores utilizan las posiciones VIX CFD como una cobertura a corto plazo contra las carteras de acciones en lugar de una operación direccional. Otros negocian la reversión (el retroceso hacia promedios históricos una vez que el pico inicial se desvanece). Ambos enfoques conllevan riesgos distintos, y ninguno garantiza un resultado específico.

Índice de volatilidad (VIX) durante la escalada del conflicto del 1 de marzo en Irán | TradingView

2. ¿Por qué mis primas de opciones 0DTE son tan caras en este momento?

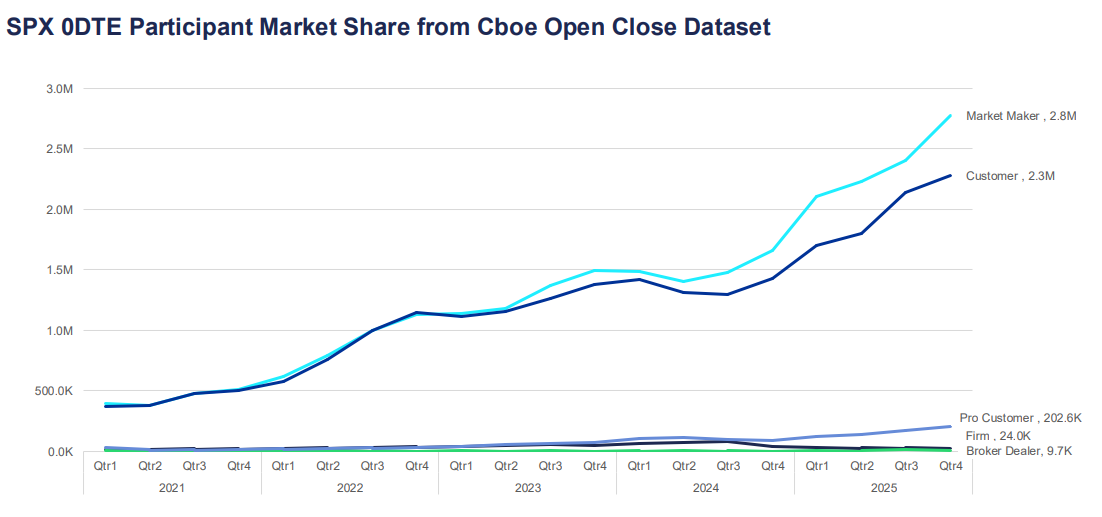

Las opciones de cero días hasta el vencimiento (0DTE) expiran el mismo día en que se negocian. Se han convertido en uno de los segmentos de más rápido crecimiento del mercado de opciones, representando ahora más del 57% del volumen diario de opciones del S&P 500 según datos de mercados globales de Cboe.

Para los participantes con sede en Asia que acceden a los mercados de opciones de Estados Unidos, las primas elevadas durante períodos volátiles pueden sentirse como un mal precio, pero por lo general reflejan factores estructurales de precios.

¿Por qué las primas se repuntan?

El precio de las opciones está impulsado por el valor intrínseco y el valor de tiempo. Para las opciones 0DTE, casi no queda valor de tiempo, lo que podría sugerir que deberían ser baratas pero el componente implícito de volatilidad compensa eso.

Cuando aumenta la incertidumbre, los vendedores pueden exigir una mayor compensación por el riesgo de movimientos intradía brusca.

Esto puede reflejarse en

Insumos de mayor volatilidad implícita.

Mayor margen de puda-tarea.

Ajustes más rápidos en cobertura delta y gamma.

En entornos de VIX más alto, los flujos de cobertura pueden contribuir a los bucles de retroalimentación a corto plazo en el índice subyacente. Esto puede amplificar las oscilaciones de precios, particularmente en torno a niveles clave.

Lo que esto significa para los comerciantes de horas asiáticas

Muchos contratos de opciones 0DTE ven sus flujos de precios y cobertura más activos durante las horas de negociación de EE. UU. Ingresar posiciones durante la sesión asiática puede significar enfrentar precios obsoletos o diferenciales más amplios.

Si está viendo primas costosas, puede reflejar que el mercado esté valorando con precisión el riesgo de una mudanza grande el mismo día. Si vale la pena pagar esa prima depende de su visión del rango intradiario probable y su tolerancia al riesgo, no solo de la cifra absoluta en dólares.

3. ¿Cómo ajusto mi bot de trading algorítmico para un entorno con alto nivel de VIX?

Muchos sistemas de comercio algorítmico se basan en parámetros calibrados durante regímenes de baja volatilidad. Cuando VIX alcanza picos, esos parámetros pueden quedar obsoletos rápidamente.

El problema del desajuste del régimen

La mayoría de los algoritmos comerciales utilizan datos históricos para establecer tamaños de posición, distancias de parada y umbrales de entrada. Esos datos reflejan las condiciones durante las cuales se probó el sistema. Si VIX pasa de 15 a 35, es posible que las suposiciones estadísticas que sustentan esas configuraciones ya no se mantengan.

Los modos de falla comunes en entornos con alto nivel de VIX incluyen

Se detiene repetidamente provocada por el ruido antes de que se produzca el movimiento direccional previsto.

Dimensionamiento de posiciones basado en el riesgo fijo en dólares, que se vuelve relativamente pequeño en comparación con los rangos intradiarios reales.

Supuestos de correlación entre activos desglosando.

Deslizamiento en la ejecución que erosiona el borde.

Enfoques que algunos comerciantes algorítmicos consideran

En lugar de ejecutar un único conjunto fijo de parámetros, algunos sistemas incorporan un filtro de régimen de volatilidad. Esta es una verificación en tiempo real en VIX o ATR que activa un interruptor a diferentes configuraciones cuando cambian las condiciones.

Ajustes de enfoque que algunos operadores revisan en entornos con alto nivel de VIX

Ampliar las distancias de parada proporcionalmente al ATR para reducir las salidas impulsadas por ruido.

Reducir el tamaño de la posición para mantener el riesgo constante en dólares en relación con rangos esperados más amplios.

Agregue un umbral VIX por encima del cual el sistema hace una pausa o se mueve al modo de comercio en papel.

Reducir el número de posiciones simultáneas, ya que las correlaciones tienden a aumentar durante el estrés del mercado.

Ningún ajuste elimina el riesgo. El backtesting de nuevos parámetros en períodos históricos de alto VIX puede proporcionar alguna indicación del probable desempeño, aunque las condiciones pasadas no son una guía confiable para los resultados futuros.

4. ¿Sigue siendo el yen japonés (JPY) un comercio seguro confiable?

Durante los períodos de aversión al riesgo global, el capital históricamente ha fluido hacia el JPY a medida que los inversores se desenrollan en las operaciones de carry y buscan tenencias de menor volatilidad. No obstante, la confiabilidad de esta dinámica se ha vuelto más condicional.

¿Por qué el yen se ha movido históricamente como un refugio seguro?

Las tasas de interés históricamente bajas de Japón hicieron del JPY la moneda de financiamiento preferida para las operaciones de carry y cuando llega el sentimiento de riesgo, esas operaciones se desenrollan rápidamente, creando demanda de yen.

Además, la gran posición neta de activos extranjeros de Japón significa que los inversores japoneses tienden a repatriar capital durante las crisis, apoyando aún más al JPY.

Lo que ha cambiado

El alejamiento del Banco de Japón de la política monetaria ultra flexible en los últimos años ha complicado la dinámica tradicional de refugio seguro.

A medida que aumentan las tasas de interés japonesas:

La escala de posicionamiento de carry trade puede cambiar.

El USD/JPY puede volverse más sensible a los diferenciales de las tasas de interés.

La comunicación del BoJ y los datos de inflación interna pueden influir en el JPY independientemente del apetito de riesgo global.

El yen aún puede comportarse como un refugio seguro, particularmente durante las fuertes vendas de acciones. Pero puede responder de manera más lenta o inconsistente en comparación con ciclos anteriores cuando la divergencia política entre Japón y el resto del mundo era más extrema.

Qué ver

Para los comerciantes que monitorean el JPY como una señal de refugio seguro, las fechas de reunión del BoJ, las publicaciones del IPC japonés y los datos de spread de tasas entre Estados Unidos y Japón en tiempo real se han convertido en insumos más relevantes que hace unos años.

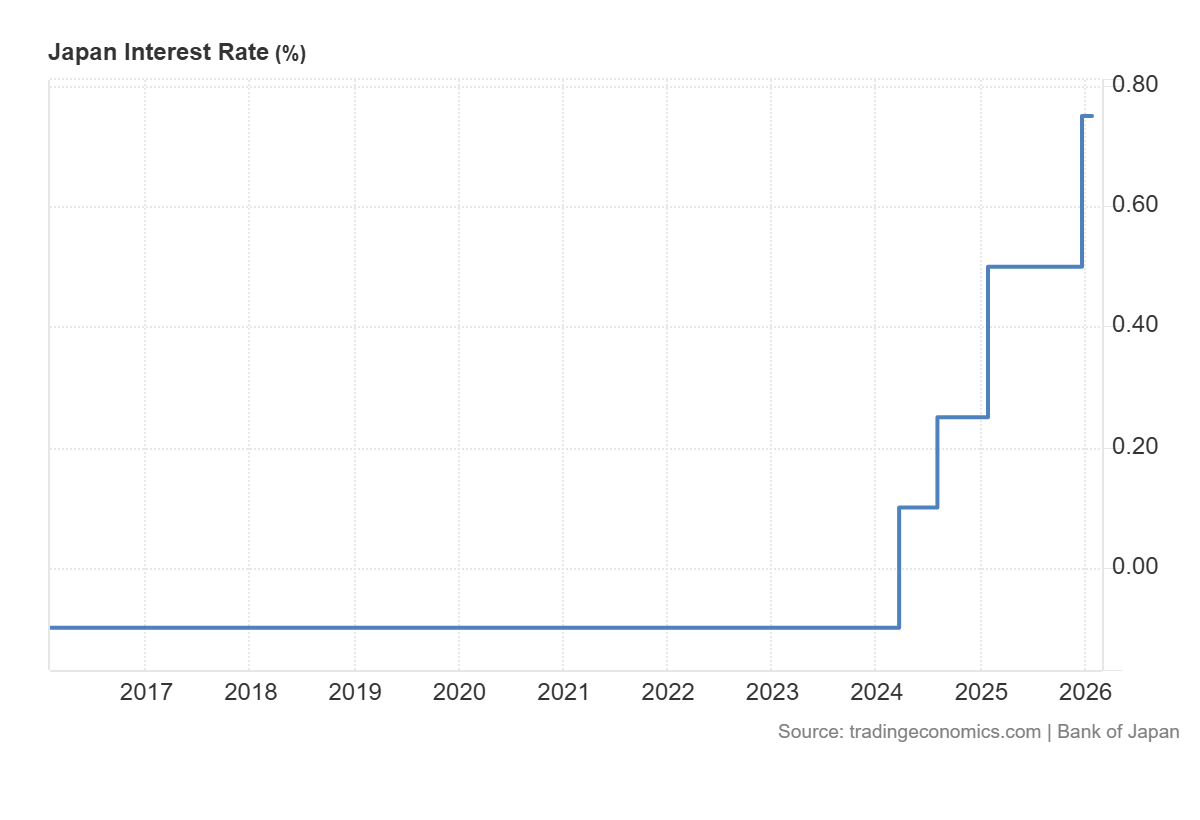

Las tasas de Japón subieron a lo positivo en 2024 después de años en -0.1% | Economía comercial

5. ¿Cómo evito los 'azotes' en los CFDs sobre energía?

Whipsawing describe la experiencia de ingresar a una operación en una dirección, ser detenido a medida que el precio se invierte, luego ver el precio retroceder en la dirección original.

Los CFDs sobre energía, particularmente el petróleo crudo, son especialmente propensos a esto en los mercados volátiles. Y para los comerciantes en Asia, la combinación de poca liquidez durante el horario local y sensibilidad a los titulares geopolíticos puede hacer que esto sea particularmente desafiante.

¿Por qué los CFDs de energía whipsaw?

El petróleo crudo es sensible a una amplia gama de impulsores generales: decisiones de producción de la OPEP+, datos de inventario de Estados Unidos, interrupciones geopolíticas del suministro y movimientos de divisas.

En entornos de alta volatilidad, el mercado puede reaccionar fuertemente a cada titular antes de dar marcha atrás cuando llegue el siguiente.

Los picos de precios en un titular, las paradas se activan en posiciones cortas.

Los comerciantes vuelven a entrar largo tiempo, esperando continuación.

Un segundo titular o toma de ganancias revierte la jugada.

Se golpean paradas largas. El ciclo se repite.

Enfoques que los comerciantes pueden considerar para administrar el riesgo de Whipsaw

Algunos comerciantes optan por cambiar sus controles de riesgo en condiciones volátiles (por ejemplo, revisar la colocación de stop en relación con las medidas de volatilidad). Sin embargo, estos pueden aumentar las pérdidas; los riesgos de ejecución y deslizamiento pueden aumentar considerablemente en los mercados rápidos.

Otros enfoques que algunos comerciantes revisan:

Evite operar con CFD de petróleo crudo en los 30 minutos antes y después de las principales publicaciones de datos programadas.

Utilice un gráfico de plazos más largo para identificar la tendencia predominante antes de entrar en un período de tiempo más corto, lo que reduce la posibilidad de operar contra flujos institucionales más grandes.

Escale a posiciones en etapas en lugar de comprometer el tamaño completo en la entrada inicial.

Monitoree el interés abierto y el volumen para distinguir entre movimientos con participación genuina y faltas de baja liquidez.

Los latiguillos no se pueden eliminar por completo en los mercados energéticos volátiles. El objetivo de la administración de riesgos en estas condiciones no es predecir qué movimientos se mantendrán, sino asegurar que las pérdidas en movimientos falsos sean menores que las ganancias cuando sigue un movimiento direccional genuino.

Consideraciones prácticas para los mercados asiáticos volátiles

Los mercados asiáticos tienen características estructurales que interactúan con la volatilidad de manera diferente a los mercados estadounidenses o europeos:

Una liquidez más delgada durante el horario local puede exagerar los movimientos en volúmenes delgados, particularmente en CFDs de energía y FX.

Los eventos en China, incluidas las publicaciones del PMI, los datos comerciales y las señales de política del PBOC, pueden mover los índices regionales.

Las decisiones políticas del BoJ se han convertido en un impulsor más activo de la volatilidad del JPY y el Nikkei en los últimos años.

Las brechas de la noche a la mañana de los movimientos de la sesión de Estados Unidos son un riesgo estructural persistente para los operadores que no pueden monitorear las posiciones durante todo el día.

Los requerimientos de margen de los productos apalancados pueden cambiar a corto plazo durante los períodos de alto VIX.

Preguntas frecuentes sobre la volatilidad en los mercados asiáticos

¿Qué significa una lectura alta de VIX para los índices bursátiles asiáticos?

VIX mide la volatilidad esperada en el S&P 500, pero las lecturas elevadas suelen reflejar la aversión global al riesgo que fluye a través de los mercados. Los índices asiáticos como el Nikkei 225, Hang Seng y ASX 200 a menudo pueden ver una mayor volatilidad y correlación negativa con fuertes picos de VIX.

¿Se pueden negociar las opciones de 0DTE durante el horario asiático?

El acceso depende de la plataforma y del instrumento específico. Las opciones del índice de acciones 0DTE de EE. UU. tienen un precio más activo durante las horas de negociación de Estados Unidos. Los comerciantes asiáticos pueden enfrentar diferenciales más amplios y precios menos representativos fuera de esas horas.

¿Las estrategias algorítmicas de trading son inherentemente más riesgosas en condiciones de alta volatilidad?

Las estrategias calibradas durante períodos de baja volatilidad pueden funcionar de manera diferente en entornos de alto VIX. La revisión periódica de los parámetros frente a las condiciones actuales del mercado es prudente para cualquier enfoque sistemático.

¿El comercio de refugio seguro del JPY ha cambiado permanentemente?

La normalización de las políticas del Banco de Japón ha introducido nuevas dinámicas, pero el JPY ha seguido fortaleciéndose durante algunos episodios de riesgo. Puede estar más condicionado a la naturaleza del choque y a la postura concurrente del BoJ.

¿Cuál es la mejor manera de establecer paradas en los CFDs de energía en condiciones de alta volatilidad?

No existe un método universalmente mejor. Muchos comerciantes hacen referencia a ATR para calibrar las distancias de parada a las condiciones prevalecientes en lugar de usar niveles fijos. Esto no garantiza la salida al precio deseado y no elimina el riesgo de whipsaw.

La volatilidad tiene una forma de aparecer sin invitación.

Un día el ASX está a la deriva silenciosamente... y al siguiente, los requisitos de margen aumentan, las paradas no llenan donde se esperaba, y las carteras se abren con incómodas brechas de la noche a la mañana.

Si has estado buscando respuestas, no estás solo. Algunas de las preguntas más buscadas sobre la volatilidad entre los comerciantes australianos se relacionan con llamadas de margen, deslizamiento, brechas nocturnas, fondos cotizados en bolsa apalancados (ETF) y herramientas como promedio true range (ATR).

Esto es lo que está pasando.

Por qué esto es importante ahora

Los mercados mundiales se han vuelto más sensibles a las tasas de interés, los datos de inflación, la geopolítica y los flujos impulsados por la tecnología. Cuando la liquidez se hace más baja y la incertidumbre sube, las oscilaciones de precios se ensanchan. Eso es volatilidad.

Y la volatilidad no solo afecta la dirección de los precios, sino que cambia la forma en que se ejecutan las operaciones, cuánto capital se requiere y cómo se comporta el riesgo debajo de la superficie.

Traducción: La volatilidad no se trata solo de movimientos más grandes, más bien, se trata de movimientos más rápidos y liquidez más delgada, ahí es cuando más importa la mecánica del trading.

¿Por qué mi broker aumentó los requerimientos de margen?

Una de las preguntas más buscadas sobre la volatilidad es por qué los requerimientos de margen aumentan sin previo aviso.

Cuando los mercados se vuelven inestables, los corredores pueden aumentar los requerimientos de margen en los contratos por diferencia (CFDs) y otros productos apalancados. Las oscilaciones de precios mayores pueden aumentar el riesgo de que las cuentas pasen a acciones negativas, por lo que aumentar los requerimientos de margen reduce el apalancamiento disponible y puede ayudar a administrar la exposición durante condiciones extremas.

Lo que esto puede significar en la práctica

-Una llamada de margen puede ocurrir incluso si el precio no se ha movido significativamente. -El apalancamiento efectivo puede caer rápidamente. -Es posible que sea necesario reducir las posiciones con poca antelación.

Los ajustes de margen suelen ser una respuesta al riesgo cambiante del mercado, no una decisión aleatoria. En mercados altamente volátiles, es prudente asumir que los ajustes de margen pueden cambiar rápidamente, por lo tanto, muchos operadores optan por revisar los tamaños de posición y los buffers disponibles a la luz de ese riesgo.

¿Qué es el deslizamiento y por qué mi stop no llenó a mi precio?

Otro tema que se busca con frecuencia es el deslizamiento.

El deslizamiento puede ocurrir cuando una orden de stop se activa y se ejecuta al siguiente precio disponible, el resultado puede depender del tipo de orden, liquidez del mercado y brechas. En los mercados tranquilos, la diferencia puede ser pequeña mientras que en los mercados rápidos, los precios pueden dispararse más allá del nivel de parada.

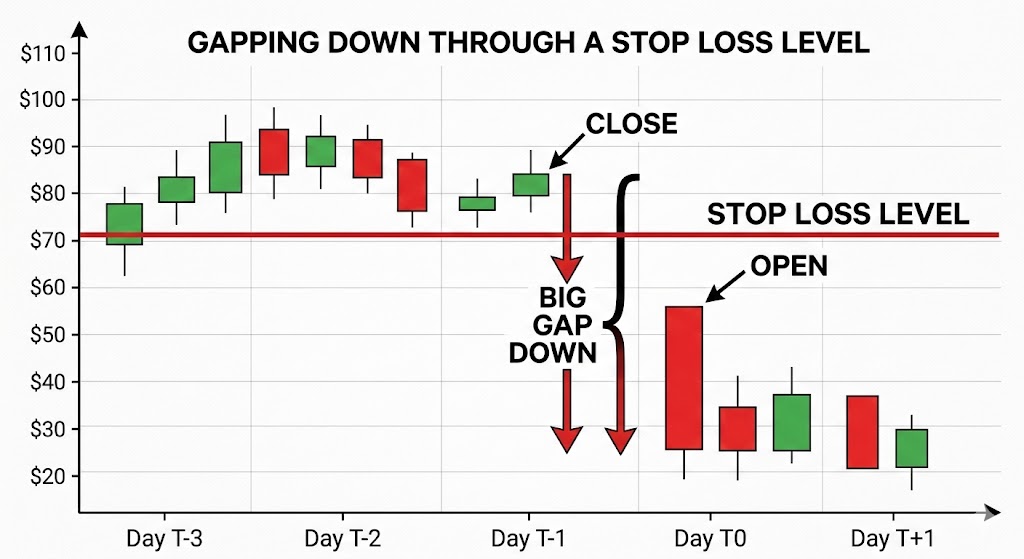

Ilustración de la brecha de precios a través del nivel stop-loss | GO Markets

Los controladores comunes incluyen

-Principales liberaciones económicas o de ganancias. -Liquidez delgada. -Niveles de parada abarrotados. -Sesiones nocturnas.

Las órdenes stop-loss generalmente priorizan la ejecución en lugar de la certeza del precio y durante los períodos de alta volatilidad, esta distinción se vuelve importante. Ajustar el tamaño de la posición y colocar topes con referencia al movimiento típico del precio puede ser más efectivo que simplemente apretar los topes en condiciones inestables.

¿Cómo administro la división nocturna en el ASX?

Australia comercia mientras Estados Unidos duerme, y viceversa. Esta diferencia de zona horaria es, lamentablemente, una de las razones por las que los comerciantes australianos buscan con frecuencia el riesgo de brecha nocturna. Si los mercados estadounidenses caen bruscamente, el ASX podría abrir a la baja a la mañana siguiente, sin oportunidad de salir entre el cierre y el abierto.

Los ejemplos de enfoques de gestión de riesgos que los comerciantes del mercado pueden utilizar incluyen

-Cobertura de índices mediante futuros ASX 200 o CFD*. -Cobertura parcial durante eventos de alto riesgo. -Reducir la exposición antes de los principales anuncios de macro.

La cobertura puede compensar parte de un movimiento, pero introduce un riesgo de base, ya que las acciones individuales pueden no moverse en línea con el índice más amplio.

No existe una protección perfecta, solo compensaciones entre costo, complejidad y reducción de riesgos.

*Los CFDs son instrumentos complejos y conllevan un alto riesgo de perder dinero debido al apalancamiento.

¿Cuáles son los riesgos clave de los ETF apalancados o inversos en mercados volátiles?

Los ETF apalancados e inversos a menudo se buscan durante períodos de mayor volatilidad.

Si bien estos productos generalmente se restablecen diariamente, su objetivo es ofrecer un múltiplo del rendimiento diario del índice, no su retorno a largo plazo. En un mercado volátil, lateral, la composición diaria puede erosionar el valor aunque el índice termine cerca de su nivel inicial.

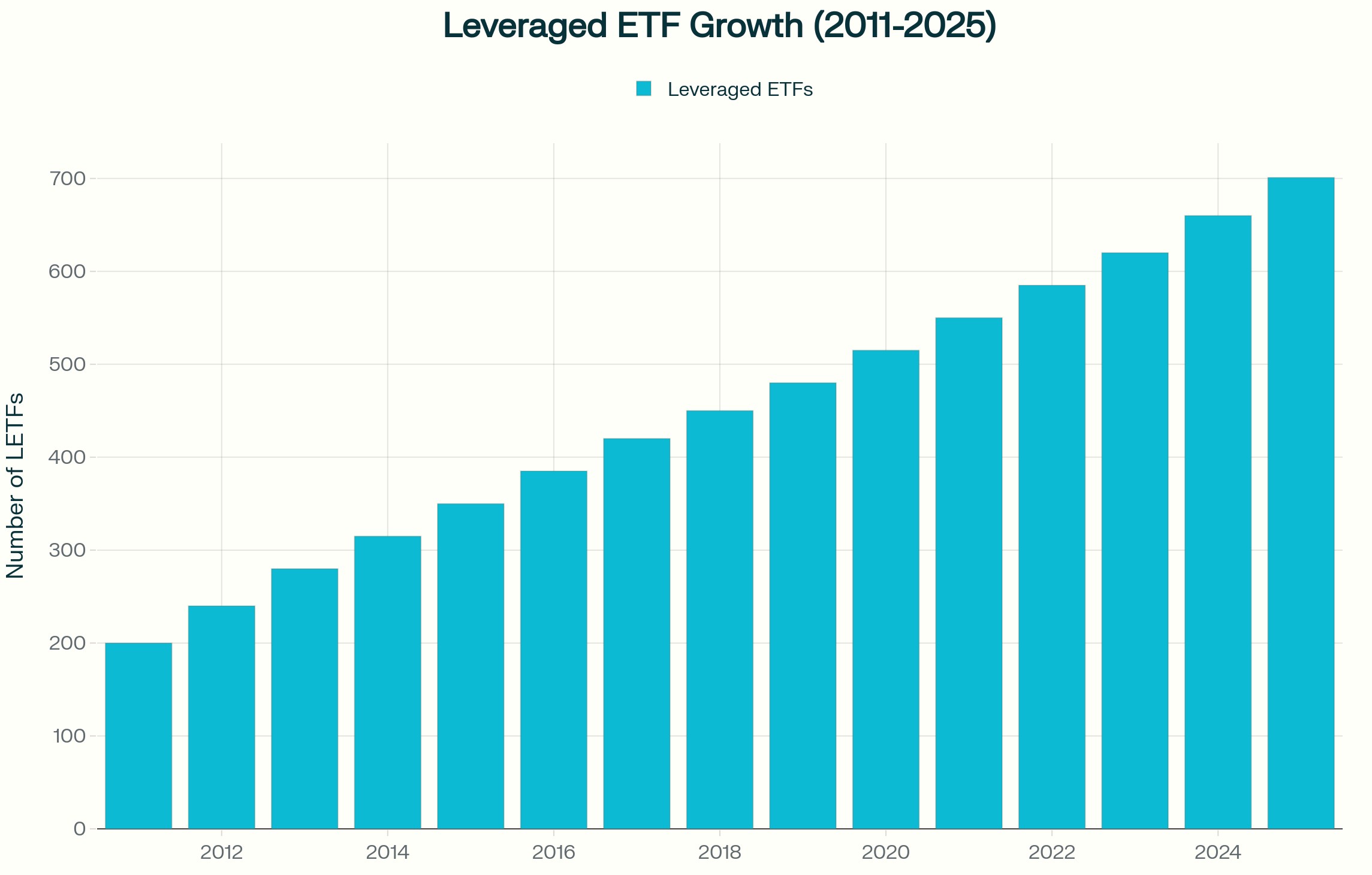

Crecimiento de ETF apalancado (2011-2025) | Fuente: Investing.com

Esto ocurre porque las ganancias y pérdidas se combinan asimétricamente. Una caída del 10 por ciento requiere una ganancia de más del 10 por ciento para recuperarse. Cuando ese efecto se multiplica diariamente, los resultados pueden divergir materialmente del índice subyacente a lo largo del tiempo.

Dichos instrumentos pueden ser utilizados tácticamente por algunos participantes en el mercado. Por lo general, no están diseñados como herramientas de cobertura a largo plazo y comprender su estructura es esencial antes de utilizarlos en una estrategia.

¿Cómo se puede utilizar ATR para informar la colocación de paradas??

El rango verdadero promedio (ATR) es un indicador comúnmente utilizado para medir la volatilidad.

ATR estima cuánto se mueve típicamente un activo durante un período determinado, incluidas las brechas. En lugar de establecer una parada en un porcentaje arbitrario, algunos comerciantes hacen referencia a ATR y colocan paradas en un múltiplo, como dos o tres veces ATR, para reflejar las condiciones prevalecientes.

Cuando la volatilidad aumenta, el ATR se expande y eso puede implicar paradas más amplias o tamaños de posición más pequeños si el riesgo general va a permanecer constante. El cambio es de preguntar: “¿Hasta dónde estoy dispuesto a perder?” a preguntar: “¿Qué es una mudanza normal en las condiciones actuales?”

Consideraciones prácticas en mercados volátiles

Durante los períodos de elevada volatilidad, los comerciantes pueden considerar

Permitiendo la posibilidad de cambios de margen

Dimensionamiento de posiciones de manera conservadora si aumenta la volatilidad

Reconocer que las órdenes de stop-loss no garantizan un precio de salida específico

Revisar la exposición antes de los principales eventos económicos

Comprender la mecánica de reinicio diario de los ETF apalancados

Uso de medidas de volatilidad como ATR para informar la colocación de paradas

Mantenimiento de los búferes de efectivo adecuados

La volatilidad no recompensa por sí sola la predicción. La preparación y el conocimiento del riesgo pueden ayudar a los comerciantes a comprender los riesgos potenciales, pero los resultados siguen siendo impredecibles.

Lo que esto significa para los comerciantes australianos

Los mercados australianos enfrentan consideraciones estructurales específicas en comparación con los mercados asiáticos y estadounidenses. El riesgo de brecha durante la noche está influenciado por las horas de negociación de Estados Unidos y los índices con gran cantidad de recursos como el ASX pueden responder rápidamente a los movimientos de los precios de las materias primas y los datos de China. La exposición a la moneda, incluidos los movimientos del AUD y el dólar estadounidense (USD), puede agregar otra capa de variabilidad.

La volatilidad no es uniforme en todas las regiones. Se comporta de manera diferente dependiendo de la estructura del mercado y la profundidad de liquidez.

Preguntas frecuentes sobre volatilidad

¿Qué causa picos repentinos en la volatilidad del mercado? Las decisiones sobre tasas de interés, los datos de inflación, la evolución geopolítica, las sorpresas de ganancias y las limitaciones de liquidez son desencadenantes comunes.

¿Por qué los brokers aumentan el margen durante los mercados volátiles? Para reducir la exposición del apalancamiento y administrar el riesgo cuando las oscilaciones de precios se amplíen.

¿Pueden fallar las órdenes stop-loss durante la volatilidad? Pueden experimentar deslizamiento si los mercados se disparan más allá del nivel stop, lo que significa que la ejecución puede ocurrir a un precio peor de lo esperado. En mercados rápidos o ilíquidos, esta diferencia puede ser significativa.

¿Los ETF apalancados son adecuados para la cobertura a largo plazo? Por lo general, están estructurados para la exposición a corto plazo debido a los reajustes diarios. Si son adecuados depende de tus objetivos, situación financiera y tolerancia al riesgo.

¿Cómo se puede medir la volatilidad antes de realizar una operación? Herramientas como ATR, indicadores de volatilidad implícita y análisis de rango histórico pueden ayudar a cuantificar las condiciones prevalecientes.

Advertencia de riesgo: Los períodos de mayor volatilidad pueden conducir a rápidos movimientos de precios, cambios de margen y ejecución a precios diferentes a los esperados. Las herramientas de gestión del riesgo, como las órdenes de stop-loss y los indicadores de volatilidad, pueden ayudar a evaluar las condiciones del mercado, pero no pueden eliminar el riesgo de pérdida, especialmente cuando se utilizan productos apalancados.

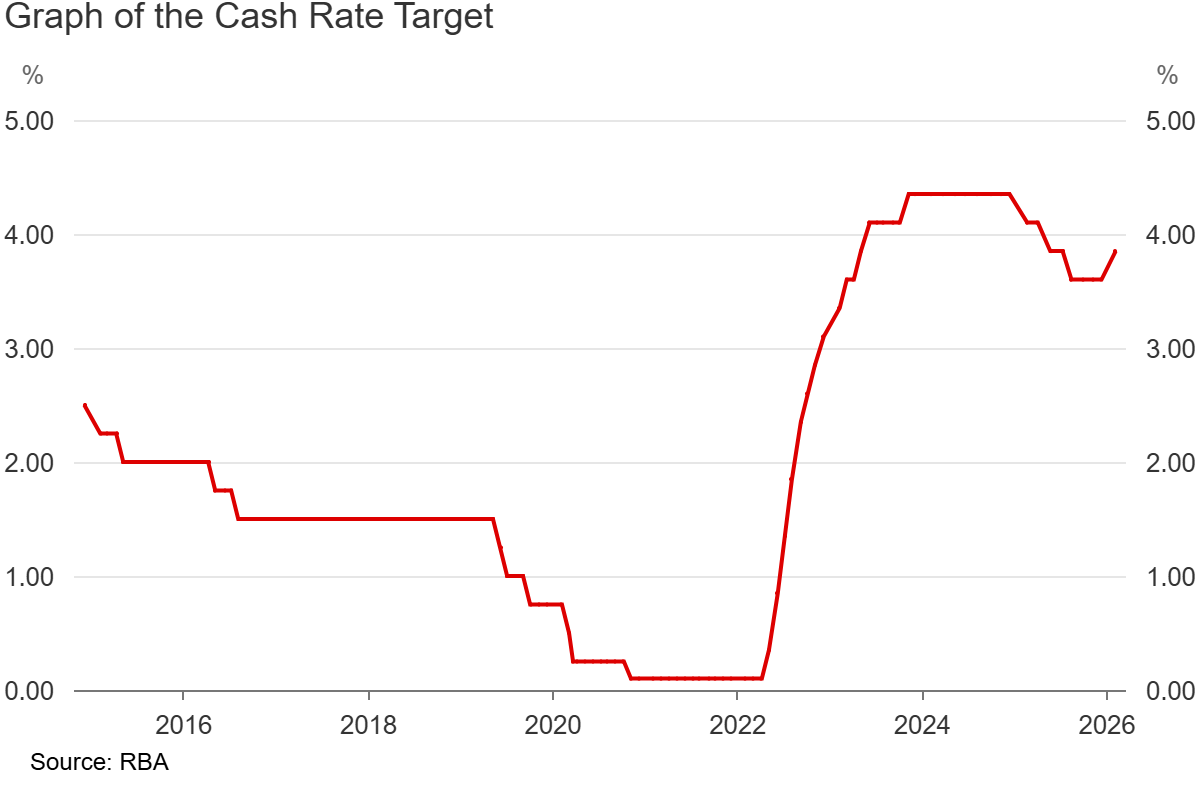

Pocas instituciones moldean la vida cotidiana australiana tan silenciosamente, o tan poderosamente, como el Banco de la Reserva de Australia (RBA).

Cada vez que renuevas una hipoteca, abres una cuenta de ahorros o ves el movimiento del dólar australiano, las decisiones del RBA están en algún lugar en segundo plano.

Pero, ¿qué sucede realmente dentro del banco, y qué impulsa las llamadas que se ondulan a través de toda la economía australiana?

Datos rápidos

La tasa de efectivo del RBA es el número más visto en las finanzas australianas.

Decisiones de tarifas son hechos por una junta directiva de nueve miembros, ocho veces al año.

El RBA apunta a una inflación de 2— 3% en promedio a lo largo del tiempo.

La tasa de efectivo de Australia alcanzó un máximo de 12 años de 4.35% en noviembre de 2023.

¿Qué es el RBA?

El RBA es el banco central de Australia. A diferencia de los bancos comerciales que prestan a particulares y empresas, el RBA presta a instituciones financieras, emite la moneda de la nación y actúa como banquero del gobierno.

También desempeña un papel en la supervisión de la estabilidad del sistema financiero en general. Puede intervenir durante períodos de estrés económico para garantizar que el crédito siga fluyendo.

Para el australiano promedio, el RBA es más visible a través de su influencia en las tasas de interés. Al establecer un objetivo para la tasa de efectivo, da forma al endeudamiento y al ahorro de costos en toda la economía.

Esta influencia puede filtrarse a través de las tasas hipotecarias, los préstamos comerciales y el precio del dólar australiano.

¿Cómo funciona la tasa de efectivo?

El tipo de efectivo es la tasa de interés que cobra el RBA sobre los préstamos a la noche entre bancos. Los bancos constantemente se prestan dinero entre sí para administrar sus necesidades diarias de efectivo, y el RBA establece la palabra sobre cuáles son esos costos de endeudamiento.

Cuando el RBA eleva la tasa de efectivo, los bancos tienden a pasar ese costo a los prestatarios; cuando recorta, los intereses sobre los pagos tienden a caer.

Este efecto colateral es la razón por la que la tasa de efectivo es una herramienta tan poderosa. Los bancos ponen precios a sus productos con respecto a la tasa de efectivo, por lo que un movimiento del 0.25% del RBA generalmente fluye a tasas hipotecarias variables en cuestión de semanas.

Efectos de los movimientos de la tasa de efectivo del RBA

Una gran parte de las hipotecas australianas están a tipos variables, por lo que cualquier cambio en la tasa de efectivo tiende a pasar a los presupuestos de los hogares más rápido que en los países donde los préstamos a tasa fija son más prominentes.

¿Cómo toma decisiones el RBA?

El directorio del RBA se reúne ocho veces al año para fijar la política monetaria, con fechas de reunión publicadas de antemano.

El Consejo cuenta con nueve miembros: el Gobernador, el Vicegobernador, el Secretario de Hacienda, y seis miembros externos designados por el Tesorero por períodos de cinco años. Las decisiones se toman por consenso en la medida de lo posible, con el Gobernador realizando un voto decisivo si es necesario.

Estos miembros toman decisiones con la intención de mantener la estabilidad de precios y apoyar el pleno empleo, con la prosperidad económica y el bienestar del pueblo australiano como objetivo general.

La estabilidad de precios generalmente significa mantener la inflación dentro de una banda objetivo de 2— 3% en promedio a lo largo del tiempo. El encuadre “en promedio a lo largo del tiempo” es deliberado; el RBA no entra en pánico si la inflación se desvía brevemente fuera de la banda, pero una desviación sostenida en cualquier dirección puede llevar a la Junta a considerar una respuesta política.

El pleno empleo se ve en términos de la Tasa de Inflación No Acelerada del Desempleo (NAIRU), la tasa de desempleo más baja que puede sostener la economía sin generar presión salarial inflacionaria. Las estimaciones varían, pero el RBA históricamente ha colocado esto en torno al 4— 4.5%.

La tensión entre estos dos objetivos define la mayoría de las decisiones del RBA. Un mercado laboral fuerte es una buena noticia para los trabajadores, pero puede empujar los salarios (y por lo tanto la inflación) al alza. Por otro lado, el enfriamiento de la inflación a menudo requiere aceptar algún aumento en el desempleo.

En el período previo a cada reunión, el personal del RBA prepara un extenso material informativo que cubre todos los indicadores económicos importantes. La Junta debate las pruebas a lo largo de dos días antes de llegar a una decisión. El resultado se da a conocer públicamente a las 2:30pm AEDT del día de la reunión, seguido de una declaración detallada y una conferencia de prensa por parte del Gobernador.

Insumos clave para cada decisión

El ciclo de tasas reciente del RBA

El ciclo de tasas actual es uno de los más agresivos en la historia moderna del RBA. Después de mantener la tasa de caja en un mínimo histórico de 0.10% a través de la pandemia de COVID, el RBA comenzó a subir en mayo de 2022 y elevó las tasas trece veces antes de hacer una pausa en 4.35% en noviembre de 2023.

Un prestatario con una hipoteca de tasa variable de $750,000 vio aumentar sus pagos mensuales en aproximadamente $1,500 a $1,800 entre mayo de 2022 y finales de 2023, una importante disminución de los presupuestos de los hogares que alimentó directamente a la desaceleración del consumidor que el RBA estaba tratando de diseñar.

A lo largo de 2025, el RBA volvió a bajar periódicamente la tasa, situándose ahora en 3.75% después de una reciente alza en febrero de 2026.

Objetivo de tasa de efectivo del RBA 2015-2026 | RBA

¿Qué deben observar los comerciantes?

IPC Mensual

El IPC mensual generalmente se considera el punto de datos individual más importante para los observadores de RBA. Si el dato arroja una impresión de “IPC medio trimestral recortado” por encima del 3%, puede agudizar las expectativas de una subida o retrasar los recortes (particularmente si sorprende al alza). La “media recortada” es la medida preferida del RBA, ya que tiende a reducir el ruido de los datos debido a la volatilidad.

Datos sobre la fuerza de trabajo

Los datos de la fuerza laboral incluyen cifras sobre las tasas de desempleo y subempleo, y el crecimiento salarial. El RBA vigila de cerca estos números para detectar cualquier señal de que los salarios puedan estar subiendo a un ritmo inconsistente con la meta de inflación.

Discursos y comparecencias del gobernador

Entre reuniones formales, el Gobernador testifica ante el Comité de Economía de la Cámara y da discursos públicos. Estos se examinan de cerca en busca de señales de sentimiento de la junta. Los cambios simples en el lenguaje, de “paciente” a “vigilante”, por ejemplo, a menudo pueden percibirse como un cambio de tono que podría influir en la decisión de tarifas en las próximas reuniones.

Tasa neutra

La “tasa neutral” es el rango de tasa de efectivo que el RBA cree que no acelerará la economía ni la ralentizará. El actual tipo de efectivo neutral se estima en alrededor de 3.0— 3.5%, que está por debajo de la tasa real de 3.75%, una señal de que el RBA sigue frenando a la economía. A medida que la tasa se acerca a la zona neutral, puede indicar menos urgencia para que el RBA siga recortando. Sin embargo, los datos sorpresa siempre pueden cambiar esta suposición.

Bancos centrales mundiales

El RBA no opera de forma aislada. Si la Reserva Federal de Estados Unidos mantiene las tasas más altas por más tiempo, limita el margen del RBA para recortar sin debilitar el AUD e importar la inflación a través de mayores precios de importación.

Conclusión

El trabajo del RBA es mantener a la economía australiana en un nivel parejo, y la tasa de efectivo es su principal herramienta para hacerlo. Sus decisiones tocan casi todos los rincones de la vida financiera australiana, desde lo que paga en su hipoteca hasta cómo se comercia el dólar australiano.

Para los comerciantes, entender cómo piensa el RBA y qué está viendo es un gran paso para dar sentido al entorno económico australiano más amplio.