Go further with GO Markets

Trade smarter with a trusted global broker. Low spreads, fast execution, powerful platforms, and award-winning customer support.

20 Years Strong

Celebrating 20 years of trading excellence.

Built for traders since 2006.

For beginners

Just getting

started?

Explore the basics and build your confidence.

For intermediate traders

Take your

strategy further

Access advanced tools for deeper insights than ever before.

Professionals

For professional

traders

Discover our dedicated offering for professionals and sophisticated investors.

Get more out of every trade

Explore our limited-time special offers

Get Started with GO Markets

Whether you’re new to markets or trading full time, GO Markets has an

account tailored to your needs.

Trusted by traders worldwide

Since 2006, GO Markets has helped hundreds of thousands of traders to pursue their trading goals with confidence and precision, supported by robust regulation, client-first service, and award-winning education.

*Trustpilot reviews are provided for the GO Markets group of companies and not exclusively for GO Markets Ltd.

*Awards were awarded to GO Markets group of companies and not exclusively to GO Markets Ltd.

Explore more from GO Markets

CFD markets

Trade CFDs across forex, indices, shares, commodities, metals, ETFs and more.

Platforms & tools

Trading accounts with seamless technology, award-winning client support, and easy access to flexible funding options.

Academy

Learn the skills, strategies, and mindset behind long-term trading success.

Accounts & pricing

Compare account types, view spreads, and choose the option that fits your goals.

Go further with

GO Markets.

Explore thousands of tradable opportunities with institutional-grade tools, seamless execution, and award winning support. Opening an account is quick and easy.

News & insights

Powerful tools for every trading style and preference.

Last week was as consequential as advertised. The RBA hiked, the Fed held, and markets barely had time to process any of it before reports emerged that Israel had struck Iran's South Pars gas field.

The week ahead brings fewer central bank decisions, but it may be just as important for markets. Flash PMIs will offer the first broad read on whether the war is already showing up in business confidence. Australia's February CPI is the domestic data point that matters most for the RBA's next move. And the oil market remains the dominant macro variable.

Quick facts

- Brent crude spiked above $110 per barrel after Israel struck Iran's South Pars gas field for the first time.

- Flash PMIs for Australia, Japan, the eurozone, UK, and the US all land Tuesday.

- Australia's February CPI lands Wednesday, the first inflation read since the back-to-back RBA hikes.

Oil: From crisis to emergency

The oil situation deteriorated significantly last week. Brent crude has now surged roughly 80% since the war began on 28 February.

The 18 March strike on Iran's South Pars gas field was the first time upstream oil and gas infrastructure has been targeted.

Iran responded to the strike by threatening to target facilities across Saudi Arabia, the UAE and Qatar. If any of these threats are executed, the global oil shock would escalate from a supply disruption to a direct attack on the region's production capacity.

Analysts are now saying $150 Brent is achievable and $200 is not outside the realm of possibility. The 1970s Arab oil embargo resulted in a quadrupling of prices, and the current shock is already being described in those terms by senior energy executives.

For markets this week, oil is the dominant variable. Any signal of ceasefire, diplomatic progress or resumed Hormuz shipping could likely trigger a correction in oil prices. Any Iranian strike on Gulf infrastructure could send them higher.

Monitor

- Daily vessel transit numbers through the Strait of Hormuz.

- Iranian retaliation against Gulf infrastructure, a strike on Saudi or UAE facilities would be a major escalation.

- When and how American and European IEA reserves reach the market.

- Qatar's South Pars disruption is affecting the European LNG market.

- Trump statements that could cause intraday oil price movement.

Global Flash PMIs: The first read on an economy at war

Tuesday delivers the S&P Global flash PMI estimates for March across every major economy simultaneously.

This will be the first data set to capture how manufacturers and services firms are responding to $100+ oil, the Strait of Hormuz blockade, and the broader uncertainty created by the war in the Middle East.

The key question for each economy is whether the oil price surge and war uncertainty have dented business confidence, suppressed new orders or pushed input price indices to new multi-year highs.

Given that oil crossed $100 before the survey window closed for most economies, input cost readings could be significantly elevated.

Key dates

- S&P Global Flash Australia PMI: Tuesday 24 March, 9:00 am AEDT

- S&P Global Flash Japan PMI: Tuesday 24 March, 11:30 am AEDT

- HSBC Flash India PMI: Tuesday 24 March, 4:00 pm AEDT

- HCOB Flash France PMI: Tuesday 24 March, 7:15 pm AEDT

- HCOB Flash Germany PMI: Tuesday 24 March, 7:30 pm AEDT

- HCOB Flash Eurozone PMI: Tuesday 24 March, 8:00 pm AEDT

- S&P Global Flash UK PMI: Tuesday 24 March, 8:30 pm AEDT

- S&P Global Flash US PMI: Wednesday 25 March, 12:45 am AEDT

Monitor

- Input price components for any multi-year highs across manufacturing and services.

- Business confidence indices for how much the war shock has dented forward expectations.

- New orders as an indicator for future output; a sharp fall could signal demand destruction is underway.

- US composite PMI: already the weakest of major economies in February, another soft reading could raise growth alarm bells.

Hormuz crisis explained

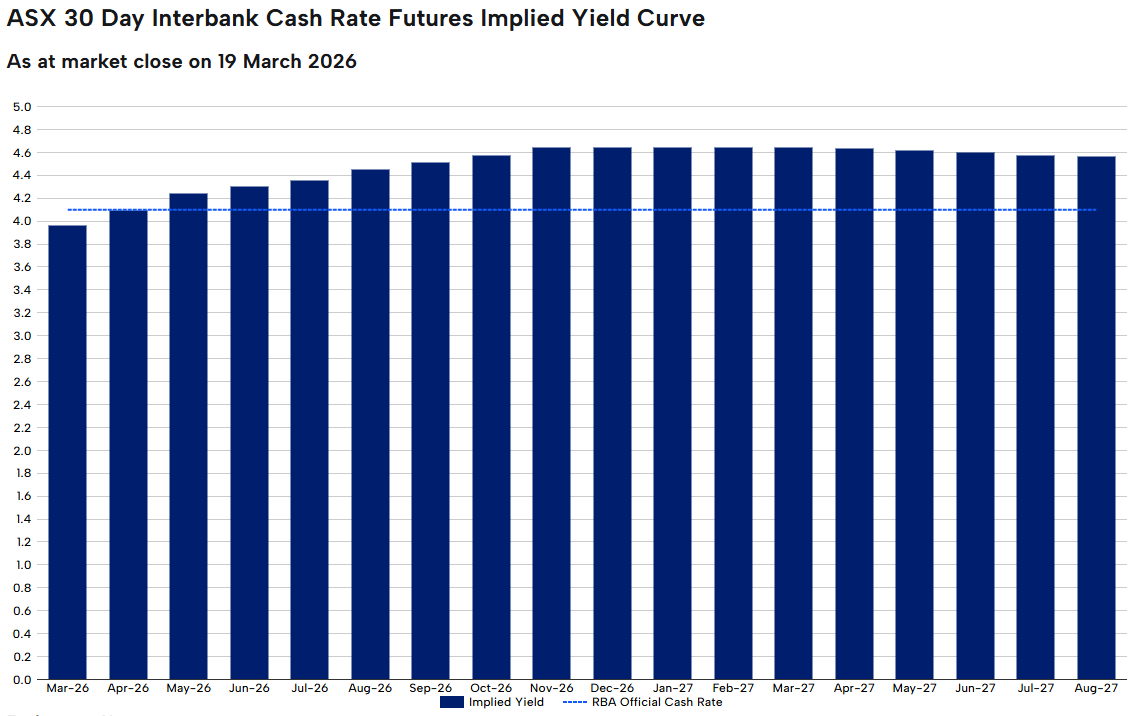

Australia: Is another hike coming?

The RBA hiked for the second meeting in a row on 17 March, lifting the cash rate to 4.10% in a narrow 5-4 vote.

Governor Bullock described it as a "very active discussion" where the direction of policy was not in question, only the timing.

This week will see the release of February's CPI as the first read to capture any of the oil shock. The trimmed mean, which strips out volatile items including fuel, will be the number the RBA watches most closely. A reading above 3.5% could cement the case for a May hike. A softer result could revive the argument for a pause.

ANZ and NAB have both stated expectations of a third hike in May, taking the cash rate to 4.35%.

Key dates

- ABS Consumer Price Index (CPI): Wednesday 25 March, 11:30 am AEDT

Monitor

- Trimmed mean inflation as the RBA's preferred measure.

- Fuel and energy components that could separate the oil shock from domestic price pressure.

- Housing and services inflation as sticky components driving the RBA's long-run concern.

Ready to trade beyond the majors?

Open an account · Log in

Asia dominates the global semiconductor supply. Five companies, spanning Taiwan, South Korea, and Japan, sit at the critical juncture of the AI buildout, controlling everything from fabrication to the equipment that makes chips possible.

Quick facts

- TSMC delivered $90 billion in revenue in 2024, with a 59% gross margin and shares up 55% in 2025.

- Advantest shares doubled (+102%) in 2025 as AI-driven chip testing demand surged.

- SK Hynix is Nvidia's primary HBM supplier, positioning it at the centre of the AI accelerator boom.

1. Taiwan Semiconductor Manufacturing Co. (TSM)

TSMC is the world's largest contract chip manufacturer, producing advanced semiconductors for Apple, Nvidia, AMD, and Qualcomm. As a pure-play foundry, it leads in 5-nanometer (5nm) and 3- nanometer (3nm) chip production, with smaller nodes in development.

The company posted $90 billion in revenue for 2024 with a 59% gross margin and 36% return on equity.

Shares delivered a total return of 55% in 2025, with analysts forecasting a further ~30% revenue increase in 2026, underpinned by its $100 billion US expansion programme.

The key risk for the company is its geopolitical exposure, with Taiwan Strait tensions remaining the sector's most-watched tail risk.

What to watch

- US expansion progress: Any delays, cost blowouts, or political friction concerning TSMC's $100 billion Arizona investment could weigh on sentiment.

- Customer order visibility: Watch for any guidance updates from Apple, Nvidia, or AMD on chip orders, as TSMC's revenue is highly concentrated among a handful of clients.

- Geopolitical developments: Any escalation of Taiwan Strait tensions could trigger sharp moves regardless of fundamentals.

- Next-node ramp: Progress on 2nm production and yield rates will be a key signal for TSMC's ability to maintain its technology lead.

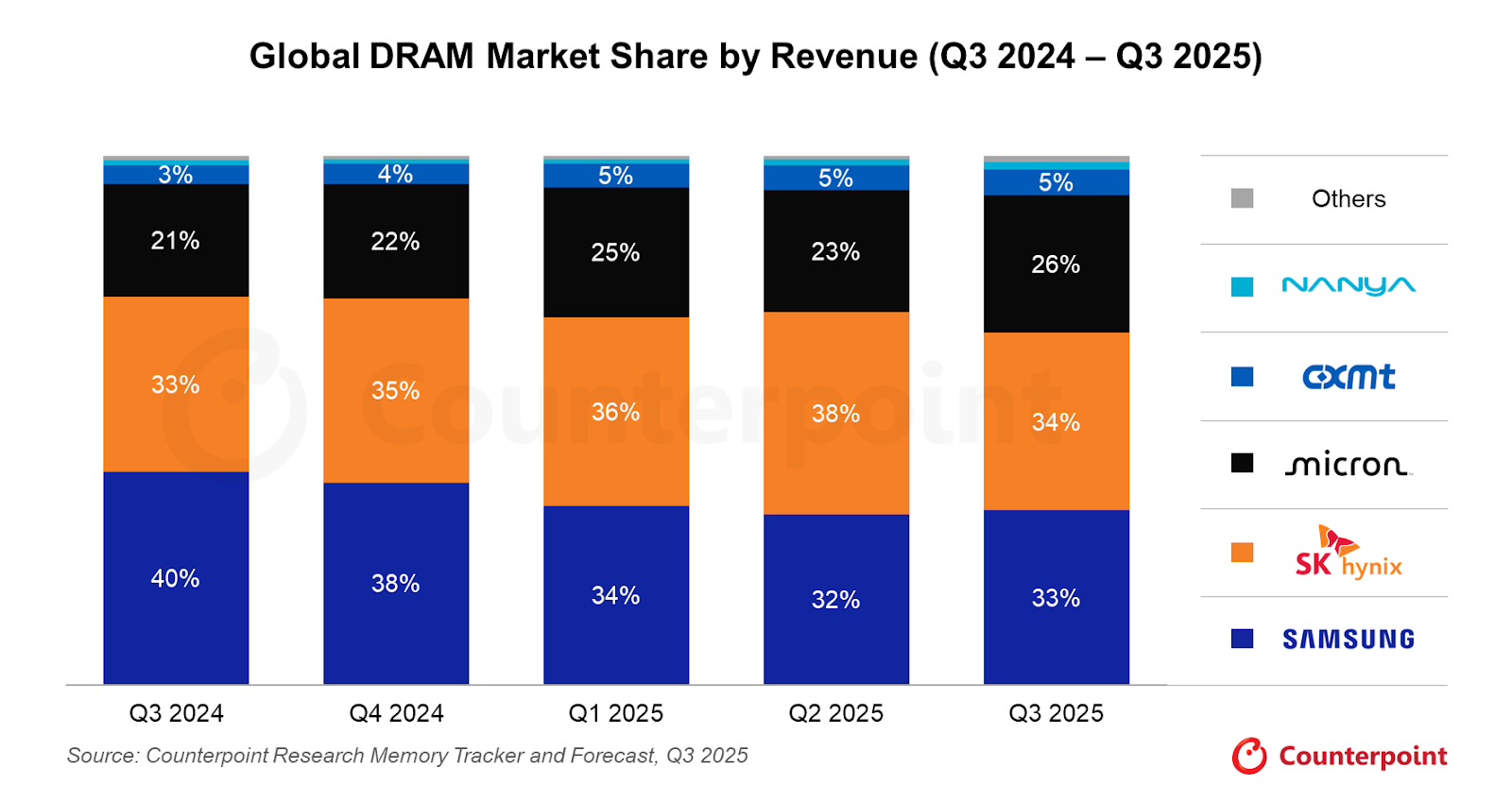

2. Samsung Electronics (KR:005930)

Samsung is one of the few companies globally that both designs and fabricates chips at scale. It competes across DRAM, NAND flash, and logic chip segments, and remains a core supplier to global tech giants.

Samsung's wide scope is a strength, but also a complexity. Its memory division faces margin pressure from inventory cycles, while its foundry business continues to lag TSMC in leading-edge yields.

The AI-driven memory boom may provide a tailwind, though execution in HBM production has been slower than local rival SK Hynix.

What to watch

- HBM qualification progress: Samsung has been working to qualify its HBM3E chips with Nvidia. Any confirmation of a major supply win could be a meaningful catalyst.

- Memory pricing trends: DRAM and NAND spot prices could be an indicator of Samsung's margin trajectory.

- Foundry yield improvements: Samsung's logic foundry business has struggled with yields at advanced nodes; any credible progress here could re-rate the division.

- Management guidance: Following a period of earnings volatility, clarity on capex plans and divisional targets at upcoming results will be closely watched.

3. Advantest (ATEYY)

Tokyo-based Advantest makes testing equipment used to verify chips meet performance and quality standards.

It supplies to Samsung, Intel, Nvidia, Qualcomm, and Texas Instruments, allowing it to benefit from chip industry growth broadly, regardless of which foundry wins market share.

Advantest shares doubled in 2025 (+102%), and it raised its sales forecast by 21.8% and earnings forecast by 70.6% for the year ending March 2026.

What to watch

- Order backlog updates: Any contraction in Advantest's backlog could be an early warning sign after the strong 2025 run.

- AI chip testing demand: As chips grow more complex, testing time per chip increases. Monitor whether AI accelerator volumes from TSMC and Samsung start to drive outsized testing demand.

- FY2026 guidance: The next forecast update will be critical in confirming whether 2025's upgrade cycle has further to run.

4. Tokyo Electron (T:8035)

Tokyo Electron is among the world's largest suppliers of semiconductor production equipment, specialising in deposition, etching, and cleaning tools.

Every major chipmaker, including TSMC, Samsung, and SK Hynix, depends on TEL's systems to scale production.

As chipmakers invest billions to expand capacity, TEL's order book grows. The risk lies in potential US export restrictions on advanced equipment sales to China, which remains one of the primary revenue segments for the company.

What to watch

- US export control policy: China accounts for a significant portion of TEL's revenue. Any tightening of equipment export rules is the most immediate risk to watch.

- Chipmaker capex announcements: TSMC, Samsung, and SK Hynix's capital expenditure plans for 2026 directly translate into equipment orders. Any cuts could flow through to TEL's order book.

- New tool adoption cycles: Monitor whether TEL's next-generation deposition and etch tools are being adopted at leading-edge fabs.

5. SK Hynix (KR:000660)

SK Hynix is the world's second-largest memory chip maker and has emerged as arguably the clearest AI-era beneficiary in the memory space.

It is Nvidia's primary supplier of High Bandwidth Memory (HBM) chips, the specialised memory used in AI accelerators like the H100 and B200.

HBM demand has driven a dramatic re-rating of SK Hynix's revenue profile and market standing. With AI infrastructure spending showing little sign of slowing heading into 2026, the company's HBM franchise could remain a key differentiator.

However, capacity constraints and the risk of Samsung and Micron closing the HBM gap are the primary concerns to watch.

What to watch

- Nvidia supply relationship: Any shift in Nvidia's supplier mix toward Samsung or Micron could be a key risk event.

- HBM4 development: The race to next-generation HBM is already underway. Watch for updates on SK Hynix's HBM4 readiness and whether it can maintain its lead.

- Conventional memory pricing: SK Hynix still derives meaningful revenue from standard DRAM and NAND. Spot price trends could be a gauge of the broader memory cycle.

Bottom line

TSMC, SK Hynix, Samsung, Advantest, and Tokyo Electron collectively control the chokepoints of the AI buildout.

The expected increase in AI infrastructure may support demand, but investors should weigh the risks carefully.

Geopolitical exposure, US export restrictions, and the pace of HBM competition could all move the needle.

Ready to trade beyond the majors?

Open an account · Log in

So, here’s the thing...

If you have been following the tech story for the last decade, you have been trained to look at a very specific, very small patch of real estate in Northern California. But as we sit here in early 2026, the "connect-the-dots" moment for investors is this: the AI trade has stopped being about shiny software demos in Palo Alto and has started being about the physical industrialisation of compute.

Want to know more? Read our 2026 AI playbook

What changed, and why it matters

We have entered the "Year of Proof". The world’s largest companies, the hyperscalers, are projected to spend a staggering US$650 billion on capital expenditures this year. But here’s the part most people miss: that money is not staying in Silicon Valley. It’s flowing to the "picks and shovels" players in Idaho, Washington, Colorado and even overseas.

If you want to understand where the actual return on investment (ROI) may be landing this earnings season, you have to look outside the 650 area code. The shift from AI hype to AI industrialisation is changing the map.

Five companies · AI infrastructure play · 2026

The full AI stack: from capex to consulting

Infrastructure builders compared to the implementation bridge across the AI value chain

Hyperscaler CapEx: Early 2026 analyst estimates, midpoint of ranges. Amazon approx. 100% YoY, Alphabet approx. 100%, Meta approx. 87%, Microsoft approx. 50%.

Accenture: Cumulative advanced AI bookings $11.5B through Q1 FY2026. Q1 AI bookings $2.2B (up 76% YoY), AI revenue $1.1B (up 120% YoY) across 1,300+ clients.

Five companies shaping the next phase of AI

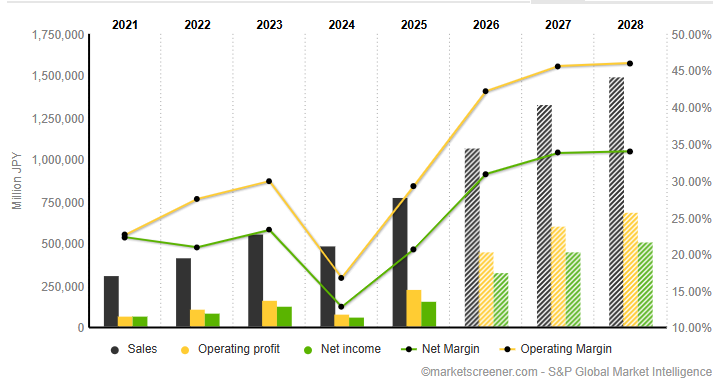

Micron Technology (MU), Boise, Idaho

Micron is the "memory backbone" of the current cycle. While everyone was watching the chip designers, many overlooked the fact that AI chips are far less useful without high-bandwidth memory (HBM). Micron is currently viewed by some analysts as a strong buy because its capacity is reportedly sold out through the end of 2026. Analysts are also eyeing a 457% jump in earnings per share (EPS) as the memory cycle reaches what some describe as a robust peak.

Microsoft (MSFT), Redmond, Washington

Microsoft is the enterprise backbone of this transition. It has moved beyond simple chatbots and is now building what analysts call "Intelligence Factories". While the stock has faced pressure recently over capacity constraints, underlying demand for Azure AI is reportedly still running ahead of capacity. The broader bull case is that Microsoft is moving into "Agentic AI", systems that do not just talk to users but may also execute multi-step business workflows.

Which Asian companies are betting big on artificial intelligence?

Amazon (AMZN), Seattle, Washington

Amazon is playing a long-term game of vertical integration. To reduce its reliance on expensive third-party hardware, it’s building its own AI chips in-house. Amazon Web Services (AWS) remains the primary driver of profitability, and the company is using its retail data to train specialised models that many Silicon Valley start-ups may struggle to replicate.

Palantir Technologies (PLTR), Denver, Colorado

If Micron provides the memory and Microsoft the platform, Palantir provides the "operating system" for the modern AI factory. The company has posted strong momentum, with US commercial sales recently growing 93% year over year. It’s often framed as a bridge between raw data and corporate profitability, which remains a key focus for investors in 2026.

Accenture (ACN), Dublin, Ireland

You cannot just "plug in" AI. Businesses often need to redesign processes around it, and that’s where Accenture comes in.

The company is viewed as an implementation bridge, with one analyst arguing that "GenAI needs Accenture" to move from pilot programs to production though the cautionary angle is that the AI story has not fully excited investors here yet because consulting revenue can take longer to show up than chip sales.

What could happen next?

The chart maps the three time horizons likely to shape the next phase of the AI industrialisation trade.

In the near term, markets are still reacting to chipmaker earnings, guidance, and any signs of capacity strain. Over the next month, attention shifts to the real-world inputs behind AI growth, especially power, financing, and infrastructure. By the 60-day window, the key question is whether AI spending is broadening into a wider market re-rating or running ahead of near-term returns.

Across all three periods, the focus is the same: proof. Investors are looking for signs that AI capital expenditure is translating into real demand for energy, land, and industrial capacity. That is why updates from companies tied to power and data centre buildout matter more than ever.

Scenario planning · March 2026

What could happen next

Three time horizons, three scenarios to watch across the AI industrialisation cycle

Chipmaker reports

Possible

Market volatility continues as traders digest the latest reports from chipmakers like Micron

Upside scenario

"Bulletproof" guidance from remaining infrastructure names triggers a sector-wide relief rally

Watch for

Any mention of "capacity constraints" or "supply bottlenecks" in earnings calls

Energy and rates

Possible

Focus shifts to "real economy" energy players like NextEra that power the data centres

Downside scenario

Rising oil prices from Middle East conflict act as a tax on tech margins, rotating into defensives

Action point

Monitor Fed language on rates. Higher for longer makes $650B capex bills far more expensive to finance

The great dispersion

Possible

Market rewards companies with real AI revenue and punishes those still stuck in experimentation

Upside scenario

NextEra Energy (NEE) data centre announcements in late April/May trigger a utility renaissance rally

Downside scenario

An "air pocket" in profits occurs where debt-funded investment outpaces revenue gains

Watch

May reports from Texas Pacific Land (TPL) — is data centre land demand still "red hot"?

Action point

Review your portfolio for geographic diversity. The AI story is now a global power race

The psychological trap

The emotional trap many traders fall into right now is recency bias. You have seen NVIDIA and the "Magnificent 7" win for so long that it feels like they are the only way to play this. But the "obvious" trade is often the one that has already been priced in. Before acting, ask yourself: "Am I buying this stock because I understand its role in the physical AI supply chain, or because I’m afraid of missing the next leg of a rally that started two years ago?"

Ready to trade beyond the majors?

Open an account · Log in

Disclaimer: This content is general information only and should not be relied on as personal financial advice or a recommendation to buy, sell, or hold any financial product. References to companies or themes, including AI-related stocks, are illustrative only. Share and derivative markets can move sharply, and concentrated sectors such as AI and technology may experience elevated volatility, valuation risk, and liquidity risk. If you trade derivatives such as CFDs, leverage can magnify both gains and losses. Past performance is not a reliable indicator of future performance.