Rather than looking for a reversal, fractal breakouts use the last fractal high (in an uptrend) or last fractal low (in a downtrend) as confirmation of a trend after a retracement in priceIt is a continuation strategy designed to capture momentum once the price has confirmed direction. When price breaks beyond the most recent fractal, it signals that the prevailing trend has the strength to continue.

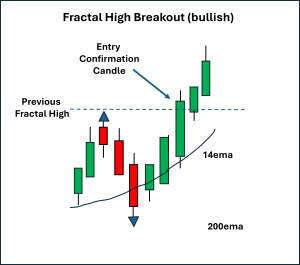

Bullish Fractal Breakout

A bullish fractal breakout occurs when price pushes above the last swing high (marked by a fractal). This indicates buyers have overcome the previous barrier, and the uptrend may continue after a small pullback in price.Confirmation is strengthened when the breakout candle also closes above both the 14 EMA and the 200 EMA, showing alignment of short-term momentum with long-term trend direction.

A: Prior uptrend (bull candles) → sustained buying pressure pushing toward resistance.B: Fractal high → the last swing high marked by a fractal, acting as a breakout trigger.C: Breakout candle → strong bullish candle closing ABOVE the fractal high (and ideally above both 14 EMA and 200 EMA).You can see a real chart example of this on the 1-hourly Gold (XAUUSD) CFD chart:[caption id="attachment_713057" align="aligncenter" width="722"]

Red squares show the last fractal of note. “E” shows where the entry points could be placed[/caption]

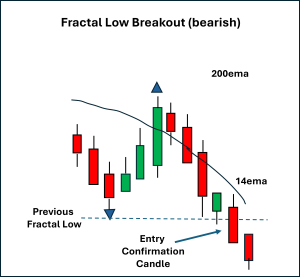

Bearish Fractal Breakout

A bearish fractal breakout occurs when price pushes below the last swing low (marked by a fractal). This shows that sellers have reconfirmed control after a small retracement, and the downtrend is likely to continue.As with the bullish version, the signal is considered stronger if the breakout candle also closes below both the 14 EMA and the 200 EMA.

A: Prior downtrend (bear candles) → sustained selling pressure pushing toward support.B: Fractal low → the last swing low marked by a fractal, acting as a breakout trigger.C: Breakout candle → strong bearish candle closing BELOW the fractal low (and ideally below both 14 EMA and 200 EMA).You can see a real-world example of this on the 1-hourly EURUSD chart: [caption id="attachment_713059" align="aligncenter" width="793"]

Red squares show the last fractal of note. “E” shows where the entry points could be place[/caption]

Stop Placement and Exits for Fractal Breakouts

Stops are logically placed on the opposite side of the breakout fractal:

- For bullish breakouts: The stop goes below the breakout candle or below the prior swing low.

- For bearish breakouts: The stop goes above the breakout candle or above the prior swing high.

Exits can be managed by:

- Targeting the next logical resistance (bullish) or support (bearish) level

- Using a fixed risk-reward ratio (e.g., 2 or 3:1)

- Trailing stops along a moving average (e.g., the 14 EMA).

- Variation: Some suggest a close beneath this (rather than just a touch) may be worth exploring as a variation.

The combination of fractals with moving averages can assist in avoiding weaker signals, but a failure to follow through on this concept is at the basis of exit approaches.

Final Thoughts

The fractal breakout setup is a clean and structured way to trade with the trend. It provides confirmation that buying pressure still exists, even after a recent pullback in price. By waiting for price to confirm beyond the last fractal point, rather than the common “buy on the dip,” you can avoid premature entries and align with the story that price action is telling you.Adding moving average filters, such as the 14 EMA for momentum and the 200 EMA for long-term bias, can significantly improve reliability, though different combinations may suit different market types and timeframes.Like all strategies, it will not always go in your favour, and even if it does, you should endeavour to reduce the amount of “give-back” of potential profit. Breakout ideas can fail, especially in choppy conditions. Risk management and unambiguous pre-defined exit criteria are essential — the only real failure is when you fail to have these in place or fail to execute your risk management.

The information provided is of general nature only and does not take into account your personal objectives, financial situations or needs. Before acting on any information provided, you should consider whether the information is suitable for you and your personal circumstances and if necessary, seek appropriate professional advice. All opinions, conclusions, forecasts or recommendations are reasonably held at the time of compilation but are subject to change without notice. Past performance is not an indication of future performance. Go Markets Pty Ltd, ABN 85 081 864 039, AFSL 254963 is a CFD issuer, and trading carries significant risks and is not suitable for everyone. You do not own or have any interest in the rights to the underlying assets. You should consider the appropriateness by reviewing our TMD, FSG, PDS and other CFD legal documents to ensure you understand the risks before you invest in CFDs. These documents are available here.

Any references to Australian or international shares, sectors, indices, ETFs, crypto-related stocks or other instruments are provided for market commentary and watchlist purposes only and do not constitute a recommendation, offer or solicitation to buy, sell or hold any financial product or adopt any investment strategy. International markets may involve additional risks, including currency fluctuations, regulatory differences, market structure differences, reduced liquidity and higher volatility. Company-specific, sector-specific and macroeconomic risks may also affect performance.

Commentary on geopolitical developments, economic data, central bank decisions, earnings, policy changes and other global or financial market events is based on information available at the time of publication and may change without notice. Such events can lead to sudden market moves, price gaps, reduced liquidity, wider spreads and increased volatility, particularly in leveraged products such as CFDs. Forward-looking statements, expectations and scenario analysis are inherently uncertain and should not be relied on as guarantees of future market behaviour or outcomes.