One Emotional Discipline: This is the precise reason why not everyone can trade. Understanding the fundamentals of the market is not beyond you and learning a technical system that provides an edge in the market is certainly not hugely challenging. However learning the skill of emotional discipline is the greatest profit making skill great traders have.

To develop the emotional discipline that all great traders have takes time and it takes a lot of patience but it can be done. There are 3 things that can help you develop the emotional discipline required. » Most budding forex traders in my experience trade too much resulting in a “duck hunter” approach rather than a “sniper” approach. The result is they trade emotionally instead of logically following a specific trading plan.

Over many years I have seen forex traders substantially improve their trading results by simply trading less. » One thing you need as a trader is time, time to learn the skill of trading and being able to stay in the game without blowing your trading account. Nobody makes it in this business without experiencing trading losses however you need to fail gracefully and this means losing small and winning bigger. » Rather than looking at your forex trades in a win-loss fashion consider looking at your trade results in blocks of 10 trades. Trading is a numbers game and if you have a specific currency trading plan that has an edge then you have a historical probability of success, you just need to see it through and play the system properly.

The system or your results cannot be measured over one, two or even three forex trades. Great trades understand the numbers game over time and it allows them to develop the emotional discipline. Two Focus: Think about someone that you know to be successful and wealthy.

There is a strong possibility that person achieved their success and wealth from being a specialist in one field. Steve Jobs was successful at building computers, Richard Branson made his first fortune selling records, Rupert Murdoch made his fortune selling Newspapers, George Soros made his fortune trading currencies and Warren Buffett made his fortune buying companies on the stock market. They applied incredible focus to the business they were in and initially did not diversify.

It was this single-minded focus on one thing that drove them to the success and yes many of them have diversified since. But they focused on one thing to start with. So I believe you will improve your probability of trading success by focusing on one market and becoming a specialist in that market.

It will allow you to focus intently on what is driving that market, it will allow you to focus on becoming the detective that you need to be and it will allow you to likely find value in a market before everyone else has figured out what you are considering buying is a good idea. Consider focusing on one market and become your own master of that market and you will likely improve the chances of your success. Watch your inbox for the link to join Senior Currency Analyst and Sky News Money host Andrew Barnett for weekly free live currency coaching sessions.

They are at 7pm AEST every Wednesday. Andrew Barnett | Director / Senior Currency Analyst Andrew Barnett is a regular Sky News Money Channel Guest and one Australia’s most awarded and respected financial experts, and is regularly contacted by the Australian Media for the latest on what is happening with the Australian Dollar. Connect with Andrew: Email

By

GO Markets

The information provided is of general nature only and does not take into account your personal objectives, financial situations or needs. Before acting on any information provided, you should consider whether the information is suitable for you and your personal circumstances and if necessary, seek appropriate professional advice. All opinions, conclusions, forecasts or recommendations are reasonably held at the time of compilation but are subject to change without notice. Past performance is not an indication of future performance. Go Markets Pty Ltd, ABN 85 081 864 039, AFSL 254963 is a CFD issuer, and trading carries significant risks and is not suitable for everyone. You do not own or have any interest in the rights to the underlying assets. You should consider the appropriateness by reviewing our TMD, FSG, PDS and other CFD legal documents to ensure you understand the risks before you invest in CFDs. These documents are available here. Any references to Australian or international shares, sectors, indices, ETFs, crypto-related stocks or other instruments are provided for market commentary and watchlist purposes only and do not constitute a recommendation, offer or solicitation to buy, sell or hold any financial product or adopt any investment strategy. International markets may involve additional risks, including currency fluctuations, regulatory differences, market structure differences, reduced liquidity and higher volatility. Company-specific, sector-specific and macroeconomic risks may also affect performance.

Commentary on geopolitical developments, economic data, central bank decisions, earnings, policy changes and other global or financial market events is based on information available at the time of publication and may change without notice. Such events can lead to sudden market moves, price gaps, reduced liquidity, wider spreads and increased volatility, particularly in leveraged products such as CFDs. Forward-looking statements, expectations and scenario analysis are inherently uncertain and should not be relied on as guarantees of future market behaviour or outcomes.

Every time markets get jumpy, a three-letter acronym starts showing up in headlines and trading rooms. The VIX. You will see it called the fear gauge, the fear index, or just "vol." For newer traders, it can feel like an insider's number that everyone seems to track but few stop to explain.

Here is the part many new traders miss. The VIX is not a prediction of where the market will go. It is a reading of how much movement the market expects in the near future. That distinction sounds small. It changes how the number should be used.

This Playbook breaks the VIX down for beginner to light-intermediate traders. Part 1 explains what it is and how it works. Part 2 turns that understanding into a practical, scenario-based process you can use to prepare, observe, and manage risk.

Before you look for a setup

Understand how this market actually behaves first. Use this guide as a starting point, then practise the concepts on charts, watchlists, and demo tools before applying them in live conditions.

Part 01

The 101 explainer

Build a clear, foundational understanding before you do anything else.

The basics

What is the VIX, in plain English

The VIX is the Cboe Volatility Index. It is a real-time index designed to measure the expected volatility of the S&P 500 over the next 30 days. It is calculated from the prices of S&P 500 index options.

Here is a simpler way to picture it. Imagine the options market is a giant insurance market for stocks. When traders are worried, they pay more for protection. When they are calm, that protection gets cheaper. The VIX takes those insurance prices and turns them into a single number.

The VIX is not a measure of what has happened. It is a measure of what option markets expect to happen, in terms of magnitude, not direction.

The VIX does not tell you whether the S&P 500 will go up or down. It tells you how much movement is being priced in.

The VIX is not directly tradable as a stock. Traders gain exposure through related products such as VIX futures, VIX options, and volatility-linked exchange-traded products.

The VIX has spiked during every major market stress event

Approximate monthly closing levels of the Cboe Volatility Index, 2007 to 2024

Illustrative

Source: Stylised representation based on publicly reported Cboe VIX historical data (Cboe Global Markets). Selected month-end values are indicative only and intended for educational illustration. The VIX peak of approximately 82 during March 2020 and the GFC peak above 80 in late 2008 are widely reported. Past performance is not an indication of future performance.

Why It Matters

Why the VIX matters to new traders

Even if you never plan to trade volatility directly, the VIX still matters. It is one of the cleanest reads on market sentiment available, and it tends to move in ways that reflect risk appetite across global markets.

When the VIX rises sharply, it often coincides with falls in equity indices, wider spreads in many CFD markets, and a flight to perceived safer assets such as the US dollar, gold, or government bonds. When the VIX is low and stable, conditions often favour trending behaviour and tighter spreads.

For CFD traders, this matters because leverage can magnify both gains and losses. Volatility is the engine behind both. A market that moves more in a day can offer more opportunity, but it also raises the risk of fast adverse moves, gaps around news, and stop-outs in thin liquidity.

Vocabulary

The key terms to know

You do not need to memorise every piece of options jargon to use the VIX. These are the terms that come up most often.

Implied volatility

The market's expectation of how much an asset will move in the future, derived from option prices. The VIX is built from implied volatility.

Realised volatility

How much the market actually moved over a past period. Useful for comparing expectations against reality.

S&P 500

The benchmark index of around 500 large US companies. The VIX is calculated from options on this index.

Mean reversion

The tendency of a series to return to its long-term average over time. The VIX is widely described as mean-reverting.

Contango

The normal shape of the VIX futures curve, where longer-dated contracts trade higher than the spot VIX. Why it matters: cost can eat into returns over time.

Backwardation

When longer-dated VIX futures trade below spot. Often short and accompanies fast-moving markets where fear is concentrated now.

Risk-on and risk-off

Shorthand for periods when investors are willing to take more risk, or pull back from riskier assets. VIX rises during risk-off.

Spread

The difference between the bid and ask price. Spreads on many CFD markets can widen during high-volatility events.

Liquidity

How easily an asset can be bought or sold without affecting its price. Liquidity tends to thin out around major news, which can amplify moves.

Mechanics

How it works in real market conditions

The VIX is not pulled out of a single price. It is calculated continuously throughout the US trading session from a wide range of S&P 500 index option prices, weighted by how close they are to current levels and how far out their expiries are.

The VIX tends to move inversely to the S&P 500 most of the time. When equities fall, demand for downside protection often rises, which pushes implied volatility higher. The relationship is not mechanical. There are days when both rise or fall together.

The VIX also tends to spike harder than it falls. Volatility can rise quickly when stress hits the system, then ease more gradually as conditions normalise. Up the elevator, down the escalator.

VIX and the S&P 500 typically move in opposite directions

Stylised illustration of the inverse relationship over a 12-month window

Illustrative

Source: Stylised illustration based on publicly available Cboe VIX and S&P 500 (S&P Dow Jones Indices) historical relationships. The depicted inverse correlation is widely documented in academic and industry research, although the strength of the relationship varies across regimes. Educational purposes only.

Most of the time, the VIX sits below 20

Approximate share of daily closes by VIX range, indicative long-run distribution

Illustrative

Source: Stylised distribution based on publicly reported Cboe VIX historical data spanning multiple decades. Buckets and percentages are indicative and intended for educational illustration. Distributions can shift across volatility regimes.

K

Market IntelligenceDon’t trade the average. Track the split.

Use GO Markets charts, alerts and watchlists to monitor how the K-shaped consumer theme connects with the VIX.

With the Iran conflict reshaping energy markets, central banks turning hawkish, and gold in freefall despite the chaos, the safe haven playbook in 2026 is more complicated than ever.

Quick facts

Gold has fallen more than 20% from its all-time high, despite an active war in the Middle East

The Singapore dollar is near its strongest level against the USD since October 2014

The Reserve Bank of Australia (RBA) hiked rates to 4.10% in March 2026 as Iran-driven oil prices push Australian inflation higher

1. Gold (XAU/USD)

Gold remains the most widely traded safe haven globally. It benefits from geopolitical stress, US dollar weakness, and negative real interest rate environments. However, its short-term behaviour in 2026 demands explanation.

Despite an active war in the Middle East, gold has sold off sharply. The likely cause is the Fed trimming its 2026 rate cut projections, citing hotter-than-expected producer inflation and Strait of Hormuz-driven oil prices creating inflation persistence.

Ultimately, gold's bull case rests on falling real yields and a weaker dollar, and right now neither condition is in place. Traders should be aware that during an inflationary supply shock like the one the Iran conflict has delivered, gold does not always behave as expected.

However, if you zoom out, the longer-term picture reinforces gold’s safe-haven status, ending 2025 as one of its strongest years on record.

Key variables to watch: US Federal Reserve guidance, real yields, and USD direction.

2. Japanese Yen (JPY)

The yen has long functioned as a safe-haven currency thanks to Japan's status as the world's largest net creditor nation. In times of stress, Japanese investors tend to repatriate capital, driving the yen higher.

However, that dynamic seems to have shifted in 2026 so far. The yen is down 6.63% YoY, near its weakest level since July 2024, and surging oil import costs are weighing on the currency.

The yen's safe-haven role has not disappeared, though. It tends to reassert itself during sharp equity selloffs and liquidity events. But in an oil-driven inflation shock, it faces structural headwinds.

Key variables to watch: BOJ rate decisions, US-Japan yield differentials, and any intervention signals from Japanese authorities.

3. Swiss Franc (CHF)

Switzerland's political neutrality, account surplus, and strong institutional framework make the franc a reflexive safe-haven currency. Unlike the yen, the CHF is holding up in the current environment, with the franc gaining against the dollar in 2026, and EUR/CHF remaining stable.

For traders across Europe and the Middle East, CHF is often the first port of call during stress events.

Key variables to watch: Swiss National Bank intervention language, European geopolitical developments, and global risk indices.

4. US Treasury Bonds (US10Y)

Under normal conditions, US government bonds are some of the deepest, most liquid safe-haven instruments in the world. But 2026 is not normal conditions…

Yields have been rising, not falling, meaning bond prices are moving in the wrong direction for anyone seeking safety.

When yields rise during a risk-off event, it signals the market is treating bonds as an inflation risk rather than a safety asset.

However, short-duration Treasuries like bills and 2-year notes are a different story. They may offer higher income with less duration risk than longer-dated bonds, which is why some investors use them more defensively in volatile periods.

Key variables to watch: Fed communication, CPI and PCE data, and whether the 10Y yield breaks above 4.50% or pulls back below 4.00%.

5. Australian Dollar vs. US Dollar (AUD/USD): inverse play

The Australian dollar is widely considered a risk-on currency, tied closely to global commodity demand and Chinese growth.

In risk-off environments, AUD/USD typically falls. A falling AUD/USD can serve as a leading indicator of broader global stress, which can be useful context for traders with regional exposure.

The RBA hiking cycle (two hikes since the start of 2026) is providing some floor under the AUD, but in a sustained global risk-off move, that support has limits.

Key variables to watch: RBA forward guidance, Chinese PMI data, iron ore prices, and oil's impact on Australian inflation expectations.

6. US Dollar Index (DXY)

The US dollar acts as the world's reserve currency and a reflexive safe haven during acute stress. When liquidity dries up, global demand for USD tends to spike regardless of the underlying trend.

Over the past 12 months, the dollar has lost ground as global confidence in US fiscal trajectory has wavered. But over the past month, it has firmed, supported by a hawkish Fed and elevated geopolitical risk.

In risk-off environments, the USD continues to attract safe-haven flows. However, rising oil prices can increase inflation risks, complicating Federal Reserve policy expectations.

Key variables to watch: Fed rate path, US inflation data, and global liquidity conditions.

7. Singapore Dollar (SGD)

Less discussed globally but highly relevant across Southeast Asia, the SGD is one of the most quietly resilient currencies in the current environment.

The Singapore dollar has advanced to near its highest level since October 2014, supported by safe haven flows and investors drawn to Singapore's AAA-rated bonds, a dividend-heavy stock market, and predictable government policies.

The MAS manages the SGD through a nominal effective exchange rate band rather than an interest rate, giving it a different character from other safe-haven currencies.

For traders with exposure to Indonesia, Malaysia, Thailand, Vietnam, and the broader ASEAN region, USD/SGD can act as a practical benchmark for regional risk appetite.

Key variables to watch: MAS policy band adjustments, regional trade flows, and USD/Asia dynamics more broadly.

8. Cash and Short-Duration Fixed Income

Sometimes, the most effective safe haven can be to simply reduce exposure. With central bank rates still elevated across major economies, cash and short-duration government bonds can offer a meaningful yield while sitting outside market risk.

The RBA raised the cash rate to 4.10% at its March meeting. The Bank of England held at 3.75%, while the ECB kept its deposit facility rate at 2.00% and main refinancing rate at 2.15%.Across all major economies, short-duration government paper is offering a real return for the first time in years.

In a volatile environment, capital preservation can sometimes matter more than return maximisation.

Key variables to watch: Central bank meeting calendars across all major economies, and any shifts in forward guidance on the rate path.

What to Watch Next

Fed inflation data. Core PCE is the single most important data point for gold, bonds, and the dollar right now. Any surprise in either direction could move all three simultaneously.

Yen intervention risk. The yen is near levels that have previously triggered action from Japanese authorities. Traders with Asia-Pacific exposure should monitor closely.

RBA's next move. With Australia now at 4.10% and inflation still above target, the question is whether the hiking cycle has further to run. The next RBA meeting is on 5 May.

Geopolitical trajectory. Any move toward de-escalation in the Middle East would quickly reduce safe haven demand and rotate capital back into risk assets. The reverse is equally true.

China's growth signal. A stronger-than-expected Chinese recovery could lift commodity currencies and reduce defensive positioning across Asia-Pacific.

The Longer-Term Lens

The 2026 environment is exposing that the effectiveness of safe haven assets depends on the type of shock, not just its severity.

An inflationary supply shock like the Iran conflict has delivered is one of the most difficult environments for traditional safe havens.

Gold falls as real yields rise. Bonds sell off as inflation expectations climb. Even the yen can weaken as Japan's import costs surge.

What has held up are assets with institutional credibility, managed frameworks, and deep liquidity regardless of macro conditions. The Swiss franc, Singapore dollar, and short-duration cash instruments fit that description better than gold or long bonds do right now.

In 2026, the question for traders is not "which safe haven?" It is "a safe haven from what?"

If you've spent any time looking at a trading terminal, you've seen it. A news headline breaks, a chart line snaps, and suddenly everyone is rushing for the same exit or the same entrance. It looks like chaos. In practice, it is often a chain of mechanical responses.

This matters for a couple of reasons. Many readers assume the story is the trade. It is not. The story, whether it is an interest rate decision, a supply shock or an earnings miss, is the fuel and the playbook is the engine.

Below are seven core strategies often used in contracts for difference (CFDs) trading. With CFDs, you are not buying the underlying asset. You are speculating on the change in value. That means a trader can take a long position if the price rises, or a short position if it falls.

Seven strategies to understand first

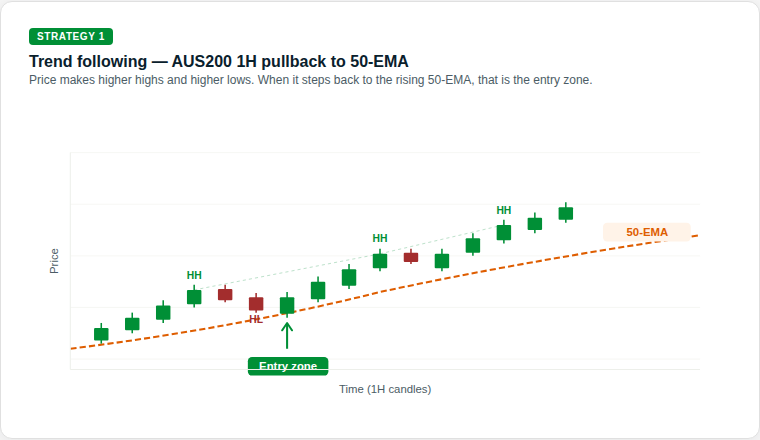

1. Trend following (the establishment play)

Trend following works on the idea that a market already in motion can remain in motion until it meets a clear structural obstacle. Some market participants view it as a chart-based approach because it focuses on the prevailing direction rather than trying to call an exact turning point.

The rationale: The aim is to identify a clear directional bias, such as higher highs and higher lows, and follow that momentum rather than position against it.

What traders look for: Exponential moving averages (EMAs), such as the 50-day or 200-day EMA, are commonly used to interpret trend strength, though indicators can produce false signals and are not reliable on their own.

Source: GO Markets | Educational example only.

How it works: The 50-period EMA can act as a dynamic support level that rises as price rises. In an uptrend, some traders watch for the market to make a new higher high (HH), then pull back towards the EMA before moving higher again. Each higher low (HL) may suggest buyers are still in control.

When price touches or comes close to the 50-period EMA during that pullback, some traders treat that area as a potential decision zone rather than assuming the trend will resume automatically.

What to watch: The sequence of HHs and HLs is part of the structural evidence of a trend. If that sequence breaks, for example if price falls below the previous HL, the trend may be weakening and the setup may no longer hold.

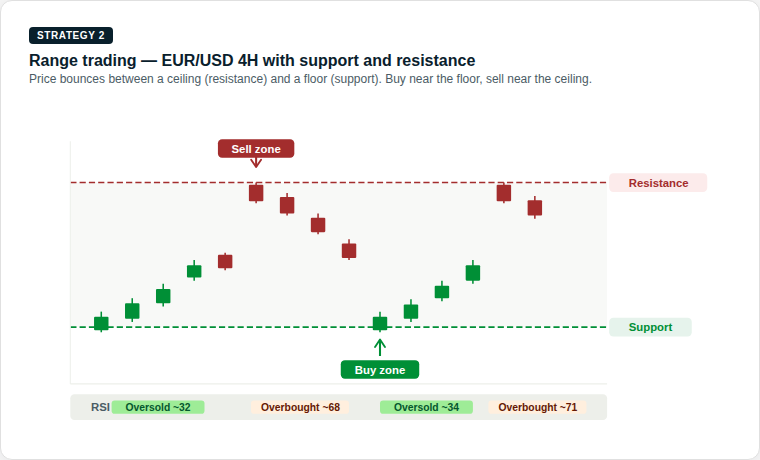

2. Range trading (the ping-pong play)

Markets can spend long stretches moving sideways. That creates a range, where buyers and sellers are in temporary balance. Range trading is built around this behaviour, focusing on moves near the bottom and top of an established range.

The rationale: Price moves between a floor, known as support, and a ceiling, known as resistance. Moves near those boundaries can help define the width of the range.

What traders look for: Some traders use oscillators such as the Relative Strength Index (RSI) to help judge whether the asset looks overbought or oversold near each boundary.

Source: GO Markets | Educational example only.

How it works: The support level is a price zone where buying interest has historically been strong enough to stop the market from falling further. The resistance level is where selling pressure has historically prevented further gains.

When price approaches support, some traders look for signs of a potential rebound. When it approaches resistance, they look for signs that momentum may be fading. RSI readings below 35 can suggest the market is oversold near support, while readings above 65 can suggest it is overbought near resistance.

What to watch: The main risk in range trading is a breakout, when price pushes decisively through either level with strong momentum. This may signal the start of a new trend and using a stop-loss just outside the range on each trade may help manage that risk.

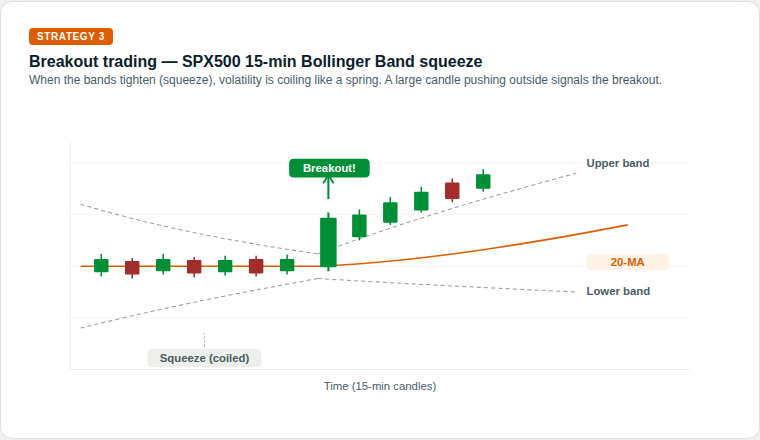

3. Breakouts (the coiled spring play)

Eventually, every range comes under pressure. A breakout happens when the balance shifts and price pushes through support or resistance. Markets alternate between periods of low volatility, where price moves sideways in a tight range, and high-volatility bursts where price can make a larger directional move.

The rationale: Quiet consolidation can sometimes be followed by a broader expansion in volatility. The tighter the compression, the more energy may be stored for the next move.

What traders look for: Bollinger Bands are often used to interpret changes in volatility. When the bands tighten, a squeeze is forming. Some market participants view a move outside the bands as a sign that conditions may be changing.

Source: GO Markets | Educational example only.

How it works: Bollinger Bands consist of a middle line, the 20-period moving average, and 2 outer bands that expand or contract based on recent price volatility. When the bands narrow and come close together, the squeeze, the market has been unusually calm.

This is often described as a coiled spring. Energy may be building, and a sharper move can follow. Some traders treat the first move through an outer band as an early clue on direction, rather than a definitive signal on its own.

What to watch: Not every squeeze leads to a powerful breakout. A false breakout occurs when price briefly moves outside a band, then quickly reverses back inside. Waiting for the candle to close outside the band, rather than entering mid-candle, can reduce the risk of being caught in a false move.

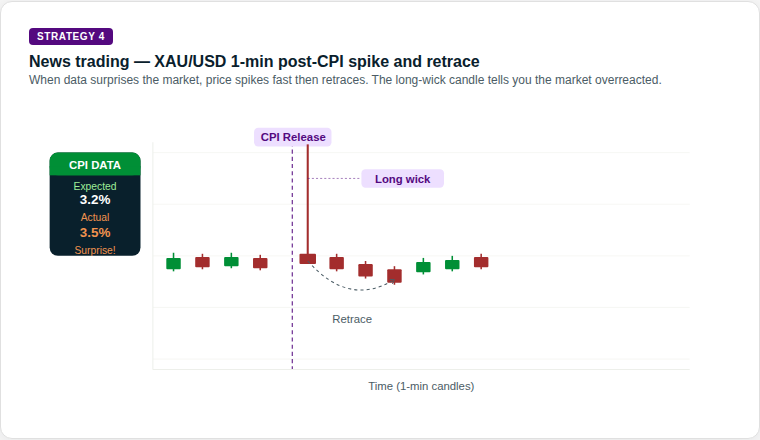

4. News trading (the deviation play)

This is event-driven trading. The focus is on the gap between what the market expected and what the data or headline actually delivered. Economic data releases, such as inflation figures (CPI), employment reports and central bank decisions, can cause sharp, fast moves in financial markets.

The rationale: High-impact releases, such as inflation data or central bank decisions, can force a fast repricing of assets. The bigger the surprise relative to expectations, the larger the move may be.

What traders look for: Traders often use an economic calendar to track timing. Some focus on how the market behaves after the initial reaction, rather than treating the first move as definitive.

Source: GO Markets | Educational example only.

How it works: Before the news, price may move in a calm, tight range as traders wait. When the data is released, if the actual reading differs significantly from the consensus expectation, repricing can happen fast.

Gold, for example, may spike sharply on a CPI reading that comes in above expectations. However, the candle can also print a very long upper wick, meaning price reached the spike high but was then rejected strongly. Sellers may step in quickly, and price may retrace. This spike-and-retrace pattern is one of the more recognisable setups in news trading.

What to watch: The direction and size of the initial spike do not always tell the full story. Wick length can offer an important clue. A long wick may suggest the initial move was rejected, while shorter wicks after a data release may indicate a more sustained directional move.

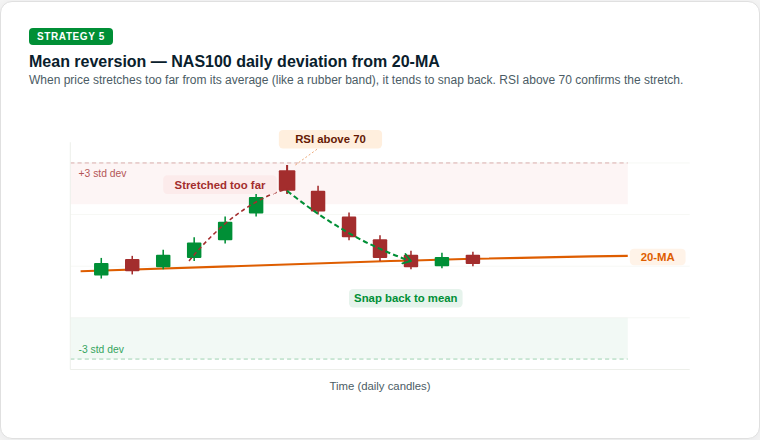

5. Mean reversion (the rubber-band play)

Prices can sometimes move too far, too fast. Mean reversion is built on the idea that an overextended move may drift back towards its historical average, like a rubber band pulled too tight, then snapping back.

The rationale: This is a contrarian approach. It looks for stretches of optimism or pessimism that may not be sustainable, and positions for a return to equilibrium.

What traders look for: A common example is price moving well away from a 20-day moving average (MA) while RSI also reaches an extreme reading. In that setup, traders watch for a move back towards the mean rather than a continuation away from it.

Source: GO Markets | Educational example only.

How it works: The 20-period MA represents the market's recent average price. When price moves into an extreme zone, such as more than 3 standard deviations above or below that average, it has moved a long way from its recent trend.

An RSI above 70 can suggest the market is stretched to the upside, while below 30 can suggest the same to the downside. Some mean reversion traders use these combined signals as a sign that a pullback towards the 20-period MA may be possible, rather than assuming the move will continue to extend.

What to watch: Mean reversion strategies can carry significant risk in strongly trending markets. A market can remain extended for longer than expected, and a position entered against the short-term trend can generate large drawdowns. Position sizing and clear stop-losses are critical.

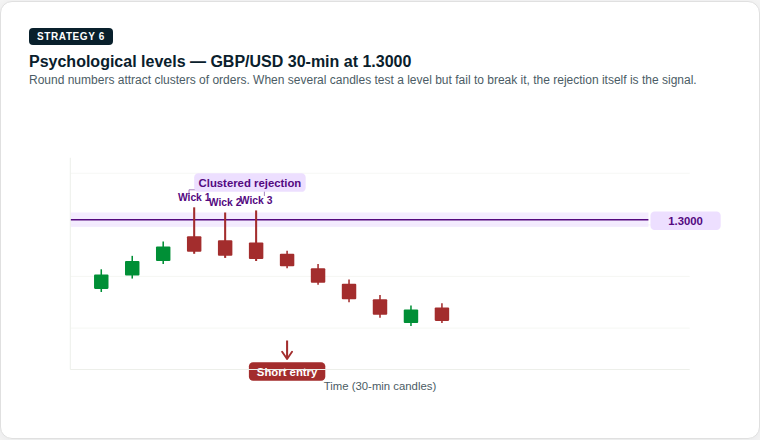

6. Psychological levels (the big figure play)

Markets are driven by people, and people tend to focus on round numbers. US$100, US$2,000 or parity at 1.000 on a currency pair can act as magnets. In financial markets, certain price levels can attract a disproportionate amount of buying and selling activity, not because of technical analysis alone, but because of human psychology.

The rationale: Large orders, stop-losses and take-profit levels can cluster around these big figures, which may reinforce support or resistance. This self-reinforcing behaviour is one reason these rejections can become meaningful for traders.

What traders look for: Traders often watch how price behaves as it approaches a round number. The market may hesitate, reject the level or break through it with momentum. Multiple wick rejections at the same level may carry more weight than a single one.

Source: GO Markets | Educational example only.

How it works: When price approaches a round number from below, some traders watch for long upper wicks, the thin vertical line above the candle body. A long upper wick means price reached that level, but sellers stepped in aggressively and pushed it back down before the candle closed.

One wick rejection may be notable. Three in a cluster may be more significant. Some traders use this accumulated rejection as part of the case for a short (sell) setup at that level.

What to watch: Psychological levels can also act as magnets in the opposite direction. If price breaks through with conviction, the level may then act as support. A decisive close above the level, rather than just a wick break, can be an early sign that the rejection setup is no longer holding.

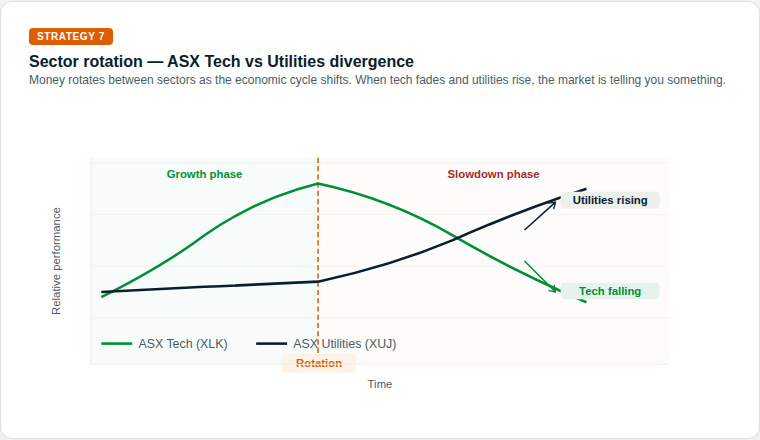

7. Sector rotation (the economic season play)

This is a macro strategy. As the economic backdrop changes, capital may move from higher-growth sectors into more defensive ones, and back again. Not all parts of the sharemarket move in the same direction at the same time.

The rationale: In a slowing economy, discretionary spending may weaken while demand for essential services can remain more stable. Investors may rotate capital between sectors accordingly.

What traders look for: With CFDs, some traders express this view through relative strength, taking exposure to a stronger sector while reducing or offsetting exposure to a weaker one.

Source: GO Markets | Educational example only.

How it works: During a growth phase, when the economy is expanding, investors tend to prefer growth-oriented sectors like technology. As the economic environment shifts, perhaps due to rising interest rates, slowing earnings or increasing recession risk, a rotation point may emerge.

In the slowdown phase, the pattern can reverse. Technology may weaken while utilities may strengthen, as investors move capital into defensive, income-generating sectors. Early signals can include relative underperformance in growth sectors combined with unusual strength in defensives.

What to watch: Sector rotation is not usually an overnight event. It typically unfolds over weeks to months. Tracking the ratio between two sectors, often shown in a relative strength chart, can make this shift visible before it becomes obvious in absolute price terms.

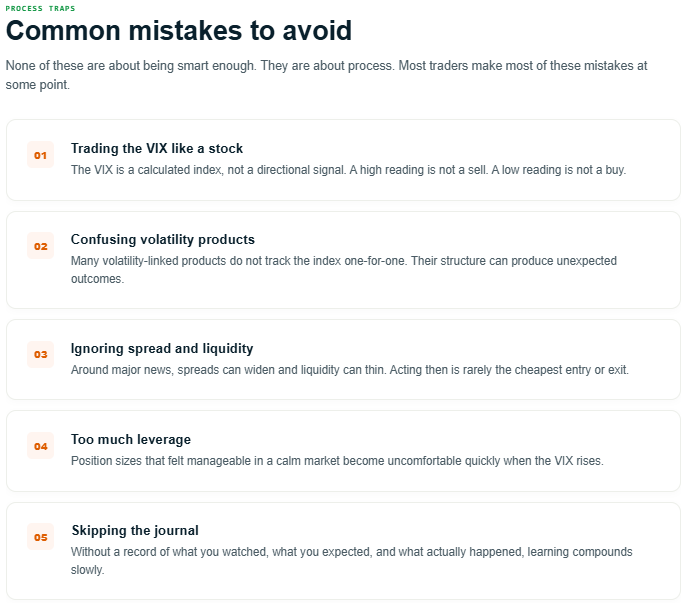

Why risk management is the engine of survival

The headline move is one thing. The market implication for your account is another. If you do not manage the mechanics, the strategy does not matter.

Because CFDs are traded on margin, a small market move may have an outsized impact on the account. If leverage is too high, even a minor wobble may trigger a margin call or automatic position closure, depending on the provider's terms. This is not a theoretical risk. It is a common reason new traders lose more than they expected on a trade that was directionally correct.

The market does not always move in a straight line. Sometimes, price gaps from one level to another, especially after a weekend or major news event and in those conditions, a stop-loss may not be filled at the exact requested price. That is known as slippage. It is one reason large positions may carry additional risk into major announcements.

Bottom line

The vehicle is powerful, but the playbook is what helps keep you on the road.

The obvious trade is often already priced in. What matters more is understanding which market condition is in front of you. Is it trending, ranging, breaking out or simply reacting to a headline?

Readers assessing leveraged products often focus on position sizing, risk limits and product disclosure before deciding whether the product is appropriate for them. The headlines will keep changing. The maths of risk management does not.

Disclaimer: This article is general information only and is intended for educational purposes. It explains common trading concepts and market behaviours and does not constitute financial product advice, a recommendation, or a trading signal. Any examples are illustrative only and do not take into account your objectives, financial situation or needs. CFDs are complex, leveraged products that carry a high level of risk. Before acting, consider the PDS and TMD and whether trading CFDs is appropriate for you. Seek independent advice if needed. Past performance is not a reliable indicator of future results.

The 2026–27 Budget landed in a high-pressure macro environment. With inflation at 5% and the RBA cash rate at 4.35% after three consecutive hikes, the gap between fiscal policy and market price may matter more than usual. The first reaction was predictable.

The more important question is where the transmission lag takes things from here.

Market Insights

How does the RBA actually work?

The Budget sets the scene, but the RBA controls the script. Understand the mechanics behind Australia's central bank before you track the next move.

📈Inflation OutlookTreasury: 5% CPI through June quarter

→

🏦RBA Rate PathCash rate 4.35% Next decision: 16 June

→

💒AUD + ASXAUD/USD 0.7231 Sector rotation underway

NOTE: The chain from Canberra to your portfolio does not move in a straight line but it does follow a logic. Educational illustration. Data as at 13 May 2026.

Policy, price and what the market may have missed

The Budget contains several significant measures and the ones most likely to move markets are not always the ones that dominate the news coverage. Here is how the major items stack up.

Moves that made sense

Energy and fuel security: A$10 billion Fuel Security Reserve. A direct intervention in the sector driving Australia’s inflation spike. Automotive fuel rose 32.8% in the March quarter. This could be a limited tailwind for domestic energy processors and critical minerals names, subject to capital deployment timing.

Critical minerals: Critical Minerals Strategic Reserve and Future Made in Australia funding create a durable government backdrop for downstream processors. Watch for specific procurement announcements and offtake agreements.

The moves that may have run ahead of the evidence

The property sector reaction is worth watching carefully. It is also worth being precise about which part of the property sector is in focus. The negative gearing changes restrict deductions to newly built homes from July 2027, with existing properties grandfathered until sold. That is a meaningful structural shift, but it is 13 months away from even opening the transmission channel.

A-REITs: the cleanest market read

The instrument most directly exposed here is the S&P/ASX 200 A-REIT Index (ASX: XPJ).

📉 A-REITs: The Cleanest Market Read

Metric

Detail

Budget eve close

Approximately 1,542

52-week high

1,975

Main sensitivity

RBA rate path

NOTE: Australian real estate investment trusts (A-REITs) are income-generating vehicles. When rates rise, their yield appeal relative to bonds compresses, and valuations tend to follow.

Why the XPJ reaction needs a closer look

The XPJ’s major constituents respond to different Budget levers.

Goodman GroupASX: GMG

Focused on logistics and industrial property. Limited direct residential policy exposure.

Scentre GroupASX: SCG

Exposed through broader property and consumer conditions.

StocklandASX: SGP

More directly in frame due to significant residential development pipelines.

Mirvac GroupASX: MGR

More directly in frame due to significant residential development pipelines.

The key point

The demand impulse from the negative gearing change is delayed and conditional on the new-build pipeline actually accelerating. There is also a significant second-order effect sitting in the banking sector. The big four Australian banks carry approximately 45 to 50% of their total loan books in residential mortgages. Any policy-driven shift in property transaction volumes, up or down, flows into their book quality. That linkage is worth keeping in mind when reading any Budget-related move in the financials sector.

📐The K-Shape Signal

This Budget may be widening the K, a dispersion pattern where sectors diverge sharply rather than moving together.

On the upper arm: Energy producers, critical minerals processors, and logistics-focused names with hard assets, pricing power, and direct government capital flowing their way.

On the lower arm: Residential-exposed REITs, property developers, and rate-sensitive financials facing the same RBA pressure that existed before the Budget, with no near-term policy relief.

Dispersion, the spread in returns between winners and losers within the same broad index, tends to rise in environments like this. The key question is whether the XPJ moves as a whole, or whether the constituent spread between names like GMG and MGR begins to widen meaningfully.

Related Analysis

The K-shaped consumer and CFD signals

Sector dispersion is reshaping how traders read market momentum. Explore how the K-shaped economy is creating new opportunities and risks for CFD positions in 2026.

The tax changes for workers, including an A$250 Working Australians Tax Offset and an A$1,000 instant tax deduction, are back-loaded to the 2027-28 financial year. If the market is pricing a near-term consumer spending boost off the back of these measures, it may be getting ahead of the calendar. The Treasurer was explicit: the delay is deliberate, designed to avoid adding to the near-term inflation problem.

That is a reasonable fiscal call. It also means the retail and discretionary sectors may not see the consumer lift as quickly as some initial reads implied.

Mortgage book composition, investment property exposure

Healthcare and aged care

NDIS reforms with A$37.8 billion in savings, care sector funding

Neutral to cautious

NDIS participant impact, service provider margins

General market observations only. Not a recommendation to buy or sell any instrument. Sector reactions can be influenced by factors beyond Budget policy.

The sceptic's corner

Before acting on any Budget-driven market reaction, three questions are worth asking. Not because scepticism is always right, but because the Budget has a way of generating confident narratives that look less convincing by the end of the following week.

⚠️

Three questions before you move

01

Is this move driven by the Budget, or was it already in motion?

The AUD was already at 0.7231 before Chalmers spoke, supported by three RBA rate hikes and a broad commodity tailwind. Some of what looks like a Budget reaction may simply be momentum that was already in place. Momentum and catalyst are not the same thing.

Watch: How the AUD and key ASX names behave 48 hours after the initial reaction settles.

02

How much benefit reaches corporate earnings?

Announced spending and deployed spending are two different events, often separated by procurement processes, legislative steps and delivery timelines. Some of the Budget’s biggest measures, including fuel security capital, critical minerals incentives and construction stimulus, run on multi-year schedules. Pricing them as if they are immediate is a common mistake.

Watch: Company guidance at the next earnings season for any specific Budget-linked revenue visibility.

03

If the RBA does not play along, does the whole thesis change?

A Budget that adds demand stimulus into an economy where the RBA is already tightening is not straightforwardly bullish. The central bank moves independently. Its May statement was clear: inflation is likely to stay above the 2–3% target range for some time. If the June decision tilts further toward restraint, some Budget tailwinds may become headwinds, particularly for rate-sensitive sectors like property, REITs and growth stocks.

Watch: RBA meeting minutes on 19 May, 11:30 am AEST, and any post-Budget commentary from the Governor.

Catalyst roadmap: what to monitor and when

The Budget does not exist in isolation. Two data windows before the next RBA decision could easily overshadow it or amplify it. Here is how the scenarios map out.

📅

Next two weeks: consumer confidence and RBA minutes

Two data points land before the end of May. RBA meeting minutes are released on 19 May at 11:30am AEST, the first official post-Budget communication from the central bank. The May consumer confidence print follows in the same week. Together, they offer the first read on whether the fiscal message is landing and whether the RBA is acknowledging the spending impulse.

✅ Base case

Minutes are neutral and confidence holds steady. Budget detail is digested without drama. AUD/USD consolidates near 0.7230. XPJ stays range-bound near 1,542.

📈 Upside scenario

Minutes flag easing concern and confidence lifts. Retail and consumer discretionary names benefit. AUD tests resistance toward 0.7250 to 0.7400.

📉 Downside scenario

Minutes are hawkish and confidence weakens on fuel and rate pressure. Rate-sensitive sectors, including REITs and banks, may give back early Budget gains.

📅

Next 30 days: CPI and the RBA decision

The monthly CPI release on 27 May at 6:00pm AEST is the most consequential single print before the RBA meets on 15 and 16 June, with the decision due at 2:30pm AEST on 16 June. The prior annual reading was 4.6%. These two events together may tell us far more about the durability of any post-Budget market move than the Budget itself.

✅ Base case

CPI softens modestly. RBA holds at 4.35%. Market shifts focus to data rather than fiscal policy. AUD and ASX respond to the print, not the Budget.

📈 Upside scenario

CPI surprises lower. Rate cut expectations pull forward. Budget consumer stimulus looks more meaningful. Risk appetite improves across the ASX. XPJ may recover toward 1,585 to 1,600 resistance.

📉 Downside scenario

CPI surprises higher. A fourth RBA hike comes into view. Fiscal stimulus becomes a headwind, not a tailwind. Property, REITs and growth names face renewed pressure. XPJ risks testing the 1,485 range low.

Disclaimer: The scenarios presented above are for educational purposes and general market commentary only. These are forward-looking projections based on current data as at 13 May 2026; price levels, interest rate expectations, and economic outcomes are subject to change without notice based on market volatility and upcoming data releases. These scenarios should not be interpreted as financial advice or specific trading recommendations.

Indicative levels only, sourced from TradingView and RBA data. ASX 200 and AUD/USD reflect confirmed 12 May 2026 closes. These are not trading signals or recommendations and should be assessed against individual circumstances and current market conditions. Past price behaviour does not guarantee future outcomes. Levels may shift materially around the 27 May CPI print and 16 June RBA decision.

The takeaway

The honest read is that the Budget’s biggest potential benefits are back-loaded or conditional. The fuel security commitment and the critical minerals agenda are immediate. The consumer tax relief and the property market changes are not. All of it sits inside an inflation and rate environment that the RBA, not the Treasurer, ultimately controls.

The next two data points that genuinely matter are the CPI print on 27 May and the RBA decision on 16 June. Watch those. The Budget set the scene. Those events may tell us whether the audience bought the story.

Trader's Playbook

RBA 2026 playbook: What do markets watch in decision weeks?

Understand the critical indicators, from wage growth to unemployment, that dictate 2026 RBA sentiment. Learn to read the triggers that shift sector-wide momentum before the announcement settles.

This is the second part of the GO Markets VIX Playbook. The first piece covered the basics and explored what the VIX measures, what it does not, why traders watch it and where new traders most often misread it. If you skipped it, start there as the foundation matters.

For everyone else, here is the part where theory becomes process.

Knowing what the VIX is does not make decisions for you. A repeatable process does. The sections that follow turn that 101 understanding into a practical workflow. A focused watchlist that travels across regimes. Three scenario timeframes for thinking past the next headline. An if/then framework for pre-committing to reactions before the market forces one. Action points for before, during, and after a move. And a checklist that takes the emotion out of the moments when emotion is most expensive.

The goal is not to predict the next move. It is to be ready for the ones that matter.

Part 02

The practical playbook

Move from understanding to a repeatable, scenario-based process.

Scenario Thinking

What could happen next

The point of this section is not to predict. It is to practise scenario thinking across different time horizons.

Volatility tends to build into events and fade after

Stylised pattern around scheduled catalysts such as central bank decisions

Conceptual

Source: Conceptual illustration. The build-up and fade pattern around scheduled macro events is widely documented in options research. Actual market behaviour varies by event surprise and regime.

Use these as templates for thinking, not as instructions. The point is to know your reaction before the market forces one on you.

VIX rises sharply on a single headline

Whether the move holds into the next session or fades

Initial reactions are often the noisiest part of the move

Price alerts on VIX and US500, plus the economic calendar

VIX stays unusually low for an extended period

Signs of complacency, narrow ranges, crowded positioning

Low-vol regimes can end abruptly when they end

TradingView charts comparing VIX with realised vol

S&P 500 falls and VIX does not rise meaningfully

Whether the decline is orderly rather than stress-driven

Divergences can resolve in either direction

Side-by-side charting with key levels marked

Major central bank meeting is within 48 hours

Spreads, liquidity, option-implied moves on related markets

Event risk can produce gaps and slippage

GO Markets economic calendar and pre-event watchlists

Practical Action

What a process actually looks like

Three windows of attention. Each one has a different question to answer.

01

Before watching the market

•Define what you are watching and why

•Mark recent VIX ranges and key S&P 500 levels

•Check the economic calendar

•Review margin and spread context

•Decide what would invalidate your scenario

02

During the market move

•Avoid reacting to the first headline alone

•Watch for confirmation across related markets

•Monitor spreads, especially around news

•Avoid increasing risk impulsively

•If the move is faster than your plan, slow down

03

After the move

•Review what happened against your scenarios

•Note where your read was useful and where it was not

•Capture emotional mistakes honestly

•Update your watchlist

•Save annotated charts for future reference

Before You Act

Beginner checklist

Tick through this before any volatility-aware trade decision.

I have identified what is driving volatility right now

I have checked the economic calendar for the next 24 to 72 hours

I am reacting to price, not to emotion

I have considered the downside as carefully as the upside

I have compared VIX with yields, gold, and the US dollar

I am only using risk I can afford to lose

I have reviewed my last few trades for similar setups

I know what would invalidate my scenario

I have marked key levels on the S&P 500 and related markets

I understand the spread and margin requirements

I have asked whether the move is already priced in

I have written down my plan, including what I will not do

I have set alerts so I do not need to stare at the screen

I have a way to step away if I need to

The Takeaway

The VIX is a thermometer, not a crystal ball

Reading it well will not tell you which way the market is going, but it can tell you a great deal about how the market is feeling and how much movement is being priced in.

The practical next step is not to predict the next move. It is to build a process. New traders can start by adding the VIX, the US500, and a handful of related markets to a watchlist, setting alerts around key levels, reviewing upcoming events on the economic calendar, and practising scenario planning before using live capital.

Strategic Application

Navigate the divergence

Mastering the VIX is just the first step. Combine volatility insights with our K-shaped market analysis to identify hidden opportunities where sector paths divide.

The VIX is a real-time index that represents the market's expectation of 30-day forward-looking volatility. It is derived from the prices of S&P 500 index options and is often called the "Fear Gauge" because it spikes during periods of high uncertainty.

Why does the VIX matter to traders? +

It acts as a sentiment indicator. A rising VIX often signals equity market stress and wider spreads, while a low VIX suggests complacency. It helps traders decide when to use defensive strategies or adjust position sizing.

Can beginners use a VIX-aware playbook? +

Yes. Beginners shouldn't necessarily trade volatility itself, but they should use the VIX as a "weather report" to understand if market conditions are becoming risky enough to warrant tighter stop-losses or smaller trade sizes.

What is the biggest risk for new traders watching the VIX? +

The biggest risk is treating it as a directional signal (thinking "VIX is high, I must sell stocks"). The VIX measures expected magnitude of movement, not the direction of that movement.

Which tools can help traders prepare? +

Interactive charting tools like TradingView, an economic calendar for tracking catalysts, and price alerts are essential. GO Markets also provides a demo environment to test these concepts without financial risk.

Tuesday, 12 May 2026, at roughly 7:30 pm AEST, Treasurer Jim Chalmers will stand up in Canberra and deliver the 2026-27 Federal Budget. According to Budget.gov.au, that is when the Budget is officially released, with the Budget papers going live online at the same time.

But this is not just another Budget night.

The Treasurer is putting together a fiscal plan while rates are moving higher, not lower. That is what makes this one feel different. The Reserve Bank of Australia (RBA) lifted the cash rate to 4.35 per cent on 5 May, its third straight hike this year, in an 8 to 1 vote.

That is the part Australian market participants may not want to overlook.

Market Event

Countdown to the 2026–27 Budget

Treasurer delivers speech Tuesday, 12 May 2026 at 7:30 pm AEST

Initializing...

AEST (+10)

7:30 PM

VIC, NSW, QLD, TAS, ACT

ACST (+9.5)

7:00 PM

SA, NT

AWST (+8)

5:30 PM

WA

LHST (+10.5)

8:00 PM

Lord Howe Island

Budget basics in plain English

The Federal Budget is basically the government’s plan for the year ahead. It sets out how much it expects to spend, tax and borrow, along with its forecasts for growth and inflation.

Markets usually care less about the big speech and more about the details buried in the papers. Think deficits, debt issuance, inflation assumptions, household relief, infrastructure spending and sector-specific surprises.

The Treasurer has already flagged a productivity package and a savings package. The Prime Minister has also shifted the broader message towards ‘national resilience’.

Those phrases may sound political, but they can matter for markets once the numbers are released.

The 2026–27 Budget catalyst watchlist

Sector

Budget Catalyst

Key Tickers / CFDs

What to Monitor

Retail

Cost-of-living rebates, A$300 tax offset

Woolworths (WOW), Wesfarmers (WES)

Spending resilience

Energy

A$10bn Fuel Security package

Santos (STO), Woodside (WDS)

Infrastructure spend

Housing

CGT/negative gearing tweaks

REA Group (REA), CBA, NAB

Loan demand, REIT pricing

Materials

Infrastructure build-out

BHP, Rio Tinto (RIO)

Iron ore assumptions

FX & Rates

Fiscal stance & debt issuance

AUD/USD, AGB 10-year futures

RBA rate pricing

Budget night scenarios

None of these are predictions, rather they are frameworks for thinking about how markets may initially react once the Budget papers are released.

Cost-of-living support

Rebates and targeted relief may give consumer-facing stocks some support. The other side is inflation risk. If markets see the package as too generous, bond yields could move higher.

Infrastructure and resilience

Construction and materials stocks could be sensitive to any new infrastructure commitments. If a fuel-security buildout is confirmed, related sectors may also get some attention.

Tax settings

Possible CGT discount changes or a return to indexation should be checked against the final papers. Markets may also watch for any flow-through to property-exposed stocks and REITs.

Fiscal restraint

A tighter Budget may be read as less inflationary, which could support bonds. Sectors that rely on government spending could face headwinds.

AUD reaction

The Aussie may move around RBA rate pricing after the Budget. That said, global drivers and commodity prices, especially oil and iron ore, can often outweigh local Budget flows.

A short pre-budget checklist

1

Confirm the release time and relevant Budget papers.

2

Note what may already be priced in, including CGT changes and fuel security.

3

Monitor AUD/USD reference levels, including 0.7180 and 0.7250.

4

Watch the 10-year government bond yield as macro confirmation.

5

Review position sizing and stops in the context of event risk.

6

Separate the political headline from the actual market implications.

Where it can go wrong

The Budget rarely writes the whole script. In fact, some measures may already be priced in. Offshore moves can dominate, details may be revised in coming weeks, and the RBA’s June meeting may matter more than any single line item.

Sector winners can still fall if valuations are stretched and the next inflation print may also overwrite the night’s narrative.

Takeaway

For newer Australian market participants, the key point is this: the Budget is a catalyst, not a crystal ball and the job is not to guess every measure. It is to watch how the Budget shifts expectations for rates, inflation, government borrowing, household income and company earnings.

That is the chain that moves prices, often well after the speech is over.

Join us on Wednesday morning for GO's reeaction and what it means for the Aussie dollar, the ASX and your trading.

Market Intelligence

Track the next catalyst

From CPI prints to RBA meetings, stay ahead of the volatility. Map the calendar and track AUD/USD or the ASX 200.