Go further with GO Markets

Trade smarter with a trusted global broker. Low spreads, fast execution, powerful platforms, and award-winning customer support.

20 Years Strong

Celebrating 20 years of trading excellence.

Built for traders since 2006.

For beginners

Just getting

started?

Explore the basics and build your confidence.

For intermediate traders

Take your

strategy further

Access advanced tools for deeper insights than ever before.

Professionals

For professional

traders

Discover our dedicated offering for professionals and sophisticated investors.

Get more out of every trade

Explore our limited-time special offers

Get Started with GO Markets

Whether you’re new to markets or trading full time, GO Markets has an

account tailored to your needs.

Trusted by traders worldwide

Since 2006, GO Markets has helped hundreds of thousands of traders to pursue their trading goals with confidence and precision, supported by robust regulation, client-first service, and award-winning education.

*Trustpilot reviews are provided for the GO Markets group of companies and not exclusively for GO Markets Ltd.

*Awards were awarded to GO Markets group of companies and not exclusively to GO Markets Ltd.

Explore more from GO Markets

CFD markets

Trade CFDs across forex, indices, shares, commodities, metals, ETFs and more.

Platforms & tools

Trading accounts with seamless technology, award-winning client support, and easy access to flexible funding options.

Academy

Learn the skills, strategies, and mindset behind long-term trading success.

Accounts & pricing

Compare account types, view spreads, and choose the option that fits your goals.

Go further with

GO Markets.

Explore thousands of tradable opportunities with institutional-grade tools, seamless execution, and award winning support. Opening an account is quick and easy.

News & insights

Powerful tools for every trading style and preference.

The latest move in oil has put energy names back in focus. Over the past six months, Exxon Mobil and Baker Hughes have outperformed Brent crude on a normalised basis, Chevron has remained broadly constructive, SLB has lagged the commodity and Woodside's broker consensus has been more measured.

When crude moves, the impact rarely stays contained to the commodity itself. Higher oil prices can affect inflation expectations, shipping costs and corporate margins across the global economy.

What the latest move is showing

There are three broad ways companies can benefit from firmer oil prices:

- Producing oil and gas, by selling the commodity at a higher price

- Providing services and equipment to producers

- Transporting oil around the world

Each of the names below represents one of those exposure types, with a different risk profile when crude rises.

1. Exxon Mobil (NYSE: XOM)

Over the past six months, Exxon Mobil has outperformed Brent crude, with its share price up nearly 35% compared with about 30% for Brent. As of 11 March 2026, both were trading just over 3% below their all-time highs, while Exxon remained closer to its 52-week high.

Exxon Mobil is one of the world's largest integrated oil companies, with exposure spanning exploration, production, refining and chemicals. When oil prices rise, its upstream business may benefit from wider margins, while its scale and diversification can help cushion weaker parts of the cycle.

Exxon Mobil (XOM) vs. Brent Crude 6-month performance

Analyst consensus: Buy

According to TradingView data, analyst sentiment towards Exxon is broadly positive. Of the 31 analysts tracked, 15 rate the stock Strong Buy or Buy, 13 rate it Hold, 1 rates it Sell and 2 rate it Strong Sell.

That positive view is linked to Exxon's balance sheet strength and higher-margin production. The most optimistic analysts project a 1-year price target as high as US$183.00. The average price target is US$145.00, which sits about 3.6% below the current trading price.

2. Chevron (NYSE: CVX)

Chevron is another global integrated major that has benefited from the recent move higher in crude, with its shares trading near 52-week highs. Like Exxon, Chevron operates across the value chain, including upstream production, refining and marketing.

Chevron's completed acquisition of Hess adds Guyana and other upstream assets, which some analysts see as supportive over time. That said, the earnings impact remains subject to integration, project execution and commodity price risks.

Exxon Mobil vs Chevron performance, 6-month chart

Analyst consensus: Buy

Chevron is viewed similarly to Exxon, with broker sentiment remaining broadly constructive. Recent TradingView aggregates show 30 analysts covering the stock over the past three months, with 17 rating it Strong Buy or Buy, 11 at Hold, 1 at Sell and 1 at Strong Sell.

Analysts have highlighted Chevron's diversified portfolio and the potential contribution from Hess, although commodity price volatility and execution risk may keep some more cautious.

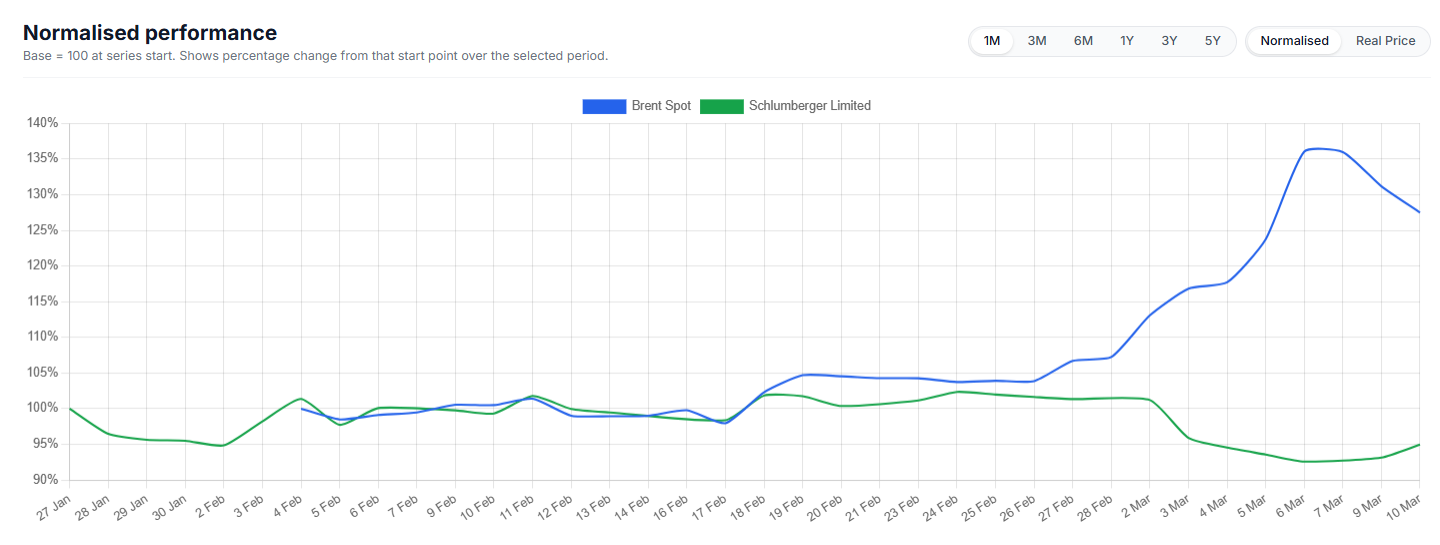

3. SLB (NYSE: SLB)

SLB, previously known as Schlumberger, is one of the world's largest oilfield services and technology providers. It supplies tools, equipment and software that help producers find, drill and complete wells more efficiently.

Over the past six months, SLB has lagged Brent crude, with the share price trading in a choppier range and remaining below its recent peak. That suggests the stronger oil backdrop has not been fully reflected in the share price.

That pattern is not unusual for oilfield services companies, where customer spending decisions often follow moves in the underlying commodity rather than move in lockstep with them. Any future re-rating would depend on factors including producer capital spending, contract timing, service pricing, offshore activity and broader market conditions. A firmer oil price should not be assumed to translate automatically into a firmer SLB share price.

SLB vs Brent crude, 6-month normalised performance

Consensus: Buy

According to TradingView data, third-party analyst consensus on SLB is Buy. Of the 33 analysts covering the stock, 27 rate it Strong Buy or Buy, 4 rate it Hold and 2 rate it Sell or Strong Sell.

That indicates constructive broker sentiment, although the gap between oil prices and SLB's recent share-price performance suggests investors may still want clearer evidence of improving service demand and pricing before the stock fully reflects the stronger commodity backdrop.

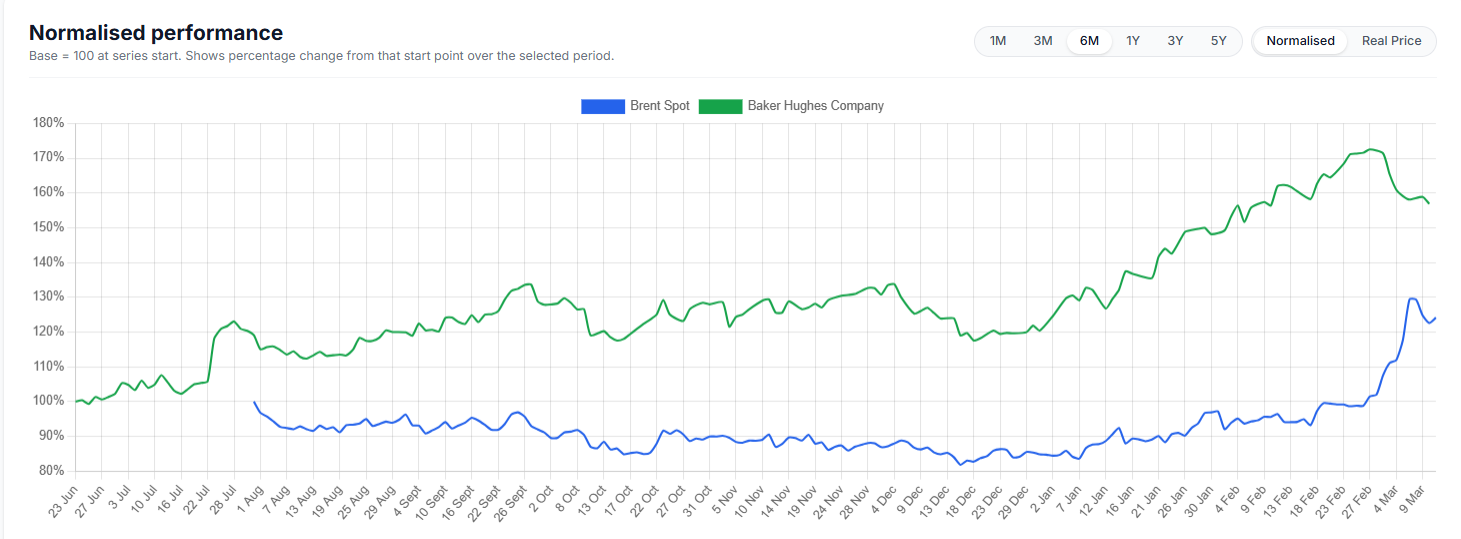

4. Baker Hughes (NASDAQ: BKR)

Baker Hughes is another major oilfield services and equipment provider, with additional exposure to industrial segments such as LNG and power infrastructure. Even when oil prices are not at extreme highs, advances in drilling technology and lower break-even costs have helped keep many shale plays profitable, supporting demand for its services.

The company has also been described as well positioned because of its balance sheet and its exposure to ongoing exploration and production activity. In a period of higher, or even stable-to-firm, oil prices, that mix of services and energy technology may create several revenue drivers.

Over the past six months, Baker Hughes has materially outperformed Brent crude on a normalised basis. Brent traded in a much tighter range for most of the period before moving higher late, while BKR climbed more steadily and reached a significantly stronger cumulative gain. That suggests BKR's share price benefited not only from the backdrop in oil, but also from company-specific optimism and broader support for oilfield services and energy technology names.

BKR vs Brent crude, 6-month normalised performance

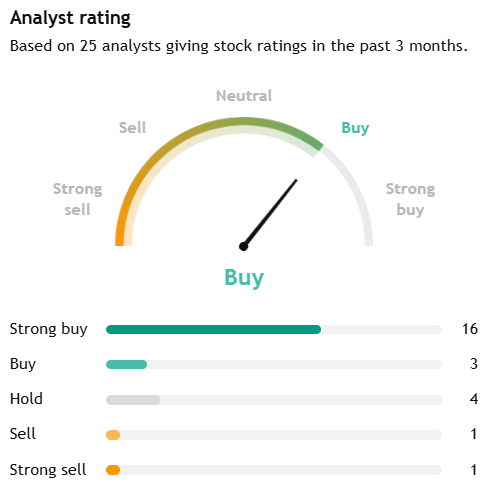

Analyst consensus: Buy

According to TradingView data, Baker Hughes is categorised as Strong Buy. Based on 25 analysts who provided ratings over the past three months, 16 rated the stock Strong Buy, 3 rated it Buy, 4 rated it Hold, 1 rated it Sell and 1 rated it Strong Sell.

Overall, broker sentiment towards Baker Hughes is broadly positive, with more than three quarters of covering analysts rating the stock either Strong Buy or Buy, while most of the remainder were at Hold. That supportive analyst view appears to reflect BKR's exposure to both traditional oilfield services and broader energy and industrial technology markets, including LNG infrastructure.

5. Woodside Energy (ASX: WDS)

Woodside Energy gives the list an Australia-based producer with significant exposure to LNG and oil markets. Its earnings are closely tied to realised commodity prices, which makes the stock sensitive to shifts in crude and gas pricing, as well as broader global energy demand.

Compared with some of the larger US energy names, broker sentiment towards Woodside appears more measured. Investors are balancing the company's global LNG exposure and leverage to stronger energy prices against softer recent realised prices, project and execution risks, and longer-term regulatory and decarbonisation pressures.

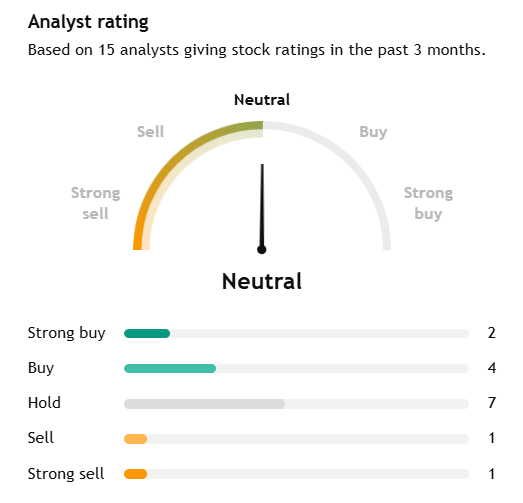

Analyst consensus: Hold

According to TradingView data, Woodside is rated Neutral/Hold. Of 15 analysts, 2 rate it Strong Buy, 4 rate it Buy, 7 rate it Hold, 1 rates it Sell and 1 rates it Strong Sell.

The average 12-month price target is A$29.20 versus a current price of about A$30.28, implying downside of roughly 3.6%. Relative to the larger US energy names in this list, that points to a more cautious broker view.

6. Global oil tanker operators

Oil tanker companies can benefit when firmer oil prices, OPEC+ policy shifts and geopolitical tension increase long-distance shipments and disrupt usual trade routes. When oil volumes travel further, 'tonne-mile' demand can support tanker day rates and profitability even when the broader energy market is volatile.

Analyst consensus: N/A

This is a broader industry category rather than a single publicly traded stock, so there is no single broker consensus to cite. Analyst views would need to be assessed at the company level, such as Frontline plc (FRO), Euronav (EURN) or Scorpio Tankers (STNG).

More broadly, the sector is cyclical. Any benefit from tighter shipping markets can reverse if routes normalise, freight rates fall or supply increases.

Risks and constraints

Higher oil prices do not remove risk for these names.

- If prices rise too far, too fast, demand destruction and policy responses can weigh on future earnings.

- Political decisions from OPEC+ or other major producers can reverse a rally by increasing supply.

- Services and tanker companies are highly cyclical. When the cycle turns, pricing power can fade quickly.

- Company-specific issues, including project execution, realised pricing and capital spending, still matter.

Taken together, these names may benefit from firmer oil prices, but they also carry sector-specific, geopolitical and company-level risks that deserve close attention.

Key market observations

- Woodside provides LNG and oil exposure, although current broker sentiment is more neutral than for the larger US names.

- Tanker operators may benefit when freight markets tighten, though that trade remains highly cyclical and route-dependent.

- SLB and Baker Hughes may benefit if firmer oil prices translate into more drilling and completion activity, but the share-price response has been mixed.

- Exxon Mobil and Chevron offer direct exposure to stronger upstream margins, supported by diversified operations.

References in this article to Exxon Mobil, Chevron, SLB, Baker Hughes, Woodside, tanker operators, analyst consensus ratings and price targets are included for general market commentary only and do not constitute a recommendation or offer in relation to any financial product or security. Third-party data, including consensus ratings and target prices, may change without notice and should not be relied on in isolation. Energy and shipping exposures are cyclical and can be materially affected by commodity price volatility, realised pricing, production changes, project execution, geopolitical disruptions, freight market conditions, regulatory developments and shifts in investor sentiment. Any views about potential beneficiaries of higher oil prices are subject to significant uncertainty.

US inflation data on Wednesday is the week's centrepiece, but with oil nearing seven-month highs, Bitcoin (BTC) sentiment shifting, and the Australian dollar at three-year highs, traders have plenty to navigate in the week ahead.

Quick Facts

- US inflation rate (February) is the key binary event for rate cut pricing and equity direction.

- Brent crude is trading around US$82–84/bbl, near seven-month highs, with a $4–$10 geopolitical risk premium baked in from Iran/Hormuz tensions.

- Bitcoin is trading above US$70,000 as of 6 March, a potential trend change if it holds through the week.

United States: inflation in focus

Last month’s US inflation reading showed prices rising 2.4% year-on-year, still well above the Fed's 2% target.

February's inflation rate, due Wednesday, will be scrutinised for signs that tariff pass-through or rising energy costs are pushing prices back up, or whether the slow grind lower is still intact.

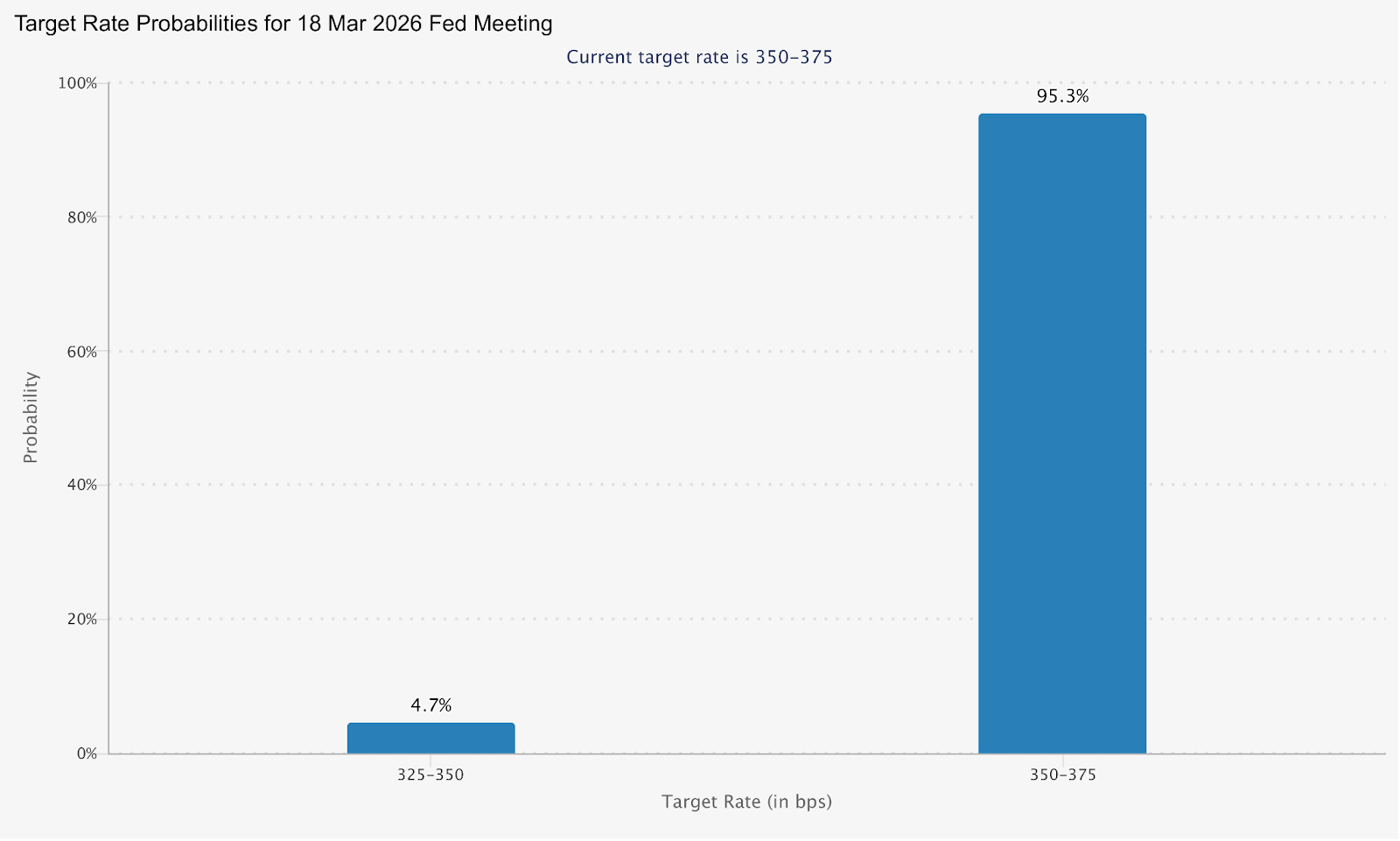

The March FOMC meeting on 17–18 March is now priced at only an 4.7% probability of a cut. A higher-than-expected inflation print this week could potentially push rate cut expectations further out.

A softer read opens the door to renewed cut pricing and potential relief across risk assets.

Key Dates

- US Inflation Rate (February CPI): Wednesday 11 March, 12:30 am (AEDT)

Monitor

- Core vs. headline inflation divergence as evidence of tariff pass-through in goods prices.

- 2-year and 10-year treasury yield sensitivity to the print.

- USD direction and FedWatch repricing in the lead up to the 18 March FOMC decision.

Oil: elevated and event-sensitive

Brent is currently trading around US$83–85 per barrel, with a 52-week range spanning $58.40 to $85.12, reflecting the dramatic move triggered by the Middle East conflict.

Analysts estimate the geopolitical risk premium already baked into oil at US$4–$10 per barrel, and average 2026 Brent forecasts have been lifted to US$63.85/bbl, up from US$62.02 in January.

The EIA's Short-Term Energy Outlook forecasts Brent to average $58/bbl in 2026, well below the current spot price.

The gap between spot and the forecast baseline could be a useful frame for traders this week: any de-escalation signal from the Middle East could rapidly close that gap.

Monitor

- Strait of Hormuz developments and any diplomatic signals from Iran nuclear talks.

- EIA weekly oil inventory data.

- Oil's knock-on to inflation expectations and whether it shifts central bank posture.

- Energy sector equity performance relative to the broader market.

Bitcoin: sentiment watch

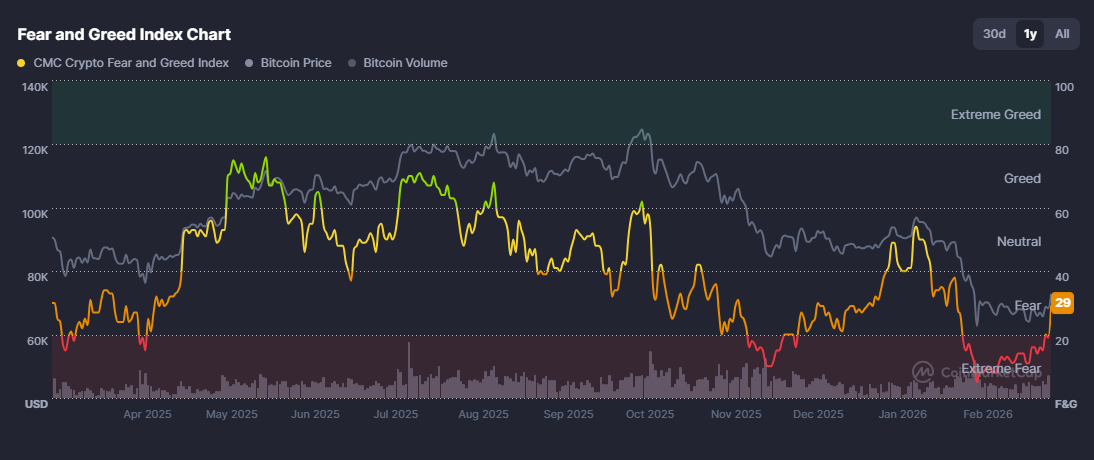

BTC has been attempting to stabilise after a brutal 53% correction over the past 17 weeks, fuelled by escalating geopolitical tensions and renewed tariff concerns.

However, yesterday saw a 8% jump back above $72,000, and the crypto “fear and greed index” jumped up to 29 (fear), up from below 20 (extreme fear), where it has been sitting for over a month, indicating a potential sentiment shift.

A cooler-than-expected US inflation print on Wednesday could provide further fuel for the breakout; a hot print risks potentially pulling BTC back below the US$70,000 level it has just reclaimed.

Monitor

- Inflation print reaction on Wednesday as the primary macro catalyst for the move.

- Any rotation into altcoins following BTC strength.

- ETF inflow/outflow data as confirmation of institutional participation.

AUD/USD: Hawkish RBA meets geopolitical crosswinds

The Aussie is trading near more than three-year highs and heading for its fourth consecutive monthly gain, up more than 6% year-to-date, making it the top-performing G10 currency in 2026.

The driver is a clear policy divergence. RBA Governor Michele Bullock signalled the March policy meeting is "live" for a possible rate increase, and warned that an oil price shock from Iran tensions could reignite domestic inflationary pressures.

Market pricing now suggests around a 28% chance of a 25bp hike at the upcoming meeting, while fully pricing in tightening through May, and around a 75% chance of another increase to 4.35% by year-end.

This hawkish read, set against a Fed on hold and facing dovish political pressure, creates a potential structural tailwind for the Aussie.

Monitor

- AUD/USD reaction to Wednesday's US inflation data.

- RBA rate hike probability repricing through the week.

- Iron ore and commodity prices as secondary AUD drivers.

- China demand signals, given Australia's export exposure.

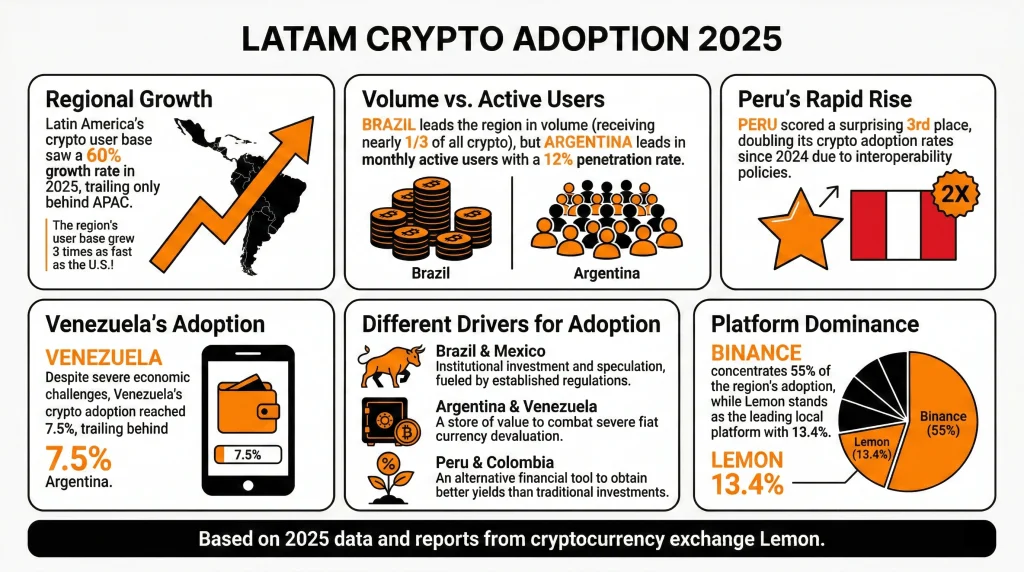

Latin America (LATAM) saw over $730 billion in crypto volume in 2025, a 60% year-on-year surge that made the region responsible for roughly 10% of global crypto activity.

In 2026, institutional players are starting to take the region seriously, regulation is crystallising, and the structural drivers from 2025 show no sign of fading. But the region is not a single story, and 2026 will test whether the current momentum is built on solid fundamentals or speculative optimism.

Quick facts

- LATAM monthly active crypto users grew 18% year-on-year (YoY), three times faster than the US.

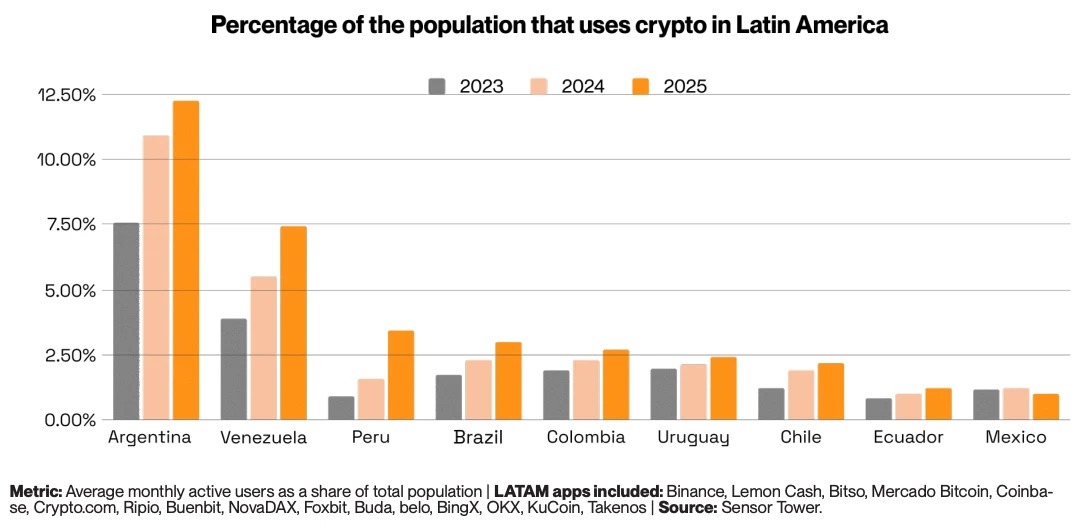

- Argentina reached 12% monthly active user penetration, accounting for over a quarter of the region's crypto activity.

- Over 90% of Brazilian crypto flows are now stablecoin-related.

- Three LATAM countries rank in the global top 20: Brazil (5th), Venezuela (18th), Argentina (20th).

- Peru's crypto app downloads grew 50% in 2025, with 2.9 million downloads.

From survival tool to financial infrastructure

Latin America did not embrace cryptocurrency because of speculation. It embraced it because traditional financial systems repeatedly failed ordinary people. Over the past 15 years, average annual inflation across the region's five largest economies ran at 13%, compared to just 2.3% in the US over the same period.

In Venezuela, it reached 65,000% in a single year. In Argentina, it exceeded 220% in 2024. For millions of people, holding savings in local currency was a slow act of self-destruction. Stablecoins became the natural response. Digital assets pegged to the US dollar offered a reliable store of value, borderless transferability, and access without a bank account.

Unlike in the West, where crypto is seen more as a speculative instrument, in LATAM it has become a necessary financial tool. However, adoption drivers are not entirely uniform across the region. Brazil and Mexico are institutional stories, driven by regulated market participation and established financial players.

Argentina and Venezuela remain store-of-value plays, with crypto serving as a direct hedge against fiat collapse. And Peru and Colombia are more yield-seeking markets, where crypto offers returns that traditional savings accounts cannot match.

How fast is LATAM adopting crypto?

LATAM’s on-chain crypto volume rose 60% year-on-year in 2025. The region has recorded nearly $1.5 trillion in cumulative volume since mid-2022, peaking at a record $87.7 billion in a single month in December 2024.

Monthly active crypto users across LATAM also grew 18% in 2025, three times faster than the US.

Stablecoins are the primary vehicle driving this adoption. Of the $730 billion received in 2025, $324 billion moved through stablecoin transactions, an 89% year-on-year surge. In Brazil, over 90% of all crypto flows are stablecoin-related, and in Argentina, stablecoins account for over 60% of activity.

Looking ahead, the Latin America cryptocurrency market is forecast to reach $442.6 billion by 2033, growing at a compound annual rate of 10.93% from 2025, according to IMARC Group.

For traders, the speed of adoption matters less as a headline than what is driving it: a region of 650 million people building parallel financial infrastructure in real time, with stablecoins as the foundation.

The institutional turn

For most of LATAM’s crypto history, adoption was bottom-up. Unbanked or underbanked retail users drove volumes through local exchanges. That picture is now changing at the top end of the market.

In February 2026, Crypto Finance Group, part of the leading global exchange operator Deutsche Börse Group, announced its expansion into Latin America, targeting banks, asset managers, and financial intermediaries seeking institutional-grade custody and trading infrastructure.

Traditional banks and fintechs are following suit. Nubank now rewards customers for holding USDC. Brazil's B3 exchange approved the world's first spot XRP and SOL ETFs, ahead of the US, in 2025. Centralised exchanges, including Mercado Bitcoin, NovaDAX, and Binance, have collectively listed over 200 new BRL-denominated trading pairs since early 2024.

In March 2025, Brazilian fintech Meliuz became the first publicly traded company in the country to launch a Bitcoin accumulation strategy, now holding 320 BTC.

“Crypto adoption in LatAm is already global-scale. What the market needs now is institutional-grade governance, and that’s exactly why we’re here,” — Stijn Vander Straeten, CEO of Crypto Finance Group

Crypto remittance use case

Latin America receives hundreds of billions of dollars annually from workers abroad, making remittances one of the most concrete and measurable crypto use cases in the region. Traditional transfer services charge an average of 6.2% per transaction. On a US$300 transfer, that is roughly US$20 in fees.

Blockchain-based infrastructure more broadly offers dramatic fee reductions. Bitcoin brings costs to around US$3.12 per US$100 transferred. While cheaper alternatives like XRP or Ethereum layer-2 infrastructure can reduce that to less than US$0.01.

For a migrant worker sending US$1,500 home to Peru, switching from a legacy bank saves more than the average Peruvian weekly wage in fees alone.

LATAM’s crypto regulatory environment

The variable that will most determine whether LATAM lives up to its 2026 potential is crypto regulation. And here, the picture is genuinely mixed.

Brazil leads the region with its Virtual Assets Law, which covers asset segregation, VASP licensing, AML/KYC requirements, and capital standards. It also implemented the Travel Rule for domestic VASP transfers, which came into force in February 2026. However, some more controversial proposals, including a US$100,000 cap on cross-border stablecoin transactions and a ban on self-custody wallet transfers, remain under active consultation.

Mexico's 2018 Fintech Law remains one of the world's earliest formal recognitions of virtual assets. Chile's 2023 Fintech Law established licences for exchanges, wallets, and stablecoin issuers, formally recognising digital assets as 'digital money.'

Bolivia reversed a decade-long crypto ban in June 2024 by authorising regulated digital asset transactions. Argentina introduced mandatory exchange registration in 2025. And El Salvador continues to expand tokenised economic initiatives despite removing Bitcoin's legal tender status.

Ten countries across the region now have formal crypto frameworks of some kind. But for traders, regulatory divergence remains a live risk, and given Brazil receiving nearly one-third of all LATAM crypto volume, any significant policy reversal there could have outsized consequences.

What traders should watch

Brazil's institutional momentum is the most significant structural trend. With $318.8 billion in on-chain volume in 2025, Brazil effectively is the LATAM market.

The outcome of the Brazil stablecoin consultation could have a big influence. A restriction on foreign stablecoins in domestic payments would directly impact the most traded asset class in the region's dominant market.

Argentina is the volatility play. Monthly active user penetration of 12% and 5.4 million crypto app downloads in 2025 signal deep and growing retail engagement.

Colombia is an early-warning market to watch. The peso's 5.3% depreciation in 2025 and deepening fiscal crisis are driving stablecoin inflows in a pattern that mirrors Argentina's trajectory in earlier years. If Colombia's macro situation deteriorates further, crypto adoption could accelerate.

There is also an exchange concentration risk at play. Binance crypto exchange is the primary exchange for over 50% of LATAM crypto users. If the exchange faces any regulatory action, operational disruption, or competitive shock, it could have an outsized market impact.

Bottom line

Latin America's crypto market has entered a new phase. The structural drivers that caused initial crypto-demand in the region have not gone away: inflation, remittances, financial exclusion, and currency instability are all still at play.

What has changed is the layer being built on top of them. Institutional infrastructure, regulatory frameworks, corporate treasury adoption, and global exchange capital flowing into a region that was, until recently, largely self-contained.

Brazil's near-250% volume growth in 2025 and its position receiving nearly one-third of all LATAM crypto are the defining market developments. Its regulatory trajectory, stablecoin policy decisions, and ETF pipeline will effectively set the tone for the region in 2026.

For traders, the headline growth figures are real, but so are the concentration risks, regulatory uncertainties, and country-level divergences that sit beneath them.