预计收益日期: 2026 年 2 月 4 日,星期三(美国,收盘后)/~ 2026 年 2 月 5 日星期四上午 8:00(澳大利亚东部夏令时间)

Alphabet的收益提供了对全球数字广告需求、企业云支出和更广泛的科技行业投资趋势的见解。

由于谷歌搜索和YouTube被消费者和企业广泛使用,因此在评估在线活动和企业营销预算以及其他指标时,通常将结果用作一种输入。

重点领域

搜寻

搜索广告仍然是Alphabet最大的收入驱动力。市场可能会关注广告增长率、定价指标(例如每次点击费用)以及零售、旅游和中小型企业等领域的总体广告商需求。

优酷

YouTube为广告和订阅收入做出了贡献。市场通常监控广告势头、参与度趋势和盈利发展,以此作为数字媒体状况和品牌支出的指标。

谷歌云

尽管结果仍不确定,但持续的云盈利能力通常被视为可能影响长期收益预期的因素。预计市场将关注收入增长、企业采用趋势和营业利润率。

其他赌注

自动驾驶和生命科学等举措虽然通常对收入的贡献较小,但市场仍可能将支出水平和进展更新视为资本配置和成本纪律的指标。

成本和利润框架

管理层此前曾表示,与人工智能基础设施(包括数据中心、专用芯片和计算能力)相关的资本支出增加。流量获取成本、人员配备水平和基础设施扩张也是影响盈利能力的关键变量。

上个季度发生了什么

Alphabet的最新季度更新重点介绍了广告趋势、云盈利能力以及支持人工智能计划的资本支出的持续增长。

管理层的评论表明,基础设施支出旨在支持长期竞争力,而市场仍在评估短期利润权衡。

最新财报主要亮点

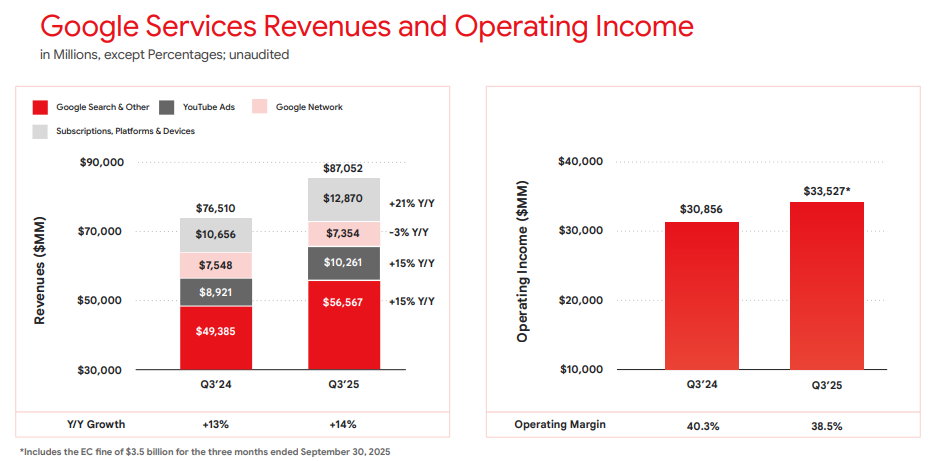

有关最近一个季度的报告数据和细分市场细节,请参阅Alphabet的最新财报发布材料,包括收入、每股收益(EPS)、服务组合、云运营收入和资本支出评论。

- 收入: 1023.5 亿美元

- EPS: 2.87 美元

- 营业收入: 312.3 亿美元

- 服务收入: 870.5 亿美元

- 云收入: 15.16 亿美元

2025 年第三季度谷歌服务收入和营业收入 | Alphabet 财报

本季度的预期

彭博社的共识估计,与去年同期相比,收入同比(YoY)增长温和,每股收益将增加,鉴于人工智能相关投资,营业利润率将继续受到关注。

彭博共识参考点:

- EPS: 低至中等 2 美元区间

- 收入: 高达800亿美元至900亿美元低点区间

- 资本支出: 预计将保持较高水平

*截至2026年1月31日观察到的所有上述观点。

市场隐含的预期

上市期权暗示在相关的近期到期窗口内,指示性预期波动幅度约为±4%至±6%。变动源于澳大利亚东部夏令时间2026年2月2日上午11点观察到的期权价格。

这些是市场隐含的估计,可能会发生变化。盈利后的实际价格变动可能更大或更小。

这对澳大利亚市场参与者意味着什么

Alphabet的收益可能会影响美国主要股指的短期情绪,尤其是与纳斯达克挂钩的产品,并有可能在发布后溢出到亚洲时段。

重要风险说明

在美国收盘并进入亚洲早盘后,纳斯达克100(NDX)期货和相关的差价合约定价可以立即反映出流动性减弱、利差扩大,以及围绕新信息的更大幅度重新定价。

相对于正常工作时间条件,这样的环境会增加差距风险和执行不确定性。

Reportingdates and release times are based on company investor relations calendars whereconfirmed. Where dates or times are not marked confirmed, they are GO Marketsestimates. Consensus EPS, revenue and analyst-range data are sourced fromBloomberg and Earnings Whispers, as at 09 July 2026 (AEST). Company guidance,backlog and operating metrics are sourced from the latest company filings orresults presentations, unless stated otherwise. Any scenario analysis reflectsGO Markets analysis. Figures and schedules may change without notice.

The information provided is of general nature only and does not take into account your personal objectives, financial situations or needs. Before acting on any information provided, you should consider whether the information is suitable for you and your personal circumstances and if necessary, seek appropriate professional advice. All opinions, conclusions, forecasts or recommendations are reasonably held at the time of compilation but are subject to change without notice. Past performance is not an indication of future performance. Go Markets Pty Ltd, ABN 85 081 864 039, AFSL 254963 is a CFD issuer, and trading carries significant risks and is not suitable for everyone. You do not own or have any interest in the rights to the underlying assets. You should consider the appropriateness by reviewing our TMD, FSG, PDS and other CFD legal documents to ensure you understand the risks before you invest in CFDs.