Market news & insights

Stay ahead of the markets with expert insights, news, and technical analysis to guide your trading decisions.

If you've spent any time looking at a trading terminal, you've seen it. A news headline breaks, a chart line snaps, and suddenly everyone is rushing for the same exit or the same entrance. It looks like chaos. In practice, it is often a chain of mechanical responses.

This matters for a couple of reasons. Many readers assume the story is the trade. It is not. The story, whether it is an interest rate decision, a supply shock or an earnings miss, is the fuel and the playbook is the engine.

Below are seven core strategies often used in contracts for difference (CFDs) trading. With CFDs, you are not buying the underlying asset. You are speculating on the change in value. That means a trader can take a long position if the price rises, or a short position if it falls.

Seven strategies to understand first

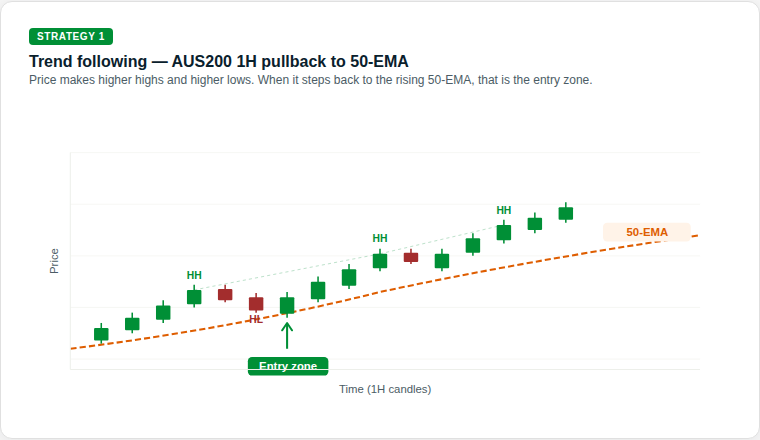

1. Trend following (the establishment play)

Trend following works on the idea that a market already in motion can remain in motion until it meets a clear structural obstacle. Some market participants view it as a chart-based approach because it focuses on the prevailing direction rather than trying to call an exact turning point.

The rationale: The aim is to identify a clear directional bias, such as higher highs and higher lows, and follow that momentum rather than position against it.

What traders look for: Exponential moving averages (EMAs), such as the 50-day or 200-day EMA, are commonly used to interpret trend strength, though indicators can produce false signals and are not reliable on their own.

How it works: The 50-period EMA can act as a dynamic support level that rises as price rises. In an uptrend, some traders watch for the market to make a new higher high (HH), then pull back towards the EMA before moving higher again. Each higher low (HL) may suggest buyers are still in control.

When price touches or comes close to the 50-period EMA during that pullback, some traders treat that area as a potential decision zone rather than assuming the trend will resume automatically.

What to watch: The sequence of HHs and HLs is part of the structural evidence of a trend. If that sequence breaks, for example if price falls below the previous HL, the trend may be weakening and the setup may no longer hold.

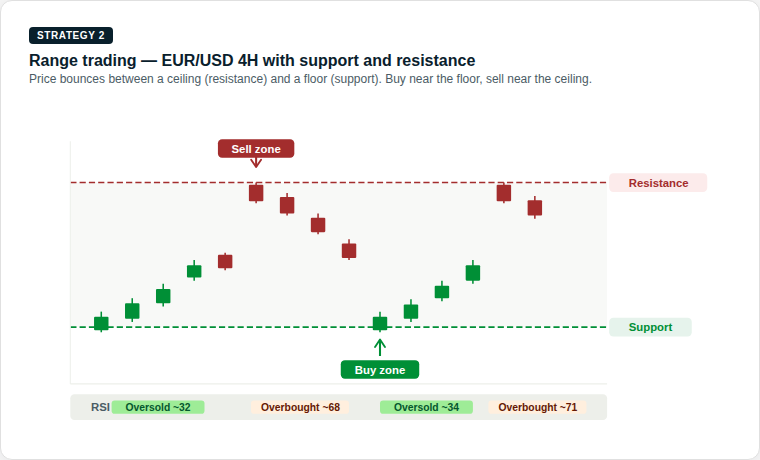

2. Range trading (the ping-pong play)

Markets can spend long stretches moving sideways. That creates a range, where buyers and sellers are in temporary balance. Range trading is built around this behaviour, focusing on moves near the bottom and top of an established range.

The rationale: Price moves between a floor, known as support, and a ceiling, known as resistance. Moves near those boundaries can help define the width of the range.

What traders look for: Some traders use oscillators such as the Relative Strength Index (RSI) to help judge whether the asset looks overbought or oversold near each boundary.

How it works: The support level is a price zone where buying interest has historically been strong enough to stop the market from falling further. The resistance level is where selling pressure has historically prevented further gains.

When price approaches support, some traders look for signs of a potential rebound. When it approaches resistance, they look for signs that momentum may be fading. RSI readings below 35 can suggest the market is oversold near support, while readings above 65 can suggest it is overbought near resistance.

What to watch: The main risk in range trading is a breakout, when price pushes decisively through either level with strong momentum. This may signal the start of a new trend and using a stop-loss just outside the range on each trade may help manage that risk.

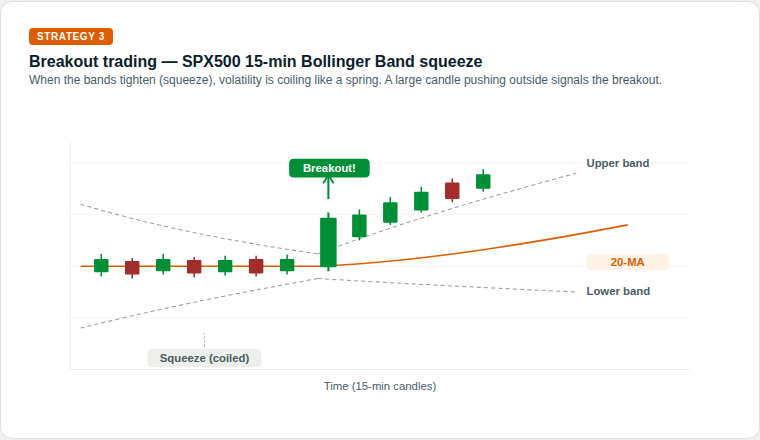

3. Breakouts (the coiled spring play)

Eventually, every range comes under pressure. A breakout happens when the balance shifts and price pushes through support or resistance. Markets alternate between periods of low volatility, where price moves sideways in a tight range, and high-volatility bursts where price can make a larger directional move.

The rationale: Quiet consolidation can sometimes be followed by a broader expansion in volatility. The tighter the compression, the more energy may be stored for the next move.

What traders look for: Bollinger Bands are often used to interpret changes in volatility. When the bands tighten, a squeeze is forming. Some market participants view a move outside the bands as a sign that conditions may be changing.

How it works: Bollinger Bands consist of a middle line, the 20-period moving average, and 2 outer bands that expand or contract based on recent price volatility. When the bands narrow and come close together, the squeeze, the market has been unusually calm.

This is often described as a coiled spring. Energy may be building, and a sharper move can follow. Some traders treat the first move through an outer band as an early clue on direction, rather than a definitive signal on its own.

What to watch: Not every squeeze leads to a powerful breakout. A false breakout occurs when price briefly moves outside a band, then quickly reverses back inside. Waiting for the candle to close outside the band, rather than entering mid-candle, can reduce the risk of being caught in a false move.

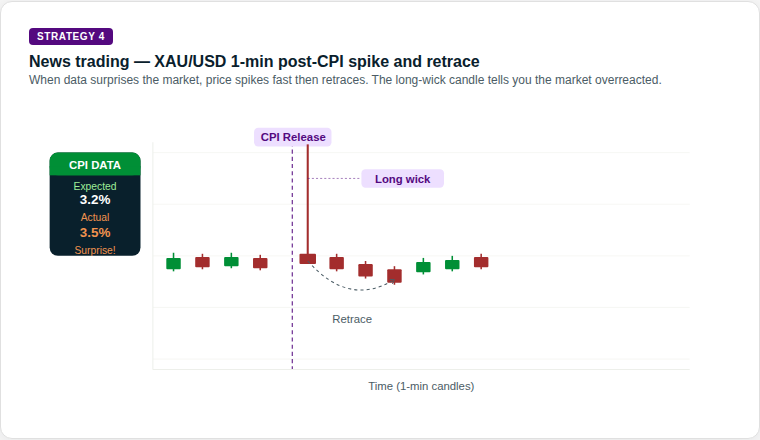

4. News trading (the deviation play)

This is event-driven trading. The focus is on the gap between what the market expected and what the data or headline actually delivered. Economic data releases, such as inflation figures (CPI), employment reports and central bank decisions, can cause sharp, fast moves in financial markets.

The rationale: High-impact releases, such as inflation data or central bank decisions, can force a fast repricing of assets. The bigger the surprise relative to expectations, the larger the move may be.

What traders look for: Traders often use an economic calendar to track timing. Some focus on how the market behaves after the initial reaction, rather than treating the first move as definitive.

How it works: Before the news, price may move in a calm, tight range as traders wait. When the data is released, if the actual reading differs significantly from the consensus expectation, repricing can happen fast.

Gold, for example, may spike sharply on a CPI reading that comes in above expectations. However, the candle can also print a very long upper wick, meaning price reached the spike high but was then rejected strongly. Sellers may step in quickly, and price may retrace. This spike-and-retrace pattern is one of the more recognisable setups in news trading.

What to watch: The direction and size of the initial spike do not always tell the full story. Wick length can offer an important clue. A long wick may suggest the initial move was rejected, while shorter wicks after a data release may indicate a more sustained directional move.

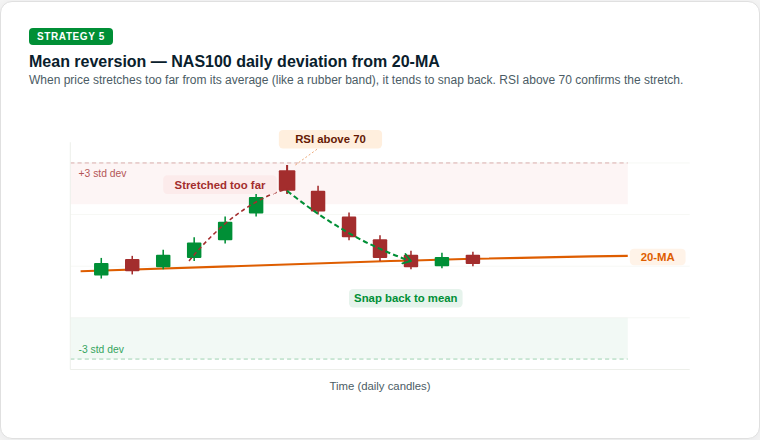

5. Mean reversion (the rubber-band play)

Prices can sometimes move too far, too fast. Mean reversion is built on the idea that an overextended move may drift back towards its historical average, like a rubber band pulled too tight, then snapping back.

The rationale: This is a contrarian approach. It looks for stretches of optimism or pessimism that may not be sustainable, and positions for a return to equilibrium.

What traders look for: A common example is price moving well away from a 20-day moving average (MA) while RSI also reaches an extreme reading. In that setup, traders watch for a move back towards the mean rather than a continuation away from it.

How it works: The 20-period MA represents the market's recent average price. When price moves into an extreme zone, such as more than 3 standard deviations above or below that average, it has moved a long way from its recent trend.

An RSI above 70 can suggest the market is stretched to the upside, while below 30 can suggest the same to the downside. Some mean reversion traders use these combined signals as a sign that a pullback towards the 20-period MA may be possible, rather than assuming the move will continue to extend.

What to watch: Mean reversion strategies can carry significant risk in strongly trending markets. A market can remain extended for longer than expected, and a position entered against the short-term trend can generate large drawdowns. Position sizing and clear stop-losses are critical.

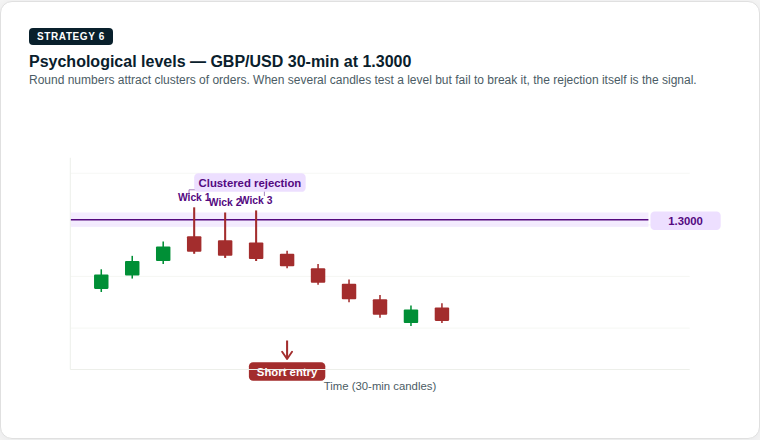

6. Psychological levels (the big figure play)

Markets are driven by people, and people tend to focus on round numbers. US$100, US$2,000 or parity at 1.000 on a currency pair can act as magnets. In financial markets, certain price levels can attract a disproportionate amount of buying and selling activity, not because of technical analysis alone, but because of human psychology.

The rationale: Large orders, stop-losses and take-profit levels can cluster around these big figures, which may reinforce support or resistance. This self-reinforcing behaviour is one reason these rejections can become meaningful for traders.

What traders look for: Traders often watch how price behaves as it approaches a round number. The market may hesitate, reject the level or break through it with momentum. Multiple wick rejections at the same level may carry more weight than a single one.

How it works: When price approaches a round number from below, some traders watch for long upper wicks, the thin vertical line above the candle body. A long upper wick means price reached that level, but sellers stepped in aggressively and pushed it back down before the candle closed.

One wick rejection may be notable. Three in a cluster may be more significant. Some traders use this accumulated rejection as part of the case for a short (sell) setup at that level.

What to watch: Psychological levels can also act as magnets in the opposite direction. If price breaks through with conviction, the level may then act as support. A decisive close above the level, rather than just a wick break, can be an early sign that the rejection setup is no longer holding.

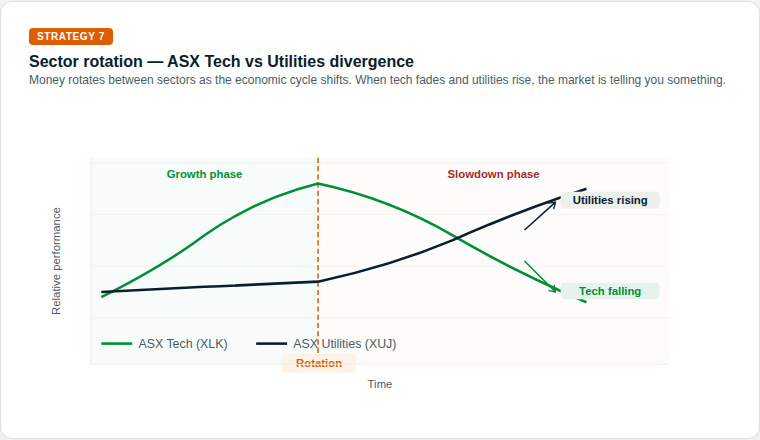

7. Sector rotation (the economic season play)

This is a macro strategy. As the economic backdrop changes, capital may move from higher-growth sectors into more defensive ones, and back again. Not all parts of the sharemarket move in the same direction at the same time.

The rationale: In a slowing economy, discretionary spending may weaken while demand for essential services can remain more stable. Investors may rotate capital between sectors accordingly.

What traders look for: With CFDs, some traders express this view through relative strength, taking exposure to a stronger sector while reducing or offsetting exposure to a weaker one.

How it works: During a growth phase, when the economy is expanding, investors tend to prefer growth-oriented sectors like technology. As the economic environment shifts, perhaps due to rising interest rates, slowing earnings or increasing recession risk, a rotation point may emerge.

In the slowdown phase, the pattern can reverse. Technology may weaken while utilities may strengthen, as investors move capital into defensive, income-generating sectors. Early signals can include relative underperformance in growth sectors combined with unusual strength in defensives.

What to watch: Sector rotation is not usually an overnight event. It typically unfolds over weeks to months. Tracking the ratio between two sectors, often shown in a relative strength chart, can make this shift visible before it becomes obvious in absolute price terms.

Why risk management is the engine of survival

The headline move is one thing. The market implication for your account is another. If you do not manage the mechanics, the strategy does not matter.

Because CFDs are traded on margin, a small market move may have an outsized impact on the account. If leverage is too high, even a minor wobble may trigger a margin call or automatic position closure, depending on the provider's terms. This is not a theoretical risk. It is a common reason new traders lose more than they expected on a trade that was directionally correct.

The market does not always move in a straight line. Sometimes, price gaps from one level to another, especially after a weekend or major news event and in those conditions, a stop-loss may not be filled at the exact requested price. That is known as slippage. It is one reason large positions may carry additional risk into major announcements.

Bottom line

The vehicle is powerful, but the playbook is what helps keep you on the road.

The obvious trade is often already priced in. What matters more is understanding which market condition is in front of you. Is it trending, ranging, breaking out or simply reacting to a headline?

Readers assessing leveraged products often focus on position sizing, risk limits and product disclosure before deciding whether the product is appropriate for them. The headlines will keep changing. The maths of risk management does not.

Ready to trade beyond the majors?

Open an account · Log in

Disclaimer: This article is general information only and is intended for educational purposes. It explains common trading concepts and market behaviours and does not constitute financial product advice, a recommendation, or a trading signal. Any examples are illustrative only and do not take into account your objectives, financial situation or needs. CFDs are complex, leveraged products that carry a high level of risk. Before acting, consider the PDS and TMD and whether trading CFDs is appropriate for you. Seek independent advice if needed. Past performance is not a reliable indicator of future results.

Last week was as consequential as advertised. The RBA hiked, the Fed held, and markets barely had time to process any of it before reports emerged that Israel had struck Iran's South Pars gas field.

The week ahead brings fewer central bank decisions, but it may be just as important for markets. Flash PMIs will offer the first broad read on whether the war is already showing up in business confidence. Australia's February CPI is the domestic data point that matters most for the RBA's next move. And the oil market remains the dominant macro variable.

Quick facts

- Brent crude spiked above $110 per barrel after Israel struck Iran's South Pars gas field for the first time.

- Flash PMIs for Australia, Japan, the eurozone, UK, and the US all land Tuesday.

- Australia's February CPI lands Wednesday, the first inflation read since the back-to-back RBA hikes.

Oil: From crisis to emergency

The oil situation deteriorated significantly last week. Brent crude has now surged roughly 80% since the war began on 28 February.

The 18 March strike on Iran's South Pars gas field was the first time upstream oil and gas infrastructure has been targeted.

Iran responded to the strike by threatening to target facilities across Saudi Arabia, the UAE and Qatar. If any of these threats are executed, the global oil shock would escalate from a supply disruption to a direct attack on the region's production capacity.

Analysts are now saying $150 Brent is achievable and $200 is not outside the realm of possibility. The 1970s Arab oil embargo resulted in a quadrupling of prices, and the current shock is already being described in those terms by senior energy executives.

For markets this week, oil is the dominant variable. Any signal of ceasefire, diplomatic progress or resumed Hormuz shipping could likely trigger a correction in oil prices. Any Iranian strike on Gulf infrastructure could send them higher.

Monitor

- Daily vessel transit numbers through the Strait of Hormuz.

- Iranian retaliation against Gulf infrastructure, a strike on Saudi or UAE facilities would be a major escalation.

- When and how American and European IEA reserves reach the market.

- Qatar's South Pars disruption is affecting the European LNG market.

- Trump statements that could cause intraday oil price movement.

Global Flash PMIs: The first read on an economy at war

Tuesday delivers the S&P Global flash PMI estimates for March across every major economy simultaneously.

This will be the first data set to capture how manufacturers and services firms are responding to $100+ oil, the Strait of Hormuz blockade, and the broader uncertainty created by the war in the Middle East.

The key question for each economy is whether the oil price surge and war uncertainty have dented business confidence, suppressed new orders or pushed input price indices to new multi-year highs.

Given that oil crossed $100 before the survey window closed for most economies, input cost readings could be significantly elevated.

Key dates

- S&P Global Flash Australia PMI: Tuesday 24 March, 9:00 am AEDT

- S&P Global Flash Japan PMI: Tuesday 24 March, 11:30 am AEDT

- HSBC Flash India PMI: Tuesday 24 March, 4:00 pm AEDT

- HCOB Flash France PMI: Tuesday 24 March, 7:15 pm AEDT

- HCOB Flash Germany PMI: Tuesday 24 March, 7:30 pm AEDT

- HCOB Flash Eurozone PMI: Tuesday 24 March, 8:00 pm AEDT

- S&P Global Flash UK PMI: Tuesday 24 March, 8:30 pm AEDT

- S&P Global Flash US PMI: Wednesday 25 March, 12:45 am AEDT

Monitor

- Input price components for any multi-year highs across manufacturing and services.

- Business confidence indices for how much the war shock has dented forward expectations.

- New orders as an indicator for future output; a sharp fall could signal demand destruction is underway.

- US composite PMI: already the weakest of major economies in February, another soft reading could raise growth alarm bells.

Hormuz crisis explained

Australia: Is another hike coming?

The RBA hiked for the second meeting in a row on 17 March, lifting the cash rate to 4.10% in a narrow 5-4 vote.

Governor Bullock described it as a "very active discussion" where the direction of policy was not in question, only the timing.

This week will see the release of February's CPI as the first read to capture any of the oil shock. The trimmed mean, which strips out volatile items including fuel, will be the number the RBA watches most closely. A reading above 3.5% could cement the case for a May hike. A softer result could revive the argument for a pause.

ANZ and NAB have both stated expectations of a third hike in May, taking the cash rate to 4.35%.

Key dates

- ABS Consumer Price Index (CPI): Wednesday 25 March, 11:30 am AEDT

Monitor

- Trimmed mean inflation as the RBA's preferred measure.

- Fuel and energy components that could separate the oil shock from domestic price pressure.

- Housing and services inflation as sticky components driving the RBA's long-run concern.

Ready to trade beyond the majors?

Open an account · Log in

Asia dominates the global semiconductor supply. Five companies, spanning Taiwan, South Korea, and Japan, sit at the critical juncture of the AI buildout, controlling everything from fabrication to the equipment that makes chips possible.

Quick facts

- TSMC delivered $90 billion in revenue in 2024, with a 59% gross margin and shares up 55% in 2025.

- Advantest shares doubled (+102%) in 2025 as AI-driven chip testing demand surged.

- SK Hynix is Nvidia's primary HBM supplier, positioning it at the centre of the AI accelerator boom.

1. Taiwan Semiconductor Manufacturing Co. (TSM)

TSMC is the world's largest contract chip manufacturer, producing advanced semiconductors for Apple, Nvidia, AMD, and Qualcomm. As a pure-play foundry, it leads in 5-nanometer (5nm) and 3- nanometer (3nm) chip production, with smaller nodes in development.

The company posted $90 billion in revenue for 2024 with a 59% gross margin and 36% return on equity.

Shares delivered a total return of 55% in 2025, with analysts forecasting a further ~30% revenue increase in 2026, underpinned by its $100 billion US expansion programme.

The key risk for the company is its geopolitical exposure, with Taiwan Strait tensions remaining the sector's most-watched tail risk.

What to watch

- US expansion progress: Any delays, cost blowouts, or political friction concerning TSMC's $100 billion Arizona investment could weigh on sentiment.

- Customer order visibility: Watch for any guidance updates from Apple, Nvidia, or AMD on chip orders, as TSMC's revenue is highly concentrated among a handful of clients.

- Geopolitical developments: Any escalation of Taiwan Strait tensions could trigger sharp moves regardless of fundamentals.

- Next-node ramp: Progress on 2nm production and yield rates will be a key signal for TSMC's ability to maintain its technology lead.

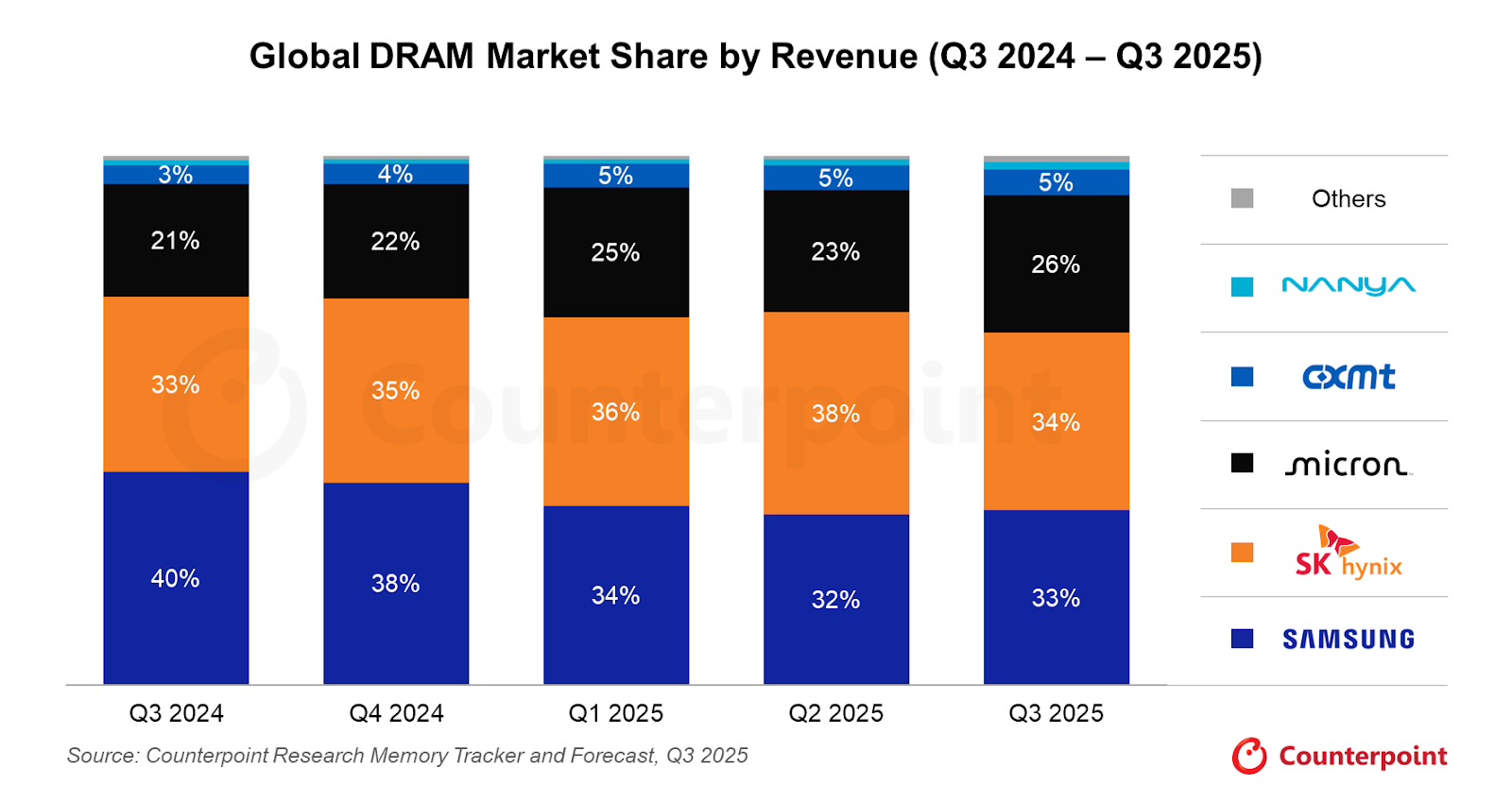

2. Samsung Electronics (KR:005930)

Samsung is one of the few companies globally that both designs and fabricates chips at scale. It competes across DRAM, NAND flash, and logic chip segments, and remains a core supplier to global tech giants.

Samsung's wide scope is a strength, but also a complexity. Its memory division faces margin pressure from inventory cycles, while its foundry business continues to lag TSMC in leading-edge yields.

The AI-driven memory boom may provide a tailwind, though execution in HBM production has been slower than local rival SK Hynix.

What to watch

- HBM qualification progress: Samsung has been working to qualify its HBM3E chips with Nvidia. Any confirmation of a major supply win could be a meaningful catalyst.

- Memory pricing trends: DRAM and NAND spot prices could be an indicator of Samsung's margin trajectory.

- Foundry yield improvements: Samsung's logic foundry business has struggled with yields at advanced nodes; any credible progress here could re-rate the division.

- Management guidance: Following a period of earnings volatility, clarity on capex plans and divisional targets at upcoming results will be closely watched.

3. Advantest (ATEYY)

Tokyo-based Advantest makes testing equipment used to verify chips meet performance and quality standards.

It supplies to Samsung, Intel, Nvidia, Qualcomm, and Texas Instruments, allowing it to benefit from chip industry growth broadly, regardless of which foundry wins market share.

Advantest shares doubled in 2025 (+102%), and it raised its sales forecast by 21.8% and earnings forecast by 70.6% for the year ending March 2026.

What to watch

- Order backlog updates: Any contraction in Advantest's backlog could be an early warning sign after the strong 2025 run.

- AI chip testing demand: As chips grow more complex, testing time per chip increases. Monitor whether AI accelerator volumes from TSMC and Samsung start to drive outsized testing demand.

- FY2026 guidance: The next forecast update will be critical in confirming whether 2025's upgrade cycle has further to run.

4. Tokyo Electron (T:8035)

Tokyo Electron is among the world's largest suppliers of semiconductor production equipment, specialising in deposition, etching, and cleaning tools.

Every major chipmaker, including TSMC, Samsung, and SK Hynix, depends on TEL's systems to scale production.

As chipmakers invest billions to expand capacity, TEL's order book grows. The risk lies in potential US export restrictions on advanced equipment sales to China, which remains one of the primary revenue segments for the company.

What to watch

- US export control policy: China accounts for a significant portion of TEL's revenue. Any tightening of equipment export rules is the most immediate risk to watch.

- Chipmaker capex announcements: TSMC, Samsung, and SK Hynix's capital expenditure plans for 2026 directly translate into equipment orders. Any cuts could flow through to TEL's order book.

- New tool adoption cycles: Monitor whether TEL's next-generation deposition and etch tools are being adopted at leading-edge fabs.

5. SK Hynix (KR:000660)

SK Hynix is the world's second-largest memory chip maker and has emerged as arguably the clearest AI-era beneficiary in the memory space.

It is Nvidia's primary supplier of High Bandwidth Memory (HBM) chips, the specialised memory used in AI accelerators like the H100 and B200.

HBM demand has driven a dramatic re-rating of SK Hynix's revenue profile and market standing. With AI infrastructure spending showing little sign of slowing heading into 2026, the company's HBM franchise could remain a key differentiator.

However, capacity constraints and the risk of Samsung and Micron closing the HBM gap are the primary concerns to watch.

What to watch

- Nvidia supply relationship: Any shift in Nvidia's supplier mix toward Samsung or Micron could be a key risk event.

- HBM4 development: The race to next-generation HBM is already underway. Watch for updates on SK Hynix's HBM4 readiness and whether it can maintain its lead.

- Conventional memory pricing: SK Hynix still derives meaningful revenue from standard DRAM and NAND. Spot price trends could be a gauge of the broader memory cycle.

Bottom line

TSMC, SK Hynix, Samsung, Advantest, and Tokyo Electron collectively control the chokepoints of the AI buildout.

The expected increase in AI infrastructure may support demand, but investors should weigh the risks carefully.

Geopolitical exposure, US export restrictions, and the pace of HBM competition could all move the needle.

Ready to trade beyond the majors?

Open an account · Log in

So, here’s the thing...

If you have been following the tech story for the last decade, you have been trained to look at a very specific, very small patch of real estate in Northern California. But as we sit here in early 2026, the "connect-the-dots" moment for investors is this: the AI trade has stopped being about shiny software demos in Palo Alto and has started being about the physical industrialisation of compute.

Want to know more? Read our 2026 AI playbook

What changed, and why it matters

We have entered the "Year of Proof". The world’s largest companies, the hyperscalers, are projected to spend a staggering US$650 billion on capital expenditures this year. But here’s the part most people miss: that money is not staying in Silicon Valley. It’s flowing to the "picks and shovels" players in Idaho, Washington, Colorado and even overseas.

If you want to understand where the actual return on investment (ROI) may be landing this earnings season, you have to look outside the 650 area code. The shift from AI hype to AI industrialisation is changing the map.

Five companies · AI infrastructure play · 2026

The full AI stack: from capex to consulting

Infrastructure builders compared to the implementation bridge across the AI value chain

Hyperscaler CapEx: Early 2026 analyst estimates, midpoint of ranges. Amazon approx. 100% YoY, Alphabet approx. 100%, Meta approx. 87%, Microsoft approx. 50%.

Accenture: Cumulative advanced AI bookings $11.5B through Q1 FY2026. Q1 AI bookings $2.2B (up 76% YoY), AI revenue $1.1B (up 120% YoY) across 1,300+ clients.

Five companies shaping the next phase of AI

Micron Technology (MU), Boise, Idaho

Micron is the "memory backbone" of the current cycle. While everyone was watching the chip designers, many overlooked the fact that AI chips are far less useful without high-bandwidth memory (HBM). Micron is currently viewed by some analysts as a strong buy because its capacity is reportedly sold out through the end of 2026. Analysts are also eyeing a 457% jump in earnings per share (EPS) as the memory cycle reaches what some describe as a robust peak.

Microsoft (MSFT), Redmond, Washington

Microsoft is the enterprise backbone of this transition. It has moved beyond simple chatbots and is now building what analysts call "Intelligence Factories". While the stock has faced pressure recently over capacity constraints, underlying demand for Azure AI is reportedly still running ahead of capacity. The broader bull case is that Microsoft is moving into "Agentic AI", systems that do not just talk to users but may also execute multi-step business workflows.

Which Asian companies are betting big on artificial intelligence?

Amazon (AMZN), Seattle, Washington

Amazon is playing a long-term game of vertical integration. To reduce its reliance on expensive third-party hardware, it’s building its own AI chips in-house. Amazon Web Services (AWS) remains the primary driver of profitability, and the company is using its retail data to train specialised models that many Silicon Valley start-ups may struggle to replicate.

Palantir Technologies (PLTR), Denver, Colorado

If Micron provides the memory and Microsoft the platform, Palantir provides the "operating system" for the modern AI factory. The company has posted strong momentum, with US commercial sales recently growing 93% year over year. It’s often framed as a bridge between raw data and corporate profitability, which remains a key focus for investors in 2026.

Accenture (ACN), Dublin, Ireland

You cannot just "plug in" AI. Businesses often need to redesign processes around it, and that’s where Accenture comes in.

The company is viewed as an implementation bridge, with one analyst arguing that "GenAI needs Accenture" to move from pilot programs to production though the cautionary angle is that the AI story has not fully excited investors here yet because consulting revenue can take longer to show up than chip sales.

What could happen next?

The chart maps the three time horizons likely to shape the next phase of the AI industrialisation trade.

In the near term, markets are still reacting to chipmaker earnings, guidance, and any signs of capacity strain. Over the next month, attention shifts to the real-world inputs behind AI growth, especially power, financing, and infrastructure. By the 60-day window, the key question is whether AI spending is broadening into a wider market re-rating or running ahead of near-term returns.

Across all three periods, the focus is the same: proof. Investors are looking for signs that AI capital expenditure is translating into real demand for energy, land, and industrial capacity. That is why updates from companies tied to power and data centre buildout matter more than ever.

Scenario planning · March 2026

What could happen next

Three time horizons, three scenarios to watch across the AI industrialisation cycle

Chipmaker reports

Possible

Market volatility continues as traders digest the latest reports from chipmakers like Micron

Upside scenario

"Bulletproof" guidance from remaining infrastructure names triggers a sector-wide relief rally

Watch for

Any mention of "capacity constraints" or "supply bottlenecks" in earnings calls

Energy and rates

Possible

Focus shifts to "real economy" energy players like NextEra that power the data centres

Downside scenario

Rising oil prices from Middle East conflict act as a tax on tech margins, rotating into defensives

Action point

Monitor Fed language on rates. Higher for longer makes $650B capex bills far more expensive to finance

The great dispersion

Possible

Market rewards companies with real AI revenue and punishes those still stuck in experimentation

Upside scenario

NextEra Energy (NEE) data centre announcements in late April/May trigger a utility renaissance rally

Downside scenario

An "air pocket" in profits occurs where debt-funded investment outpaces revenue gains

Watch

May reports from Texas Pacific Land (TPL) — is data centre land demand still "red hot"?

Action point

Review your portfolio for geographic diversity. The AI story is now a global power race

The psychological trap

The emotional trap many traders fall into right now is recency bias. You have seen NVIDIA and the "Magnificent 7" win for so long that it feels like they are the only way to play this. But the "obvious" trade is often the one that has already been priced in. Before acting, ask yourself: "Am I buying this stock because I understand its role in the physical AI supply chain, or because I’m afraid of missing the next leg of a rally that started two years ago?"

Ready to trade beyond the majors?

Open an account · Log in

Disclaimer: This content is general information only and should not be relied on as personal financial advice or a recommendation to buy, sell, or hold any financial product. References to companies or themes, including AI-related stocks, are illustrative only. Share and derivative markets can move sharply, and concentrated sectors such as AI and technology may experience elevated volatility, valuation risk, and liquidity risk. If you trade derivatives such as CFDs, leverage can magnify both gains and losses. Past performance is not a reliable indicator of future performance.

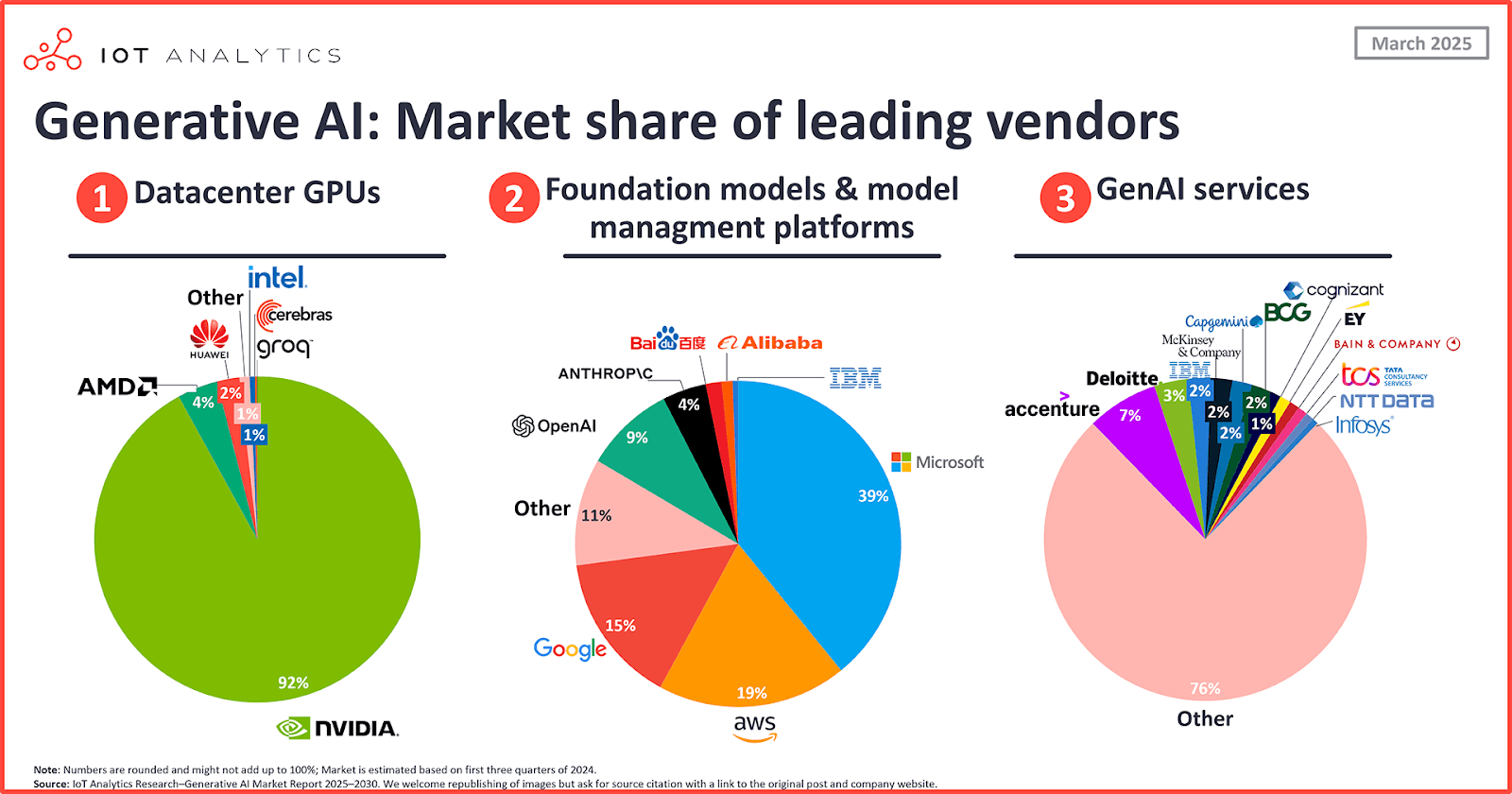

While all eyes are on the US AI narrative dominated by Nvidia, Microsoft, and Google, Asia has quietly been moving on AI and is home to some of the world’s most aggressive AI bets.

Quick facts

- SoftBank has committed $41 billion to OpenAI, securing approximately an 11% ownership stake.

- Alibaba plans to invest more than $50 billion in AI infrastructure over the coming years.

- Baidu's Core AI-powered business revenue grew 48% year over year in Q4, with ~70% of search results now AI-generated.

1. SoftBank Group (TYO: 9984)

SoftBank is the most AI-committed company in Asia by capital deployed and ambition. CEO Masayoshi Son has declared the company in "total offence mode," having completed a $41 billion investment into OpenAI for approximately an 11% ownership stake.

Son has also launched a $100 billion initiative aimed at building a vertically integrated AI semiconductor champion (Project Izanagi), repositioning SoftBank as an "AI-era industrial holding company."

SoftBank's fortunes are now deeply tied to the success of OpenAI and Son's ability to execute his semiconductor plan that puts it in direct competition with established players.

What to monitor

- OpenAI's trajectory: Any shift in OpenAI's competitive position, valuation, or path to profitability has direct implications for SoftBank's balance sheet.

- Project Izanagi progress: Watch for partner announcements, funding milestones, and whether Son can attract the engineering and manufacturing talent needed.

- Arm Holdings performance: SoftBank also has a listed stake in Arm. Arm's data centre and AI chip licensing momentum is worth tracking.

- Debt levels and Vision Fund exposure: SoftBank carries significant leverage. Rising interest rates or a correction in AI valuations could pressure the group's net asset value.

2. Alibaba Group (BABA)

Alibaba has committed more than US$50 billion to AI infrastructure, making it one of the largest AI capex programmes in the world.

Its Qwen family of large language models underpins a rebuilt AI-focused cloud platform, and the company has partnered with Nvidia on physical AI projects.

Alibaba Cloud is also the leading cloud provider in China. The key commercial question is whether Alibaba's can convert this cloud leadership into durable revenue growth.

However, it will have to navigate ongoing regulatory scrutiny in China and competition from local rivals like Huawei and ByteDance.

What to monitor

- Cloud AI revenue growth: The clearest signal of whether the $50 billion investment is translating into commercial traction.

- Qwen model adoption: Enterprise and developer uptake of the Qwen model family could be an indicator of Alibaba's AI platform stickiness.

- Regulatory environment: Beijing's approach to large tech platforms and any renewed regulatory action could disrupt execution and sentiment.

- US-China tech tensions: Nvidia partnership activity and access to advanced AI chips could be affected by further export controls.

3. Baidu (BIDU)

Baidu has made the most visible AI transformation of any company on this list. It has released a 2.4 trillion parameter omni-modal model (ERNIE 5.0) with approximately 70% of its search results now delivered as AI-generated rich media.

Beyond search, its Apollo Go robotaxi service is now partnering with Uber to expand into Dubai and the UK.

Its Core AI-powered business generated RMB 11.3 billion in Q4 revenue, up 48% YoY. The question now is whether that momentum is sustainable and whether the robotaxi business can scale economically.

What to monitor

- ERNIE monetisation: Watch for updates on enterprise API revenue and advertising yield improvements driven by AI-generated search.

- Apollo Go expansion: Rider volume growth and cost per ride will indicate whether unit economics are improving.

- Search market share: Competition from ByteDance and emerging AI-native search alternatives in China is a potential structural risk.

4. Tencent Holdings (HK: 0700)

Tencent's AI play is to allocate its GPU capacity to itself. This allows it to convert AI directly into efficiency gains across its ecosystem.

With WeChat's 1.4 billion users providing an unmatched data engine, Tencent is embedding AI across gaming, payments, cloud, and search in a way that is difficult to replicate.

This approach also offers greater resilience against AI chip export restrictions, since the compute stays internal.

The AI upside here is arguably underappreciated because it is embedded rather than a separate segment, which could also mean the market may find it harder to isolate and value that contribution.

What to monitor

- Advertising revenue trends: The most measurable near-term AI benefit is from ad targeting improvements translating into sustained advertising revenue growth.

- WeChat ecosystem AI integration: Watch for new AI-native features within WeChat, including search, mini-programs, and payments, as signals of platform deepening.

- Regulatory and geopolitical risk: Tencent operates under ongoing scrutiny from Chinese regulators and faces restrictions in some Western markets.

5. Kakao (KRX: 035720)

Kakao is South Korea's dominant AI and internet platform, operating KakaoTalk, which is used by approximately 95% of South Koreans.

It is one of the most aggressively AI-focused non-Chinese tech companies in Asia, investing heavily in LLM development and AI-native services.

The domestic dominance of KakaoTalk provides a captive distribution platform for AI products in a way few companies outside China can match. The key question is whether Kakao can monetise that distribution advantage before global competitors close the gap.

What to monitor

- KakaoAI product rollouts: New AI-native features within KakaoTalk and Kakao's broader service suite are the most direct signal of commercial AI progress.

- Cloud division growth: Kakao's cloud business is the infrastructure layer for its AI ambitions. Revenue growth and enterprise customer additions are key metrics.

- LLM competitive positioning: Monitor how Kakao's models benchmark against global and regional peers, and whether Korean enterprise customers are adopting them at scale.

- Corporate governance: Kakao has faced governance-related scrutiny in recent years; any developments here could affect sentiment independently of AI progress.

Bottom line

Asia's AI landscape is far more complicated than a simple "follow the AI spend" narrative suggests.

China's top companies are innovating rapidly but operate under regulatory and geopolitical constraints. Japan's SoftBank is making the biggest single bet, but at a level of concentration risk that demands scrutiny. And South Korea's Kakao offers a differentiated, lower-geopolitical-risk angle.

The AI push in Asia is real. But the range of outcomes across these five names is wide, making it pivotal to understand each company's specific exposure and risk profile, not just its AI narrative.

The war in Iran is increasingly shifting from a regional conflict into a global energy shock, as disruption in the Strait of Hormuz threatens the oil market at its most critical chokepoint.

Key takeaways

- Around 20 million barrels per day (bpd) of oil and petroleum products normally pass through the Strait of Hormuz between Iran and Oman, equal to about one-fifth of global oil consumption and roughly 30% of global seaborne oil trade.

- This is a flow shock, not an inventory problem. Oil markets depend on continuous throughput, not static storage.

- If the disruption persists beyond a few weeks, Brent could shift from a short-term spike to a broader price shock, with stagflation risk.

The world’s most critical oil chokepoint

The Strait of Hormuz handles roughly 20 million barrels per day of oil and petroleum products, equal to about 20% of global oil consumption and around 30% of global seaborne oil trade. With global oil demand near 104 million bpd and spare capacity limited, the market was already tightly balanced before the latest escalation.

The strait is also a critical corridor for liquefied natural gas. Around 290 million cubic metres of LNG transited the route each day on average in 2024, representing roughly 20% of global LNG trade, with Asian markets the main destination.

The International Energy Agency (IEA) has described Hormuz as the world’s most important oil transit chokepoint, noting that even partial interruptions may trigger outsized price moves. Brent crude has moved above US$100 a barrel, reflecting both physical tightness and a rising geopolitical risk premium.

Tankers idle as flows slow

Shipping and insurance data now point to strain in real time. More than 85 large crude carriers are reported to be stranded in the Persian Gulf, while more than 150 vessels have been anchored, diverted or delayed as operators reassess safety and insurance cover. That would leave an estimated 120 million to 150 million barrels of crude sitting idle at sea.

Those volumes represent only six to seven days of normal Hormuz throughput, or a little more than one day of global oil consumption.

A market built on flow, not storage

Oil markets function on continuous movement. Refineries, petrochemical plants and global supply chains are calibrated to steady deliveries along predictable sea lanes. When flows through a chokepoint that carries roughly one-fifth of global oil consumption and around 30% of global seaborne oil trade are interrupted, the system can move from equilibrium to deficit within days.

Spare production capacity, largely concentrated within OPEC, is estimated at only 3 million to 5 million bpd. That falls well short of the volumes at risk if Hormuz flows are severely disrupted.

Oil market analysis

How long do idle tankers last?

135M idle barrels — days of cover against each demand benchmark

vs. Strait of Hormuz daily flow (20M bbl/day)

vs. Global oil consumption (104M bbl/day)

vs. US Strategic Petroleum Reserve release (1M bbl/day)

135M

idle barrels on tankers (midpoint of 120–150M range)

~33%

of daily Hormuz flow that is idle storage, not transit

<31 hrs

is all idle storage against global daily consumption

Scenarios for the weeks ahead

Market trajectories now hinge on the duration and severity of the disruption.

Short disruption, 1 to 2 weeks

If tanker traffic resumes within 1 to 2 weeks, the shock may show up as a sharp but ultimately reversible spike.

Cumulative supply loss would remain relatively limited, while inventories and strategic stocks may partly bridge the shortfall. In that scenario, Brent could trade in roughly the US$95 to US$110 range as traders price temporary disruption and elevated risk premia.

Extended disruption, 2 to 4 weeks

Beyond a fortnight, the cumulative loss becomes more material.

A 2 to 4 week disruption affecting up to 20 million bpd could imply roughly 280 million to 560 million barrels of lost supply. Commercial inventories, floating storage and strategic reserves may then begin to erode more visibly. In that scenario, Brent could shift toward the US$110 to US$130 range, while higher fuel costs may begin feeding into transport and industrial production.

These price ranges are scenario-based and indicative, not forecasts.

If the war ends within four weeks

A ceasefire or credible de-escalation within roughly four weeks would likely trigger a sharp reversal in oil markets, though not an instant reset to pre-crisis levels.

Initially, the unwinding of geopolitical risk premia and the normalisation of tanker traffic could push Brent lower, potentially into the US$80 to US$95 range as speculative and hedging positions are reduced.

Assuming flows are fully restored and further disruptions are avoided, prices could gradually trend back toward the low US$70s over subsequent months, broadly consistent with projections that show inventories rebuilding once supply regains a small surplus over demand.

Inflation risks and macro spillovers

The inflationary impact of an oil shock typically arrives in waves. Higher fuel and energy prices may lift headline inflation quickly as petrol, diesel and power costs move higher.

Over time, higher energy costs may pass through freight, food, manufacturing and services. If the disruption persists, the combination of elevated inflation and slower growth could raise the risk of a stagflationary environment and leave central banks facing a difficult trade-off.

No easy offset, a system with little slack

What makes the current episode particularly acute is the lack of slack in the global system.

Global supply and demand near 103 million to 104 million bpd leave little spare cushion when a chokepoint handling nearly 20 million bpd, or about one-fifth of global oil consumption, is compromised. Estimated spare capacity of 3 million to 5 million bpd, mostly within OPEC, would cover only a fraction of the volumes at risk.

Alternative routes, including pipelines that bypass Hormuz and rerouted shipping, can only partly offset lost flows, and usually at higher cost and with longer lead times.

Bottom line

Until transit through the Strait of Hormuz is restored and seen as credibly secure, global oil flows are likely to remain impaired and risk premia elevated. For investors, policymakers and corporate decision-makers, the core question is whether oil can move where it needs to go, every day, without interruption.

Ready to trade beyond the majors?

Open an account · Log in

Any scenarios, price ranges or market views in this article are illustrative only and should not be relied on as forecasts, guarantees or trading recommendations. Geopolitical events can cause sudden volatility, reduced liquidity and sharp price movements across oil, forex and CFD markets, and trading in these conditions carries a high risk of loss.

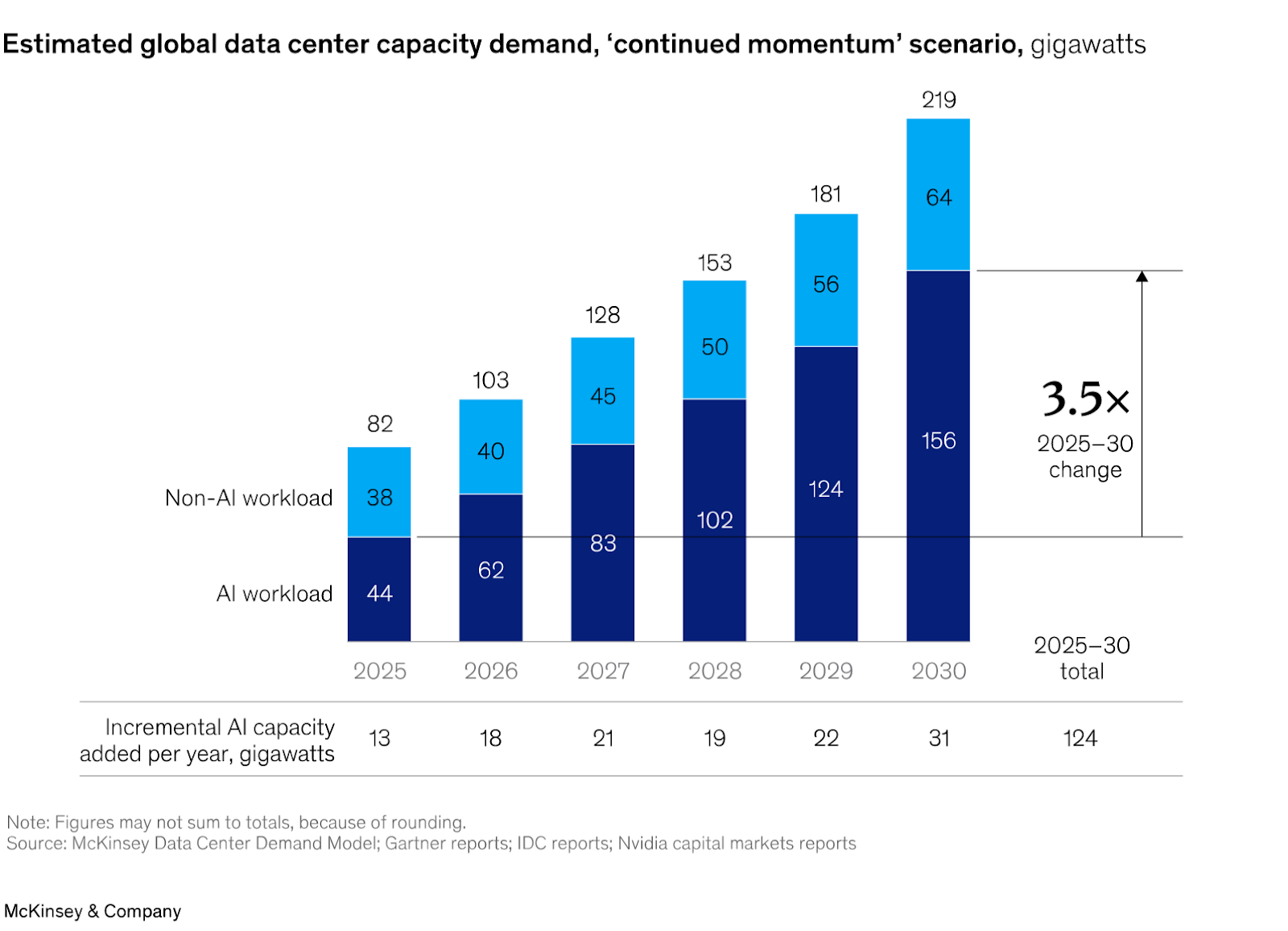

After three consecutive years in which mega-cap AI-linked names carried the Nasdaq, the mix of winners may be starting to change.

2026 is the "show me the money" year. Any hint of doubt about whether tech companies were correct to spend nearly US$700 billion on AI last year could have a major impact on market sentiment.

Quick facts

- Global AI capex is projected to exceed US$600 billion in 2026.

- The total addressable market (TAM) for AI data centre systems is estimated to exceed US$1.2 trillion by 2030.

- Nvidia, Microsoft and TSMC are all trading below analyst fair value estimates, despite surging revenues.

- Broadcom's AI chip division is targeting US$100 billion in AI revenue by 2027.

What is powering the AI trade?

Multiple macro forces are likely to underpin the AI investment theme through 2026. The direction of US interest rates, the scale of AI infrastructure spending and the geopolitical backdrop are all likely to matter.

Rates and valuations

The Federal Reserve delivered 75 basis points (bps) of rate cuts in 2025, and markets expect another 50 bps in 2026. Lower rates can reduce the discount applied to future tech earnings and typically support growth stocks, including AI-linked names.

Infrastructure spending and earnings expectations

On the spending side, Nvidia CEO Jensen Huang has said data centre operators could spend up to US$4 trillion annually by 2030, and AI capital spending is projected to reach US$571 billion in 2026 alone.

However, markets appear to have already priced in much of this optimism. Analysts are projecting 14% to 16% annual earnings per share (EPS) growth in 2026. That would require S&P 500 stocks outside the Magnificent 7 to roughly double the pace of earnings growth recorded in 2025.

Geopolitics and export controls

Geopolitics could also shape the outlook. US-China export controls on AI chips, along with reduced access to key international buyers, could weigh on data centre growth projections.

Top AI-linked stocks

Nvidia (NVDA)

Nvidia remains the clearest expression of the AI trade. It holds a wide economic moat thanks to its market leadership in GPUs, hardware, software, and networking tools.

Goldman Sachs and Morgan Stanley both carry price targets near $250 on NVDA, with Goldman's call based on a 2027 revenue forecast of over $380 billion. Bank of America sits in the $275 camp, effectively pricing in more AI upside on 2027 earnings.

At 21.6 times forward earnings, Nvidia is now trading below the broader S&P 500's multiple. Key risks include the overhang from US–China export restrictions and any softening in data centre capex guidance from major cloud providers.

Microsoft (MSFT)

Microsoft is down around 25% from its all-time high. During the second quarter of fiscal year 2026, Azure's revenue increased 39% year over year, and the company holds a US$625 billion backlog of contracted usage still to come.

The gap between the stock's recent performance and its underlying revenue growth has drawn attention from analysts, though elevated valuations across the broader tech sector remain a risk to watch.

Broadcom (AVGO)

While Nvidia makes broad-purpose GPUs, Broadcom is winning business by going bespoke, designing custom AI chips tailored specifically to the needs of individual hyperscalers like Google and Meta.

During Q1 of FY2026, Broadcom's AI semiconductor division grew at a 106% pace to US$8.4 billion, and by the end of 2027 it expects its AI chip revenue to reach more than US$100 billion.

Broadcom trades at a significant premium to the broader market, which could amplify any downside if growth expectations are not met.

TSMC (TSM)

Almost every major AI chip is manufactured by TSMC. The company holds approximately 70% market share in chip foundry, making it the single most critical piece of infrastructure in the entire AI supply chain.

TSMC sales are projected to increase by 30% in 2026, with gross margins expected to remain above 60% as new fabrication capacity comes online.

The primary risk is geopolitical: any escalation in Taiwan Strait tensions could weigh heavily on the stock regardless of its underlying fundamentals.

Vertiv (VRT)

Less prominent than the semiconductor giants, Vertiv provides the power management, cooling, and data centre infrastructure that keeps AI hardware running.

Nvidia, Broadcom, and Vertiv sit at different points in the AI build-out, including compute, custom silicon, networking and physical infrastructure.

Vertiv's revenue is tied to overall AI capex rather than any single chip maker, which gives it a different risk profile to the names above.

Corning (GLW)

Corning's stock rose 84% in 2025 thanks to surging demand from data centres for its fibre optic cables. Its optical communications segment has grown 69% YoY.

At a Price-to-Earnings (P/E) ratio of roughly 37x, Corning trades at a discount to Nvidia and Broadcom while still carrying direct exposure to AI infrastructure spending. However, its valuation depends heavily on continued capex from the major hyperscalers.

US market drivers for March 2026

AI trades beyond the headline stocks

Energy and utilities

Training large-scale AI models is extraordinarily energy-intensive. A typical 1 gigawatt AI data centre facility requires upwards of US$60 billion in capital expenditure, with roughly half going directly to hardware. Utilities exposed to data centre power demand could also be affected by the AI build-out.

International spillover

South Korea's Kospi surged 76% in 2025 due to AI-linked chipmakers like SK Hynix. Japan's Topix, Germany's DAX, and the UK's FTSE 100 also saw gains of more than 20%. Memory supplier Kioxia was the world's best-performing stock, surging 540%.

Data centre infrastructure

Companies like Emcor, which provides critical electrical, HVAC, and power infrastructure to data centres, reported its contracted backlog surged 31.2% year over year to a record US$13.25 billion. These companies can offer different exposure to the AI capex cycle, but they carry their own execution, backlog, margin and valuation risks.

What could derail the AI trade?

Valuation compression

Broadcom trades at about 50x earnings and AMD at 56x. Any disappointment in forward guidance could trigger a sharp contraction in multiples.

The return on investment test

Companies are investing today on the assumption that highly profitable business applications of AI will emerge over time. If the timing or scale of those returns disappoints, the AI trade could face pullbacks.

Index concentration

The 10 largest stocks in the S&P 500 account for about 40% of the index's total value. A rotation out of mega-cap tech could disproportionately affect broad indices.

Efficiency disruption

China's DeepSeek recently published research suggesting large language models may be developed more efficiently than previously assumed. If AI can be built with less compute, demand for GPUs and data centre hardware could fall short of current forecasts.

Bottom line for traders

The AI trade is maturing but far from over. 2026 is shaping up to be a more nuanced chapter, spreading across the full AI value chain.

The US earnings season will be closely watched for evidence that the hundreds of billions being poured into AI infrastructure are beginning to generate the anticipated returns.

All data points referenced in this article were verified against primary sources on 18 March 2026.