Global markets move into the new week with a number of potentially high-impact catalysts. Japan’s general election lands first on Sunday, followed by US inflation and labour market data that continue to shape interest-rate expectations.

- Japan election: Policy continuity and political stability are generally viewed as supportive for regional markets.

- US inflation and labour market: The consumer price index (CPI) and the Employment Situation report (nonfarm payrolls, NFP) are the immediate macro focal points for the week.

- Bitcoin risk gauge: Bitcoin is back near levels last seen in late 2024 and remains well below its October 2025 peak.

- Sector rotation watch: Technology has recently underperformed while value and defensive segments have stabilised, with earnings season continuing to influence flows.

Japan election

The general election in Japan is primarily viewed through the lens of policy certainty. Markets typically favour a clear outcome and continuity in fiscal and monetary settings.

Unexpected results or coalition uncertainty may increase short-term volatility in the JPY and regional indices at the start of the week.

Key dates

- General election (Japan): Sunday, 8 February

- Results through Asian trade on Monday

Market impact

- JPY may be sensitive to results uncertainty or potential changes in policy direction

- Asia equities may see early-week volatility until results are clear

US inflation and labour market

Inflation remains the most direct input into interest-rate expectations, while the monthly NFP report provides a broad read on employment conditions and wage pressures.

Treasury yields and the USD often react quickly to these releases, with knock-on effects across equities, gold and growth assets.

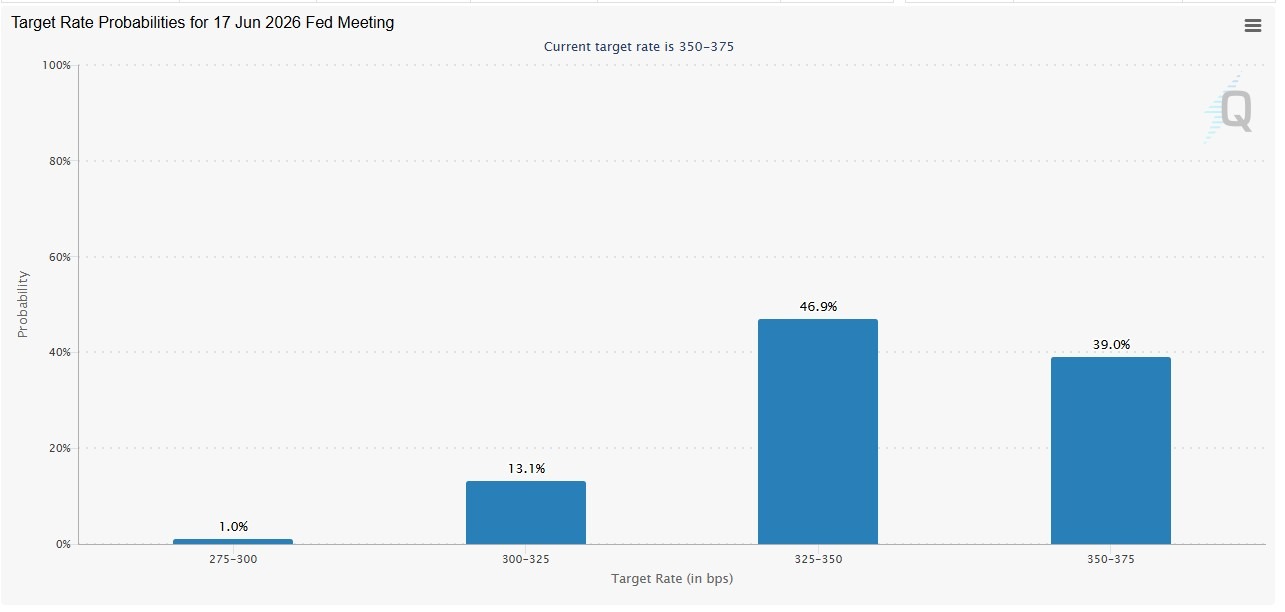

Current pricing indicates markets assign less than a 30% probability of a cut by the April meeting, with June meeting hike probabilities above 50%.

Key dates

- Employment Situation: Wednesday, 11 February 08:30 (ET) | Thursday, 12 February 00:30 (AEDT)

- CPI (January 2026): Friday, 13 February 08:30 (ET) Saturday, 14 February 00:30 (AEDT)

Market impact

- Yields often move first, followed by USD and then risk assets

- Expectations for rate-cut timing may adjust quickly

- Growth and technology shares remain more rate-sensitive

Bitcoin

Bitcoin has declined to levels last seen prior to the US elections in November 2024 and is close to 50% below its October 2025 peak.

While not a traditional macro indicator, crypto markets could be viewed as a real-time read on investor risk tolerance. Sustained weakness can coincide with more cautious positioning across higher-beta assets, including technology shares.

Market impact

- Softer crypto sentiment may coincide with reduced speculative flows

- Risk appetite may remain more selective

Sector rotation

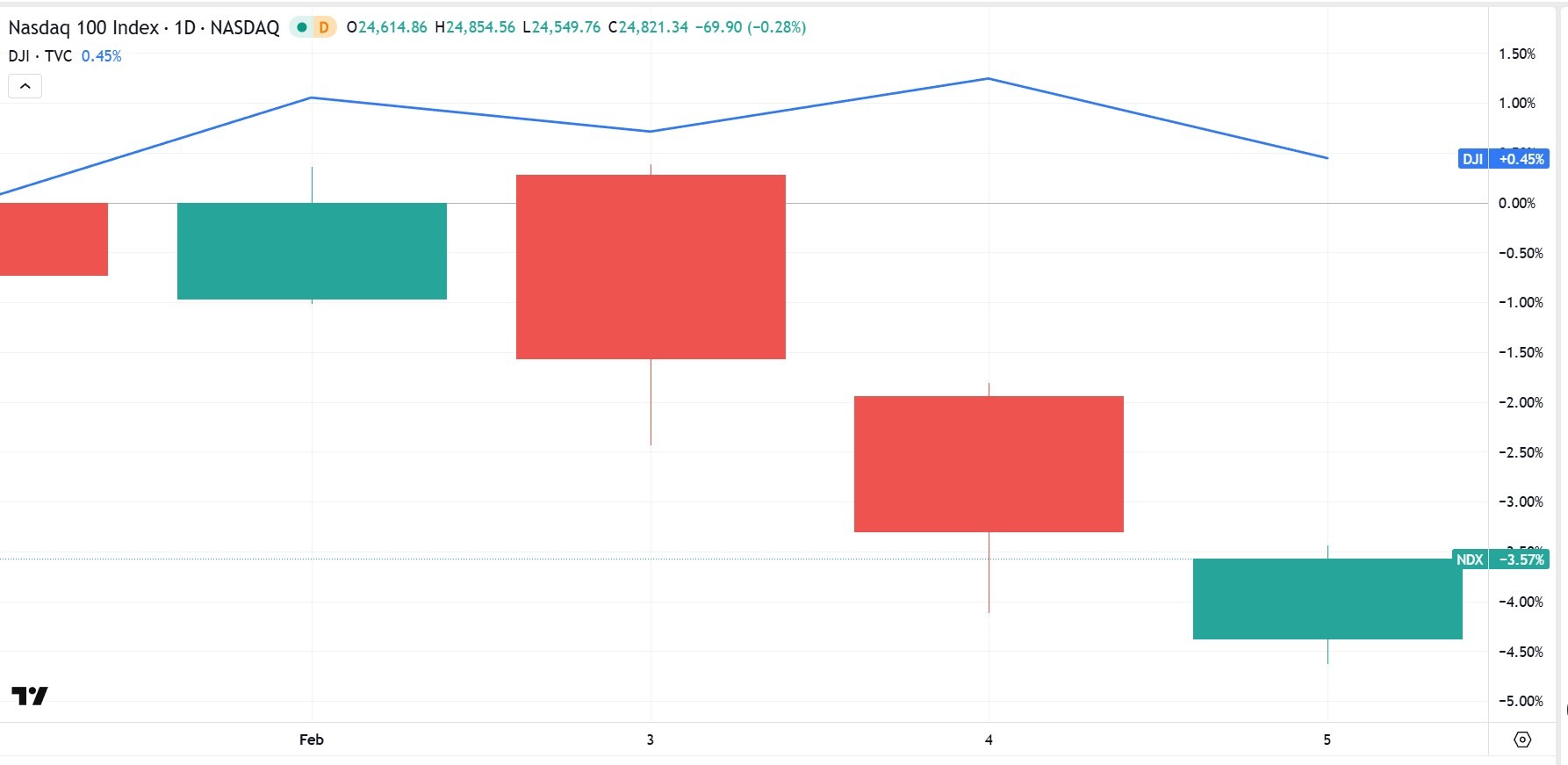

Over the past week, the Dow Jones Industrial Average has outperformed, trading just below neutral, while the Nasdaq-100 has declined more than 4%, reflecting sensitivity in large-cap technology to firmer yields.

What the move may reflect

- Rate-driven pressure on growth stocks

- Profit-taking after strong tech performance

- Earnings season favouring broader sector participation

- A generally more cautious tone across higher-beta assets

Markets typically look for sustained multi-week outperformance in financials, industrials or defensives before characterising the shift as structural rotation.

Market impact

- Tech remains more sensitive to yield moves

- Value and defensive sectors may see relative support

- Earnings guidance continues to influence leadership

Reportingdates and release times are based on company investor relations calendars whereconfirmed. Where dates or times are not marked confirmed, they are GO Marketsestimates. Consensus EPS, revenue and analyst-range data are sourced fromBloomberg and Earnings Whispers, as at 09 July 2026 (AEST). Company guidance,backlog and operating metrics are sourced from the latest company filings orresults presentations, unless stated otherwise. Any scenario analysis reflectsGO Markets analysis. Figures and schedules may change without notice.

The information provided is of general nature only and does not take into account your personal objectives, financial situations or needs. Before acting on any information provided, you should consider whether the information is suitable for you and your personal circumstances and if necessary, seek appropriate professional advice. All opinions, conclusions, forecasts or recommendations are reasonably held at the time of compilation but are subject to change without notice. Past performance is not an indication of future performance. Go Markets Pty Ltd, ABN 85 081 864 039, AFSL 254963 is a CFD issuer, and trading carries significant risks and is not suitable for everyone. You do not own or have any interest in the rights to the underlying assets. You should consider the appropriateness by reviewing our TMD, FSG, PDS and other CFD legal documents to ensure you understand the risks before you invest in CFDs. These documents are available here.

Any references to Australian or international shares, sectors, indices, ETFs, crypto-related stocks or other instruments are provided for market commentary and watchlist purposes only and do not constitute a recommendation, offer or solicitation to buy, sell or hold any financial product or adopt any investment strategy. International markets may involve additional risks, including currency fluctuations, regulatory differences, market structure differences, reduced liquidity and higher volatility. Company-specific, sector-specific and macroeconomic risks may also affect performance.

Commentary on geopolitical developments, economic data, central bank decisions, earnings, policy changes and other global or financial market events is based on information available at the time of publication and may change without notice. Such events can lead to sudden market moves, price gaps, reduced liquidity, wider spreads and increased volatility, particularly in leveraged products such as CFDs. Forward-looking statements, expectations and scenario analysis are inherently uncertain and should not be relied on as guarantees of future market behaviour or outcomes.