You might have heard about Hong Kong in the news, recently they celebrated twenty years of “return to the motherland”. Before we discuss the HK50 index, it’s let’s briefly review the historical and political situation. You might be asking yourself, is Hong Kong a separate country or part of China? [caption id="attachment_57013" align="alignright" width="450"] Source: https://www.hsi.com.hk/HSI-Net/static/revamp/contents/en/dl_centre/factsheets/FS_HSIe.pdf [/caption] In the strictest sense, Hong Kong is part of China, her official name being Hong Kong Special Administrative Region of the People's Republic of China.

Confusingly, Hong Kong has her own immigration policy, money, stock exchange, postage stamps, flag, etc. This peculiar arrangement is due to the fact that Hong Kong was a British colony from 1841 to 1997. The treaty on “return” stipulated that Hong Kong would continue to operate in a different fashion than most of China, known as “One country, two systems”.

The Hang Seng 50 (HK50 on the GoTrader MT4) has a market capitalization-weighted index of 50 of the largest companies that trade on the Hong Kong Exchange. These companies cover approximately 65% of its total market capitalization. Finance represents almost half of the index.

An additional quarter is weighted in information technology, properties, and telecommunications. As you can see in the weekly view below, HK50 recently broke the 25,000 point mark for the first time in nearly two years. From an all-time high in April 2015, it was last over 25,000 in July 2015.

Continuing a rally from January 2016 which saw the index drop to a five year low. [caption id="attachment_57014" align="alignleft" width="600"] Source: Go Trader MT4 HK50[/caption] Despite the fact that the index’s constituent companies are listed in Hong Kong, 55% of the companies are based in China. A meteoric rise from 5% in 1997, 25% in 2003 and an all-time high of 59% in 2009. HK50 is tied at the hip to the Chinese economy.

How tied is HK50 to mainland Chinese companies you ask? On Tuesday July 4 th shares suffered their worst day in 2017, falling 1.5%, representing the biggest one-day percentage fall since December 15 th. Tencent, one of the ten most valuable companies in the world, headquartered in nearby Shenzhen and making up nearly 11% of the composite.

Tumbled 4% relating to recent negative comments around its popular one-line game products, we should continue to see growth as China's first-quarter GDP growth hit 6.9%, the highest level since the fall. By: Samuel Hertz GO Markets

By

GO Markets

The information provided is of general nature only and does not take into account your personal objectives, financial situations or needs. Before acting on any information provided, you should consider whether the information is suitable for you and your personal circumstances and if necessary, seek appropriate professional advice. All opinions, conclusions, forecasts or recommendations are reasonably held at the time of compilation but are subject to change without notice. Past performance is not an indication of future performance. Go Markets Pty Ltd, ABN 85 081 864 039, AFSL 254963 is a CFD issuer, and trading carries significant risks and is not suitable for everyone. You do not own or have any interest in the rights to the underlying assets. You should consider the appropriateness by reviewing our TMD, FSG, PDS and other CFD legal documents to ensure you understand the risks before you invest in CFDs. These documents are available here.

2025 has seen a material decline in the fortunes of the greenback. A technical structure breakdown early in the year was followed by a breach of the 200-day moving average (MA) at the end of Q1. The index then entered correction territory, printing a three-year low at the end of Q2.

Since then, we have seen attempts to build a technical base, including a re-test of the end-of-June lows in mid-September. However, buying pressure has not been strong enough to push price back above the technically critical and psychologically important 100 level.

What the levels suggest from here

As things stand, the index remains more than 10% lower for 2025. On this technical view, the index may revisit the 96 area. However, technical levels can fail and outcomes depend on multiple factors.

US dollar index

Source: TradingView

The key question for 2026

The key question remains: are we likely to see further losses in the early part of next year and beyond, or will current support hold?

We cannot assess the US dollar in isolation and any outlook is shaped by internal and global factors, not least its relative strength versus other major currencies. Many of these drivers are interrelated, but four potential headwinds stand out for any US dollar recovery. Collectively, they may keep downside pressure in play.

Four headwinds for any US dollar recovery

1. The US dollar as a safe-haven trade

One scenario where US dollar support has historically been evident is during major global events, slowdowns and market shocks. However, the more muted response of the US dollar during risk-off episodes this year suggests a shift away from the historical norm, with fewer sustained US dollar rallies.

Instead, throughout 2025, some investors appearedto favour gold, and at other times, FX and even equities, rather than into the US dollar. If this change in behaviour persists through 2026, it could make recovery harder, even if global economic pressure builds over the year ahead.

2. US versus global trade

Trade policy is harder to measure objectively, and outcomes can be difficult to predict. That said, trade battles driven by tariffs on US imports are often viewed as an additional potential drag on the US dollar.

The impact may be twofold if additional strain is placed on the US economy through:

a slowdown in global trade volumes as impacted countries seek alternative trade relationships, with supply chain distortions that may not favour US growth

pressure on US corporate profit margins as tariffs lift costs for importers

3. Removal of quantitative tightening

The Fed formally halted its balance sheet reduction, quantitative tightening (QT), as of 1 December 2025, ending a program that shrank assets by roughly US$2.4 trillion since mid-2022.

Traditionally, ending QT is seen as marginally negative for the US dollar because it stops the withdrawal of liquidity, can ease global funding conditions, and may reduce the scarcity that can support dollar demand. Put simply, more dollars in the system can soften the currency’s support at the margin, although outcomes have varied historically and often depend on broader financial conditions.

4. Interest rate differential

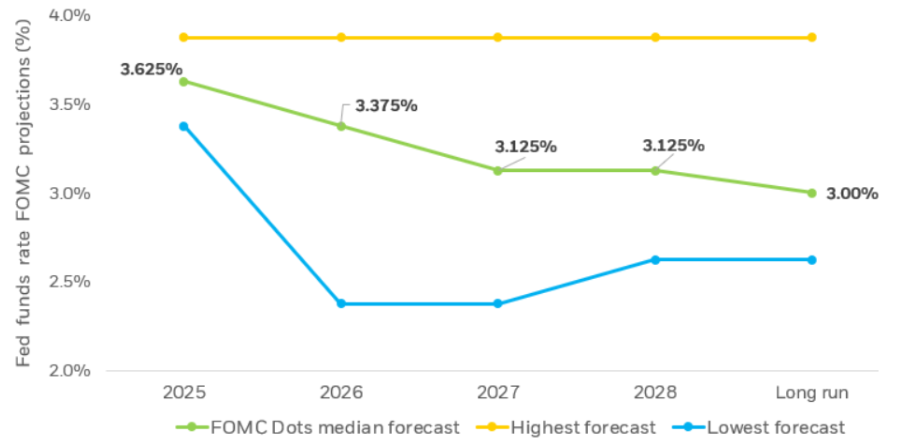

Interest rate differential (IRD) is likely to be a primary driver of US dollar strength, or otherwise, in the months ahead. The latest FOMC meeting delivered the expected 0.25% cut, with attention on guidance for what may come next.

Even after a softer-than-expected CPI print, markets have been reluctant to price aggressive near-term easing. At the time of writing, less than a 20% chance of a January cut is priced in, and it may be March before we see the next move.

The Fed is balancing sticky inflation against a jobs market under pressure, with the headline rate back at levels last seen in 2012. The practical takeaway is that a more accommodative stance may add to downward pressure on the US dollar.

Current expectations imply around two rate cuts through 2026, with the potential for further easing beyond that, broadly consistent with the median projections shown in the chart below. These are forecasts rather than guarantees, and they can shift as economic data and policy guidance evolve.

Source: US Federal Reserve, Summart of Economic Projections

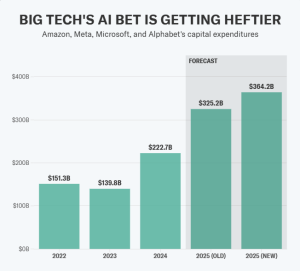

The “Magnificent Seven” technology companies are expected to invest a combined $385 billion into AI by the end of 2025.

Microsoft is positioning itself as the platform leader. Nvidia dominates the underlying AI infra. Google leads in research. Meta is building open-source tech. Amazon – AI agents. Apple — on-device integration. And Tesla pioneering autonomous vehicles and robots.

The “Big 4” tech companies' AI spending alone is forecast at $364 billion.

With such enormous sums pouring into AI, is this a winner-take-all game?

Or will each of the Mag Seven be able to thrive in the AI future?

Microsoft: The AI Everywhere Strategy

Microsoft has made one of the biggest bets on AI out of the Mag Seven — adopting the philosophy that AI should be everywhere.

Through its deep partnership with OpenAI, of which it is a 49% shareholder, the company has integrated GPT-5 across its entire ecosystem.

Key initiatives:

GPT-5 integration across consumer, enterprise, and developer tools through Microsoft 365 Copilot, GitHub Copilot, and Azure AI Foundry

Azure AI Foundry for unified AI development platform with model router technology

Copilot ecosystem spanning productivity, coding, and enterprise applications with real-time model selection

$100 billion projected AI infrastructure spending for 2025

Microsoft’s centrepiece is Copilot, which can now detect whether a prompt requires advanced reasoning and route to GPT-5's deeper reasoning model.

This (theoretically) means high-quality AI outputs become invisible infrastructure rather than a skill users need to learn.

However, this all-in bet on OpenAI does come with some risks. It is putting all its eggs in OpenAI's basket, tying its future success to a single partnership.

Elon Musk warned that "OpenAI is going to eat Microsoft alive"[/caption]

Google: The Research Strategy

Google’s approach is to fund research to build the most intelligent models possible. This research-first strategy creates a pipeline from scientific discovery to commercial products — what it hopes will give it an edge in the AI race.

Key initiatives:

Over 4 million developers building with Gemini 2.5 Pro and Flash

Ironwood TPU offering 3,600 times better performance compared to Google’s first TPU

AI search overviews reaching 2 billion monthly users across Google Search

DeepMind breakthroughs: AlphaEvolve for algorithm discovery, Aeneas for ancient text interpretation, AlphaQubit for quantum error detection, and AI co-scientist systems

Google’s AI research branch, DeepMind, brings together two of the world's leading AI research labs — Google Brain and DeepMind — the former having invented the Transformer architecture that underpins almost all modern large language models.

The bet is that breakthrough research in areas like quantum computing, protein folding, and mathematical reasoning will translate into a competitive advantage for Google.

Today, we're introducing AlphaEarth Foundations from @GoogleDeepMind , an AI model that functions like a virtual satellite which helps scientists make informed decisions on critical issues like food security, deforestation, and water resources. AlphaEarth Foundations provides a… pic.twitter.com/L1rk2Z5DKk

Meta has made a somewhat contrarian bet in its approach to AI: giving away their tech for free. The company's Llama 4 models, including recently released Scout and Maverick, are the first natively multi-modal open-weight models available.

Key initiatives:

Llama 4 Scout and Maverick - first open-weight natively multi-modal models

AI Studio that enables the creation of hundreds of thousands of AI characters

$65-72 billion projected AI infrastructure spending for 2025

This open-source strategy directly challenges the closed-source big players like GPT and Claude. By making AI models freely available, Meta is essentially commoditizing what competitors are trying to monetize. Meta's bet is that if AI models become commoditized, the real value will be in the infrastructure that sits on top. Meta's social platforms and massive user base give it a natural advantage if this eventuates.

Meta's recent quarter was also "the best example to date of AI having a tangible impact on revenue and earnings growth at scale," according to tech analyst Gene Munster.

H1 relative performance of the Magnificent Seven stocks. Source: KoyFin, Finimize

However, it hasn’t been all smooth sailing for Meta. Their most anticipated release, Llama Behemoth, has all but been scrapped due to performance issues. And Meta is now rumored to be developing a closed-source Behemoth alternative, despite their open-source mantra.

Amazon: The AI Agent Strategy

Amazon’s strategy is to build the infrastructure for AI that can take actions — booking meetings, processing orders, managing workflows, and integrating with enterprise systems.

Rather than building the best AI model, Amazon has focused its efforts on becoming the platform where all AI models live.

Key initiatives:

Amazon Bedrock offering 100+ foundation models from leading AI companies, including OpenAI models.

$100 million additional investment in AWS Generative AI Innovation Center for agentic AI development

Amazon Bedrock AgentCore enabling deployment and scaling of AI agents with enterprise-grade security

$118 billion projected AI infrastructure spending for 2025

The goal is to become the “orchestrator” that lets companies mix and match the best models for different tasks.

Amazon’s AgentCore will provide the underlying memory management, identity controls, and tool integration needed for these companies to deploy AI agents safely at scale.

This approach offers flexibility, but does carry some risks. Amazon is essentially positioning itself as the middleman for AI. If AI models become commoditized or if companies prefer direct relationships with AI providers, Amazon's systems could become redundant.

Nvidia: The Infra Strategy

Nvidia is the one selling the shovels for the AI gold rush. While others in the Mag Seven battle to build the best AI models and applications, Nvidia provides the fundamental computing infrastructure that makes all their efforts possible.

This hardware-first strategy means Nvidia wins regardless of which company ultimately dominates. As AI advances and models get larger, demand for Nvidia's chips only increases.

Key initiatives:

Blackwell architecture achieving $11 billion in Q2 2025 revenue, the fastest product ramp in company history

New chip roadmap: Blackwell Ultra (H2 2025), Vera Rubin (H2 2026), Rubin Ultra (H2 2027)

Data center revenue reaching $35.6 billion in Q2, representing 91% of total company sales

Manufacturing scale-up with 350 plants producing 1.5 million components for Blackwell chips

With an announced product roadmap of Blackwell Ultra (2025), Vera Rubin (2026), and Rubin Ultra (2027), Nvidia has created a system where the AI industry must continuously upgrade to Nvidia’s newest tech to stay competitive.

This also means that Nvidia, unlike the others in the Mag Seven, has almost no direct AI spending — it is the one selling, not buying.

However, Nvidia is not indestructible. The company recently halted its H20 chip production after the Chinese government effectively blocked the chip, which was intended as a workaround to U.S. export controls.

Apple: The On-Device Strategy

Apple's AI strategy is focused on privacy, integration, and user experience. Apple Intelligence, the AI system built into iOS, uses on-device processing and Private Cloud Compute to help ensure user data is protected when using AI.

Key initiatives:

Apple Intelligence with multi-model on-device processing and Private Cloud Compute

Enhanced Siri with natural language understanding and ChatGPT integration for complex queries

Direct developer access to on-device foundation models, enabling offline AI capabilities

$10-11 billion projected AI infrastructure spending for 2025

The drawback of this on-device approach is that it requires powerful hardware from the user's end. Apple Intelligence can only run on devices with a minimum of 8GB RAM, creating a powerful upgrade cycle for Apple but excluding many existing users.

Tesla: The Robo Strategy

Tesla's AI strategy focuses on two moonshot applications: Full Self-Driving vehicles and humanoid robots.

This is the 'AI in the physical world' play. While others in the Mag Seven are focused on the digital side of AI, Tesla is building machines that use AI for physical operations.

Tesla’s Optimus robot replicating human tasks

Key initiatives:

Plans for 5,000-10,000 Optimus robots in 2025, scaling to 50,000 in 2026

Robotaxi service targeting availability to half the U.S. population by EOY 2025

AI6 chip development with Samsung for unified training across vehicles, robots, and data centers

$5 billion projected AI infrastructure spending for 2025

This play is exponentially harder to develop than digital AI, and the markets have reflected low confidence that Tesla can pull it off.

TSLA has been the worst-performing Mag Seven stock of 2025, down 18.37% in H1 2025.

However, if Tesla’s strategy is successful, it could be far more valuable than other AI plays. Robots and autonomous vehicles could perform actual labour worth trillions of dollars annually.

The $385 billion Question

The Mag Seven are starting to see real revenue come in from their AI investments. But they're pouring that money (and more) back into AI, betting that the boom is just getting started.

The platform players like Microsoft and Amazon are betting on becoming essential infrastructure. Nvidia’s play is to sell the underlying hardware to everyone. Google and Meta compete on capability and access. While Apple and Tesla target specific use cases.

The $385 billion question is which of the Magnificent Seven has bet the right way? Or will a new player rise and usurp the long-standing tech giants altogether?

You can access all Magnificent Seven stocks and thousands of other Share CFDs on GO Markets.

Over the past 3 months Nvidia has moved through ranges that some stocks don’t do in years, in some cases decades. Having lost over 35 per cent in the June to August sell off, it quickly bounced over 40 per cent in the preceding 20 days once it hit its August low as we build positions ahead of its results. These results delivered Nvidia style numbers with three figure growth on the sales, net profit and earnings lines but this did not appease the market, seeing it fall 22 per cent in a little over 8 days.

Which brings us to now – a new 16 per cent drive as Nivida reports it’s struggling to meet demands and that the AI revolution is translating faster than even it expected. This got us thinking – Where are we right “Now” in the AU players? Thus, it’s time to dive into the drivers for the Nvidia and Co.

AI players. Supersonic As mentioned, Nvidia’s results have been astonishing – and it still has time to do a US$50 billion buyback. It collected the award for becoming the world’s largest company in the shortest timeframe in the post-WWII era, think about that for one second – that’s faster than Amazon, Microsoft, Apple, Google, Shell, BP, ExxonMobil, TV players of the 60s and 70s.

So the question is how does it keep its speed and trajectory? Well that comes from what some are calling the ‘supersonic’ scalers. These are the players like Google, Amazon, Meta and Microsoft that are the users and providers of the AI revolution.

These are the players that have spent hundreds billions thus far on the third digital revolution. Let us once again put that into perspective, the amount of spending is (inflation adjusted) the same as what was spent during the 1960’s on mainframe computing and the 1990’s distribution of fibre-optics. So we have now seen that level of spending in AI the next step is ‘usage’ and that is the inflection point we find ourselves at.

Currently AI is mainly used to train foundational models and chatbots – which is fine but not long-term financially stable. It needs to move into things like productions – that is producing models for corporate clients that forecast, streamline and increase productivity. This is the ‘Grail’ This immediately raises the bigger question for now – can this Grail be achieved?

The Voices To answer that – let us present some arguments from some of AI’s largest “Voices” On the AI potential and the possibility of a profound and rapid technological revolution, Sam Altman, CEO of OpenAI, has claimed that AI represents the "biggest, best, and most important of all technology revolutions," and predicts that AI will become increasingly integrated into all aspects of life. This reflects a belief in AI's far-reaching influence over time. The never subtle McKinsey and Co. has projected that generative AI could eventually contribute up to $8 trillion to the global economy annually.

This figure underscores the massive economic potential of AI. The huge caveat: McKinsey's predictions are never real-world tested and inevitably fall flat in the market. This kind of money is what makes AI so attractive to players in Venture Capital.

For the VC watchers out there the one that is catching everyone’s attention is VC accelerator Y Combinator which is fully embracing the technology. Just to put Y Combinator into context, according to Jared Heyman’s Rebel Fund, if anyone had invested in every Y Combinator deal since 2005 (which would have been impossible just to let you know), the average annual return would have been 176%, even after accounting for dilution. Furthermore to the VC story - AI has accounted for over 40 per cent of new unicorns (startups valued at $1 billion or more) in the first half of 2024, and 60 per cent of the increase in VC-backed valuations.

So far in 2024, U.S. unicorn valuations have grown by $162 billion, largely driven by AI’s rapid expansion, according to Pitchbook data. So the Voices certainly believe it can be achieved. But is this a good thing?

The Good, the Bad and the Ugly AI is advancing at such a rapid pace that existing performance benchmarks, such as reading comprehension, image classification and advanced maths, are becoming outdated, necessitating the creation of new standards. This reflects the fast-moving nature of AI progress. For example, look at the success of AlphaFold, an AI-driven algorithm that accurately predicts protein structures.

Some see this as one of the most important achievements in AI’s short history and underscores AI’s transformative impact on science, particularly in fields like biology and healthcare. This is the Good. Then there is the 165-page paper titled "Situational Awareness" by Aschenbrenner which has predicted that by 2030, AI will achieve superintelligence and create a $1 trillion industry.

Also, a positive, but will consume 20 per cent of the U.S. power supply. These incredible predictions emphasise the enormous scale of AI and the impact it will have on industry, infrastructure and people. The latest Google study found that generative AI could significantly improve workforce productivity.

The study suggests that roughly 80 per cent of jobs could see at least 10 per cent of tasks completed twice as fast due to AI, which has implications for industries such as call centres, coding, and professional writing. This highlights AI's capacity to streamline tasks and enhance efficiency across various fields. However it also raises the massive concern around job security, job satisfaction and the socio-economic divide as the majority of those affected by AI ‘productivity’ are in mid to low scales.

Then we come to Elon Musk’s new AI startup, xAI, which raised $6 billion at a valuation of $24 billion this year. The company is planning to build the world’s largest supercomputer in Tennessee to support AI training and inference. This all sounds economically and financially exciting but it has a darker side.

These are the kinds of AI ventures that have seen ‘deep-fake’ creations. For example Musk himself shared a deep-fake video of Vice President Kamala Harris. This is the ugly side of AI and reflects the broader cultural and ethical issues surrounding AI-generated content.

Furthermore – we should always be forecasting both the good and the bad for investment opportunities. These issues are already attracting regulations and compliance responses. How impactful will these be?

And will it halt the AI driven share price appreciation? It is a very real and present issue. Where does this leave us?

The share price future of Nvidia and Co is clearly dependent on the longer-term achievement of the AI revolution. As shown, the supersonic players in technology and venture capital are betting big on AI, with predictions that it will reshape the global economy, industries, and even basic societal structures. However, there is still uncertainty about the exact timeline for these changes and how accurately the market is pricing in AI's potential.

The AI ecosystem is moving at breakneck speed, with new developments outpacing benchmarks and productivity gains reshaping jobs, but whether all these projections that range from trillion-dollar economies to superintelligence materialises remains to be seen. Thus – for now – Nvidia and Co’s recent roller-coaster trading looks set to continue.

In 2025, the ASX 200 closed around 8,621 points and was up approximately 6% year to date (YTD) as of 19 December close. Market direction was most sensitive to Reserve Bank of Australia (RBA) expectations, commodity prices and China-linked demand, and (to a lesser extent) moves in the Australian dollar (AUD). The index recovered from November’s pullback, but remained below October’s record close.

Key 2025 drivers included:

RBA policy expectations: Sentiment was shaped by shifting views on the timing and extent of rate moves. The November pullback reflected repricing towards a longer pause and higher uncertainty around whether the next move could be a hike rather than a cut, particularly as jobs and inflation data surprised.

Resources and China sensitivity: With a meaningful resources weight, the index responded to iron ore stability, strong gold prices and relative firmness in base metals. China data and any perceived policy support (including signals from the People’s Bank of China (PBOC)) remained important for the export backdrop. A relatively stable AUD also reduced currency-related noise for exporters.

Index composition and market structure: The ASX 200’s heavier tilt to materials and banks, and lower exposure to high-growth technology, meant it often lagged tech-led global rallies, but tended to hold up better when AI and growth valuations were questioned.

Corporate earnings: Reporting season outcomes influenced valuation support. In September’s half-year reporting season, around 33% of ASX 200 companies beat expectations, which helped underpin pricing around current levels.

Current state

The ASX 200 was roughly 5% below its late-October record high close of 9,094 points. After the November retracement, support around 8,400 appeared to hold and buying interest improved. The 50-day EMA near 8,730 (a prior consolidation area) was a commonly watched near-term reference, noting technical indicators can be unreliable.

What to watch in January

China and commodity demand: Growth, trade and any fresh stimulus inference from the PBOC may affect sentiment.

Domestic inflation and labour data: CPI and jobs prints are key inputs into RBA expectations.

Key levels and follow-through: The post-November rebound may need continued demand to sustain momentum.

Source: Trading View

What moved the Nikkei 225 in 2025?

In 2025, the Nikkei 225 traded around 39,200 points and was up approximately 21% year to date (YTD). Market direction was most sensitive to moves in the Japanese yen (JPY) and Bank of Japan (BOJ) communication, with the index consolidating after multi-decade highs. While broader signals remained constructive, consolidation can resolve either higher or lower.

Key influences included:

JPY movements and earnings translation: A weaker JPY can boost the reported value of overseas earnings for some exporters, although it may also increase input and import costs. The net impact often depends on company hedging practices and varies by sector, with effects most evident in export-heavy industries such as automotive, industrials and parts of technology manufacturing.

Gradual BOJ policy transition: The BOJ continued to step away from ultra-easy settings, but tightening was generally cautious. Markets largely priced a slow, conditional normalisation, which helped limit downside, even as policy headlines created bouts of volatility.

Corporate governance reforms: Ongoing improvements in capital efficiency and shareholder returns supported interest from overseas investors. Share buybacks, stronger balance-sheet discipline and improved return on equity (ROE) contributed to re-rating in parts of the market.

Global cyclical exposure: The Nikkei moved with shifts in global manufacturing sentiment and expectations for US growth, particularly during risk-on phases associated with AI-related capital spending.

Current state

After pushing to multi-decade highs earlier in the year, the Nikkei spent time consolidating but has remained structurally strong. Price sits above key long-term moving averages, and some technicians watch the 50-day exponential moving average (EMA) as a potential reference level (noting these indicators can be unreliable). Currency swings and shifting BOJ expectations were commonly cited as contributors to much of the second-half volatility, although pullbacks were generally met with buying interest.

What to watch in January for Japan

JPY volatility: Sharper yen moves, especially if driven by BOJ or Federal Reserve expectations, could quickly change exporter earnings assumptions.

BOJ communication: Small changes in language on inflation persistence or bond market operations may move sentiment.

Global growth data: US and China manufacturing and trade prints remain key inputs for an externally focused economy.

2025 has seen a material decline in the fortunes of the greenback. A technical structure breakdown early in the year was followed by a breach of the 200-day moving average (MA) at the end of Q1. The index then entered correction territory, printing a three-year low at the end of Q2.

Since then, we have seen attempts to build a technical base, including a re-test of the end-of-June lows in mid-September. However, buying pressure has not been strong enough to push price back above the technically critical and psychologically important 100 level.

What the levels suggest from here

As things stand, the index remains more than 10% lower for 2025. On this technical view, the index may revisit the 96 area. However, technical levels can fail and outcomes depend on multiple factors.

US dollar index

Source: TradingView

The key question for 2026

The key question remains: are we likely to see further losses in the early part of next year and beyond, or will current support hold?

We cannot assess the US dollar in isolation and any outlook is shaped by internal and global factors, not least its relative strength versus other major currencies. Many of these drivers are interrelated, but four potential headwinds stand out for any US dollar recovery. Collectively, they may keep downside pressure in play.

Four headwinds for any US dollar recovery

1. The US dollar as a safe-haven trade

One scenario where US dollar support has historically been evident is during major global events, slowdowns and market shocks. However, the more muted response of the US dollar during risk-off episodes this year suggests a shift away from the historical norm, with fewer sustained US dollar rallies.

Instead, throughout 2025, some investors appearedto favour gold, and at other times, FX and even equities, rather than into the US dollar. If this change in behaviour persists through 2026, it could make recovery harder, even if global economic pressure builds over the year ahead.

2. US versus global trade

Trade policy is harder to measure objectively, and outcomes can be difficult to predict. That said, trade battles driven by tariffs on US imports are often viewed as an additional potential drag on the US dollar.

The impact may be twofold if additional strain is placed on the US economy through:

a slowdown in global trade volumes as impacted countries seek alternative trade relationships, with supply chain distortions that may not favour US growth

pressure on US corporate profit margins as tariffs lift costs for importers

3. Removal of quantitative tightening

The Fed formally halted its balance sheet reduction, quantitative tightening (QT), as of 1 December 2025, ending a program that shrank assets by roughly US$2.4 trillion since mid-2022.

Traditionally, ending QT is seen as marginally negative for the US dollar because it stops the withdrawal of liquidity, can ease global funding conditions, and may reduce the scarcity that can support dollar demand. Put simply, more dollars in the system can soften the currency’s support at the margin, although outcomes have varied historically and often depend on broader financial conditions.

4. Interest rate differential

Interest rate differential (IRD) is likely to be a primary driver of US dollar strength, or otherwise, in the months ahead. The latest FOMC meeting delivered the expected 0.25% cut, with attention on guidance for what may come next.

Even after a softer-than-expected CPI print, markets have been reluctant to price aggressive near-term easing. At the time of writing, less than a 20% chance of a January cut is priced in, and it may be March before we see the next move.

The Fed is balancing sticky inflation against a jobs market under pressure, with the headline rate back at levels last seen in 2012. The practical takeaway is that a more accommodative stance may add to downward pressure on the US dollar.

Current expectations imply around two rate cuts through 2026, with the potential for further easing beyond that, broadly consistent with the median projections shown in the chart below. These are forecasts rather than guarantees, and they can shift as economic data and policy guidance evolve.

Source: US Federal Reserve, Summart of Economic Projections

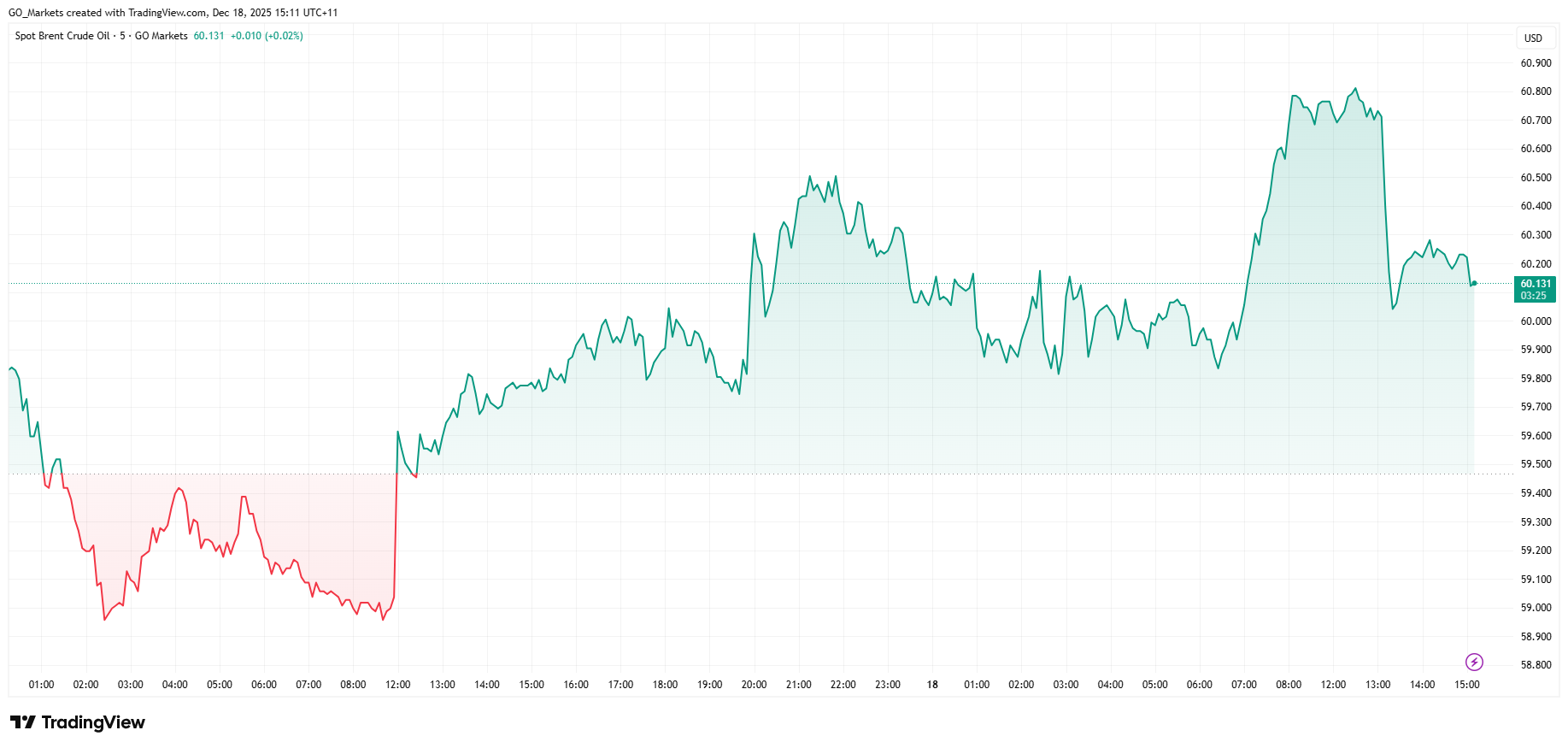

Donald Trump has officially declared the Maduro regime in Venezuela a foreign terrorist organisation and ordered a "total and complete blockade" of the country's sanctioned oil tankers.

The U.S. has positioned 11 warships in the Caribbean to enforce the blockade, which could remove 400,000 to 500,000 barrels daily from global supply.

The move sent crude prices jumping over 2% and sparked renewed concerns about supply stability heading into 2026.

UKOUSD 48-hour chart

White House Chief of Staff Susie Wiles succinctly summarised the situation as: “Trump wants to keep on blowing boats up until Maduro cries uncle."

Brent crude jumped 2.4% to $60.33 per barrel, while WTI climbed 2.6% to $56.69.

If crude maintains its $60 per barrel price, analysts project the blockade, combined with potential Russian sanctions, could push prices toward $70 as Venezuela's already-devastated economy faces collapse.

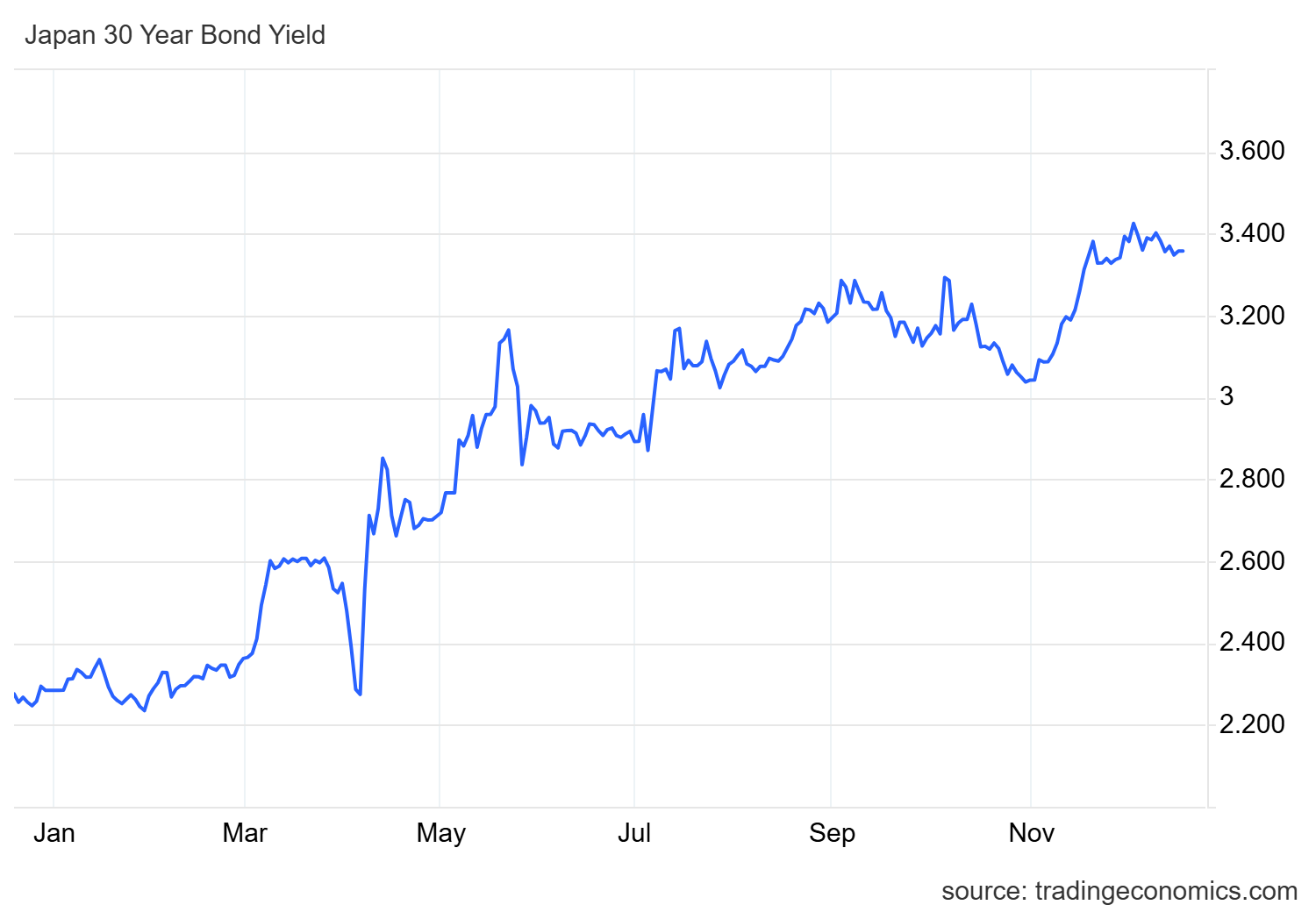

Bank of Japan to Hike Rates to Highest Level in Decades

The Bank of Japan is set to raise interest rates to their highest level in three decades this Friday, with Governor Kazuo Ueda expected to lift the benchmark rate from 0.5% to 0.75%.

While modest by global standards, this marks a landmark step in Japan's departure from decades of near-zero rates and unconventional easing.

The decision comes amid significant market turbulence. Japanese government bond yields have surged, with 30-year bonds hitting record highs and 10-year yields reaching 19-year peaks.

The volatility stems partly from concerns under new Prime Minister Sanae Takaichi, who recently approved a $118 billion stimulus package with over 60% financed through borrowing.

While Friday's hike appears certain, policymakers have signalled caution as they push rates toward levels estimated between 1% and 2.5%.

Ueda's post-meeting press conference will be closely watched for signals about future increases.

Micron Forecasts Blowout Earnings on Booming AI Market

Micron Technology is projecting second-quarter earnings of $8.42 per share, nearly double Wall Street's $4.78 estimate.

Micron shares surged 7% in after-hours trading as markets reacted to the news that the AI-driven memory chip race is showing no signs of slowing.

As one of only three major suppliers of high-bandwidth memory (HBM) chips alongside SK Hynix and Samsung, Micron sits at a chokepoint in AI infrastructure.

The HBM specialised chips are essential for training and deploying generative AI models, and current demand is dramatically outpacing supply.

CEO Sanjay Mehrotra revealed that supply tightness will extend beyond 2026, with Micron expecting to fulfil only 50-70% of key customer demand in the medium term.

Micron projects revenue of $18.70 billion this quarter versus analyst estimates of $14.20 billion. The company has retooled their operations toward AI applications, even dissolving its consumer "Crucial" brand to concentrate on AI data centre demand.

HBM chips are now the bottleneck in AI system performance, and suppliers who can deliver at scale have the potential to capture large amounts of value over the coming years.