Expected earnings date: Wednesday, 28 January 2026 (US, after market close) / early Thursday, 29 January 2026 (AEDT)

Key areas in focus

Intelligent Cloud (Azure)

Azure remains Microsoft’s primary earnings swing factor. Markets are watching to see whether any growth reflects demand strength or capacity constraints, and how AI-related workloads are impacting margins.

Productivity and Business Processes

Microsoft 365, Office, and LinkedIn are sources of recurring revenue for Microsoft. Growth, pricing discipline, and client churn remain the key variables that markets will be watching.

Personal Computing

Windows, devices, and gaming are more cyclical. Stabilisation of PC demand and gaming engagement remain secondary sources of revenue but are still noteworthy.

Artificial intelligence

Approaches around the monetisation of Microsoft’s AI play are still developing. Trends in enrolment and infrastructure cost are expected to be key factors.

What happened last quarter

Microsoft reported results ahead of consensus, supported by steady cloud demand and resilient enterprise software revenues.

Azure and other cloud services' growth remained a central focus, alongside commentary on AI-related investment and capacity.

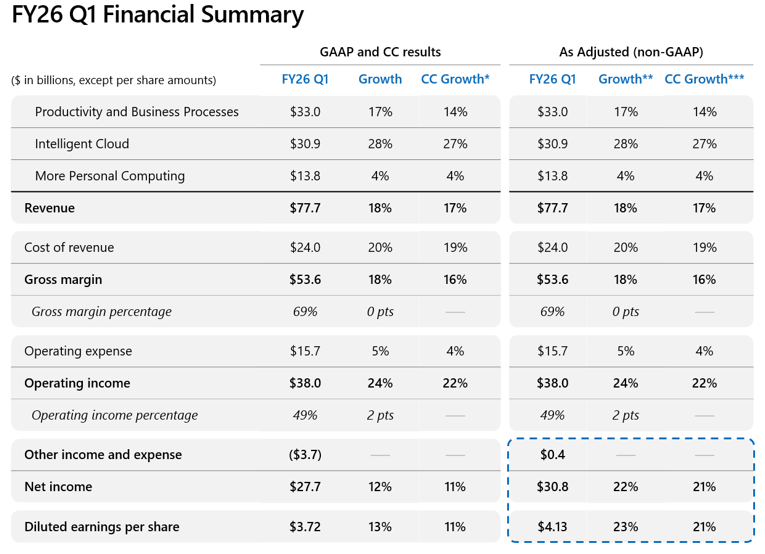

Last earnings key highlights:

- Revenue: US$77.7 billion

- Earnings per share (EPS): US$3.72 (GAAP) and US$4.13 (non-GAAP adjusted)

- Intelligent Cloud revenue: US$30.9 billion

- Azure and other cloud services: up 40% year on year

- Operating income: US$38.0 billion

How the market reacted last time

Microsoft shares fell in after-hours trading following the release, despite the beating of headline numbers, as investors focused on AI investment intensity, capacity constraints and related implications for future margins.

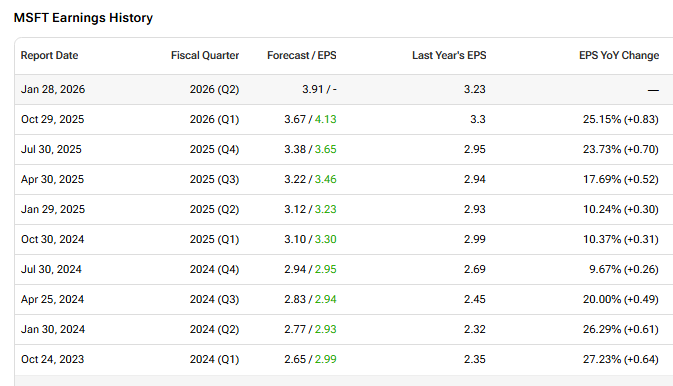

What’s expected this quarter

Bloomberg consensus points to continued revenue growth led by cloud services, alongside broadly stable margins despite elevated capex.

Bloomberg consensus reference points (January 2026):

- Revenue: about US$68 to US$69 billion

- EPS: about US$3.10 to US$3.20 (adjusted)

- Azure growth: mid-to-high 20% year on year (YoY) (constant currency)

- Operating margin: expected to remain broadly stable

- Capex: expected to remain elevated, reflecting AI and cloud build-out

*All above points observed as of 16 January 2026.

Expectations

Sentiment appears cautious. Microsoft can remain sensitive to any cloud, margin, or guidance disappointment, particularly where investors interpret investment intensity as open-ended.

Price action traded within an established range of US$472 and US$490 recently, but has moved below this in the last week.

Listed options were pricing an indicative move of around ±2% based on near-dated options expiring after 28 January and an at-the-money options-implied ‘expected move’ estimate.

Implied volatility was about 33.5% annualised into the event as observed on Barchart at 11:00 AEDT on 16th January 2026.

These are market-implied estimates and may change; actual post-earnings moves can be larger or smaller.

What this means for Australian traders

Microsoft’s earnings may influence near-term sentiment across US technology indices, particularly the Nasdaq, with potential spillover into global equity risk appetite and, in turn, the ASX.

As a major technology stock, and with Tesla (TSLA) also scheduled to report after the US close on the same day, volatility in Nasdaq-linked products may increase while futures markets remain open.

Important risk note

Immediately after the US close and into the early Asia session, Nasdaq 100 (NDX) futures and related CFD pricing can reflect thinner liquidity, wider spreads, and sharper repricing around new information.

Such an environment can increase gap risk and execution uncertainty relative to regular-hours conditions.

Reportingdates and release times are based on company investor relations calendars whereconfirmed. Where dates or times are not marked confirmed, they are GO Marketsestimates. Consensus EPS, revenue and analyst-range data are sourced fromBloomberg and Earnings Whispers, as at 09 July 2026 (AEST). Company guidance,backlog and operating metrics are sourced from the latest company filings orresults presentations, unless stated otherwise. Any scenario analysis reflectsGO Markets analysis. Figures and schedules may change without notice.

The information provided is of general nature only and does not take into account your personal objectives, financial situations or needs. Before acting on any information provided, you should consider whether the information is suitable for you and your personal circumstances and if necessary, seek appropriate professional advice. All opinions, conclusions, forecasts or recommendations are reasonably held at the time of compilation but are subject to change without notice. Past performance is not an indication of future performance. Go Markets Pty Ltd, ABN 85 081 864 039, AFSL 254963 is a CFD issuer, and trading carries significant risks and is not suitable for everyone. You do not own or have any interest in the rights to the underlying assets. You should consider the appropriateness by reviewing our TMD, FSG, PDS and other CFD legal documents to ensure you understand the risks before you invest in CFDs.