热门话题

一年一度的dota2国际邀请赛将要召开啦。Dota2国际邀请赛也俗称TI,之前已经召开了10次比赛而这一次的就是TI 11.这次举办的地址选在了新加坡,这是电竞界的最高盛事首次来到东南亚。这将是迄今为止连续四个周末的Dota 赛事,共有来自世界各地的30 支队伍参加,这也将是迄今为止最大的Dota 赛事。

Dota 2是由Valve在2013年开发和发行的多人在线战斗竞技场(MOBA)视频游戏。该游戏是远古防御( Defense of the Ancients )的续集,DOTA是暴雪娱乐的《魔兽争霸III:混沌之治》社区创建的模组。Dota 2是在两由五名玩家组成的队伍之间进行的比赛,每支队伍在地图上占领和保卫自己的独立基地。十名玩家中的每一位都独立控制一个强大的角色,称为“英雄”,他们都拥有独特的能力和不同的游戏风格。在比赛期间玩家收集经验值 以及进行物品的购买,为了可以击杀对方团队的英雄。一个团队首先摧毁了另一个团队的“古代遗迹”,这是一个位于队伍己方基地,一旦基地遗迹被摧毁,那么摧毁方就会赢得比赛。因此,在这样的规则下,就让Dota2的比赛充满着许多的不确定性,无论击杀对方英雄多少次,一旦遗迹被摧毁,还是会输掉比赛。所以,DOta2的游戏魅力应运而生,那就是有无限的可能性,有时候一个小小的失误也可能葬送掉比赛。不过就是dota2的学习周期太长和上手难度高,导致游戏新鲜血液也越来越少。在今年8月分开始出售新加坡Ti11的比赛门票,但是在短短的15秒钟,门票就被黄牛抢购一空,作为想买门票的doter,不禁也感叹,黄牛真厉害。

不过,我们今天就来讲一讲从dota2国际邀请赛购票衍生出的黄牛经济学。黄牛一词的出现,是来源于20世纪的上海,在当时,票贩子进行抢票的的时候都是跑得快,挤的厉害,人们就称其“似黄牛之群骚动”。那么这个词真正开始推广的原因是之前的春运。春运期间,无数的人返现家,那么春运票就出现了供不应求的一个情况,而且因为政策的限制,票价不可能持续上涨。在这种情况下,黄牛就看准了这个机会,提前购入大量票,然后以高价把票卖出去,以此来牟利。纵观历史,黄牛实际上一直都存在于我们的社会生活当中。各个地方的叫法不同,有叫倒爷的,有叫黄牛的。然而他们都是同一类人。随着时代的改变,黄牛的倒卖范围也在不断的增加,从之前的演唱会票,到后来的Dota2 Ti 票,新上市的电子产品,甚至医院的挂号。大部分人把黄牛归结为管制的不够完善,而实际上,其中也存在的底层的经济学逻辑,让黄牛这一职业存活了下来,甚至到这些年,存活的也越来越好。

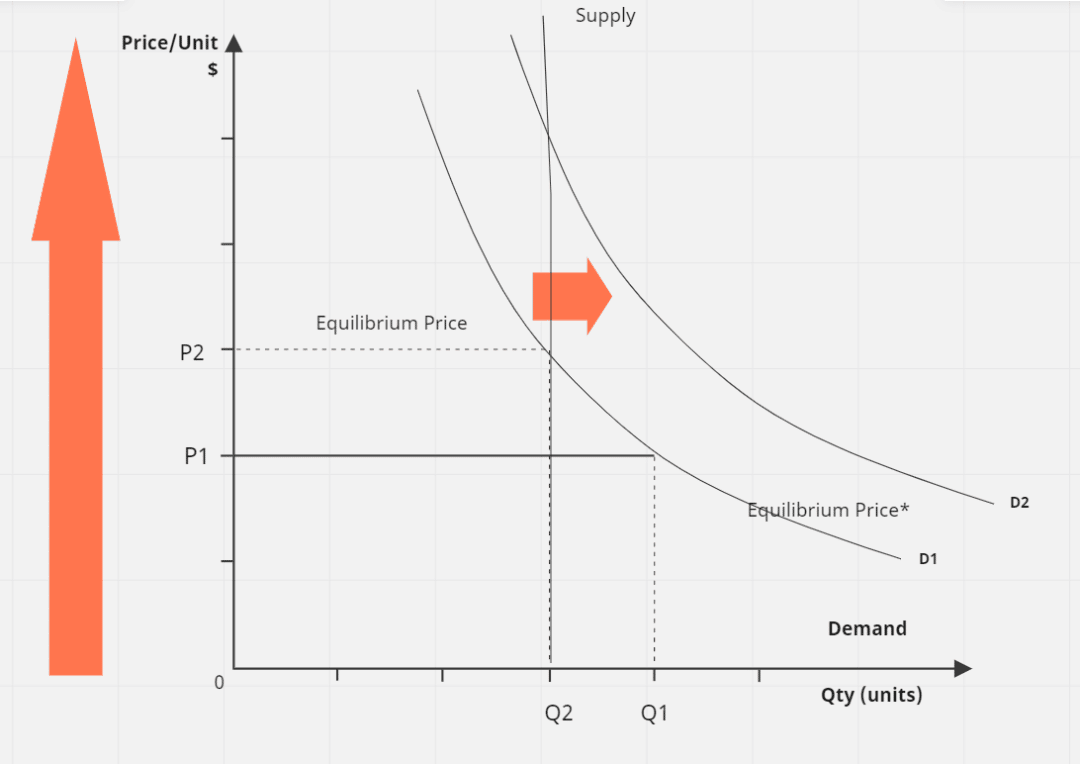

首先,最大的问题就是供不应求和价格的控制。对于这些情况,实际上就存在一个供不应求的关系。每年或者每个时间段有的供给是一个固定的数量(图中的S),但是在需求端是在逐渐上升的(D1-D2)。那么就造成供求曲线不存在任何的弹性。同时,在价格严格控制的同时,原本可以通过涨价使得需求降低的情况也不存在。这时候,黄牛的就应运而生,黄牛通过牟利,赚取差价,让票价上市(P1-P2),从而需求降低(Q1-Q2)。从某种意义上来说,黄牛“创造”了一个二级市场,然后通过自定义价格去使得供需达到一个罕见的平衡。当然,这个自定义的票价也不是随便去定义的,而是符合市场需求环境去定价。只要一天供给达不到平衡,价格继续被控制住,黄牛就会继续牟利。

以这次Ti门票为例,实际上,对于决赛的门票一定需求大于供给的,那么黄牛看准这个机会,先抢到这个票,把价格提上来,最后卖出去牟利,而黄牛也知道,决赛门票只要不是贵的离谱,近期是不会出现滞销的,因此,很多人成为的抢不到票的倒霉蛋。进而大概率只能去购买高价的黄牛票。其次,就是定价的公平性。实际上很多东西的定价对于不同人群是不同的。举个例子,抢购某个新产品,会员价格是5000,非会员价格是7000.那么这样的情况就会自然而然的产生差价,要么我就成为会员,要么就是找有会员的人买。当然,有会员的人出售的时候,大部分都不会以5000的原价出售。因为我费时费力的抢购,但是又不会以7000的非会员价出售,这时候可能6000就是一个合理价格,那么就可以达成双方都开心的局面。没需求的会员赚了1000,有需求的非会员节省了1000元。当然,这并不能改变黄牛在我们心中的地位。最主要的原因就是,黄牛打破了一个最基本的原则。公平。因为无论是我们抢票还是买东西,只要我们有足够的资金,都有权去购买想要的产品,这就是有着同样机会的公平性。就像但是黄牛通过自身的手段,使我们失去了这种机会和权力的公平性。其次就是使得供求双方的权利受损的可能性非常大。因为其使得供需双方不能直接交易,那么很容易出现就是分配不公平的现象。最简单的例子就是,黄牛价格太狠,导致演唱会门票滞销,想看演唱会的人看不到,辛辛苦苦准备的歌手等主办方努力付诸东流。然后就是,黄牛中不可避免的存在有欺诈的存在,导致供需双方利益进一步受损。免责声明:GO Markets分析师或外部发言人提供的信息基于其独立分析或个人经验。所表达的观点或交易风格仅代表其个人;并不代表GO Markets的观点或立场。联系方式:墨尔本 03 8658 0603悉尼 02 9188 0418中国地区(中文) 400 120 8537中国地区(英文) +248 4 671 903作者:Neo Yuan | GO Markets 助理分析师

The information provided is of general nature only and does not take into account your personal objectives, financial situations or needs. Before acting on any information provided, you should consider whether the information is suitable for you and your personal circumstances and if necessary, seek appropriate professional advice. All opinions, conclusions, forecasts or recommendations are reasonably held at the time of compilation but are subject to change without notice. Past performance is not an indication of future performance. Go Markets Pty Ltd, ABN 85 081 864 039, AFSL 254963 is a CFD issuer, and trading carries significant risks and is not suitable for everyone. You do not own or have any interest in the rights to the underlying assets. You should consider the appropriateness by reviewing our TMD, FSG, PDS and other CFD legal documents to ensure you understand the risks before you invest in CFDs. 免责声明:文章来自 GO Markets 分析师和参与者,基于他们的独立分析或个人经验。表达的观点、意见或交易风格仅代表作者个人,不代表 GO Markets 立场。建议,(如有),具有“普遍”性,并非基于您的个人目标、财务状况或需求。在根据建议采取行动之前,请考虑该建议(如有)对您的目标、财务状况和需求的适用程度。如果建议与购买特定金融产品有关,您应该在做出任何决定之前了解并考虑该产品的产品披露声明 (PDS) 和金融服务指南 (FSG)。

.jpg)

.jpg)

.jpg)